Did ATI's (ATI) Shift Into Russell Growth Indices Just Redefine Its Investor Base?

- ATI was recently reclassified by FTSE Russell into several Russell growth indices and removed from corresponding value indices, shifting its peer group toward faster-growing companies.

- This index migration may alter ATI’s investor base and trading patterns as growth-focused funds and benchmarks adjust their holdings and exposures.

- Next, we’ll examine how ATI’s move into Russell growth indices interacts with its aerospace-driven expansion and capital return plans.

AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

ATI Investment Narrative Recap

To own ATI, you have to believe its aerospace contracts, margin profile, and capital returns can justify a higher-growth identity. The Russell growth reclassification itself does not materially change ATI’s core near term catalysts around aerospace demand or its biggest risk, which remains concentration in a handful of large OEM customers and exposure to weaker non-aerospace end markets.

The most relevant recent announcement here is ATI’s expanded share repurchase authorization to US$1.2 billion, alongside ongoing buybacks that have already retired about 6.35% of shares. As ATI migrates into growth indices, this capital return program could influence how growth-oriented investors weigh its earnings trajectory, balance sheet leverage, and sensitivity to any slowdown in industrial and medical demand.

Yet, against the optimism around aerospace growth, investors should be aware of the risk that rising capital intensity and alternative materials could...

Read the full narrative on ATI (it's free!)

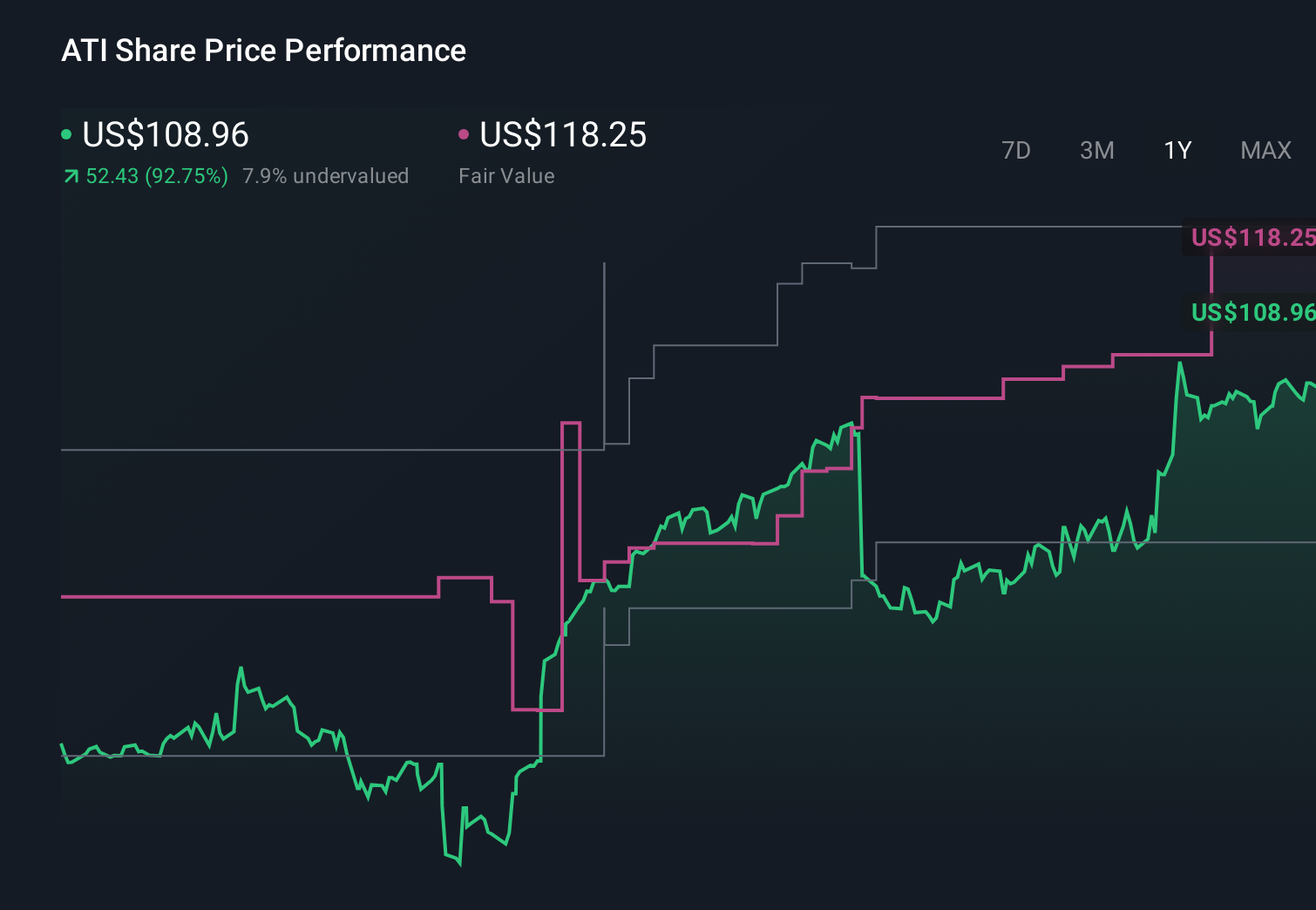

ATI's narrative projects $5.9 billion revenue and $864.9 million earnings by 2029.

Uncover how ATI's forecasts yield a $185.56 fair value, in line with its current price.

Exploring Other Perspectives

Compared with consensus, the most pessimistic analysts were already assuming ATI needs higher R&D just to defend relevance, even while forecasting revenue to about US$5.9 billion and earnings near US$838.3 million before this index shift, highlighting how sharply views can differ and why it is worth weighing several viewpoints before deciding what this new growth label might mean for you.

Explore 6 other fair value estimates on ATI - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com