Nvidia (NVDA) Stock Looks Fairly Priced As AI Hopes Face Tests

NVIDIA stock has delivered a very large 5 year return, yet the current checks give a more muted message, with the Discounted Cash Flow (DCF) intrinsic value estimate sitting close to the market price while the earnings multiple view still screens the shares as undervalued.

- NVIDIA has returned about 10.7x over 5 years, which puts extra pressure on today’s buyers to be confident that future cash flows can justify that kind of long term repricing.

- Ongoing heavy AI infrastructure spending by major customers can support the revenue and cash flow story, while rising competition from in house and regional AI chips may cap how much investors are willing to pay for that growth.

- The broader valuation checks are mixed rather than conclusive. NVIDIA scores 4 out of 6, which points to a stock that is not a clear bargain but also not obviously overpriced.

The issue now is whether NVIDIA’s current price already reflects a fair reading of its intrinsic value, or if the multiples signal enough upside to compensate for the competitive and capital spending risks that are now in focus.

Find out why NVIDIA's 28.1% return over the last year is lagging behind its peers.

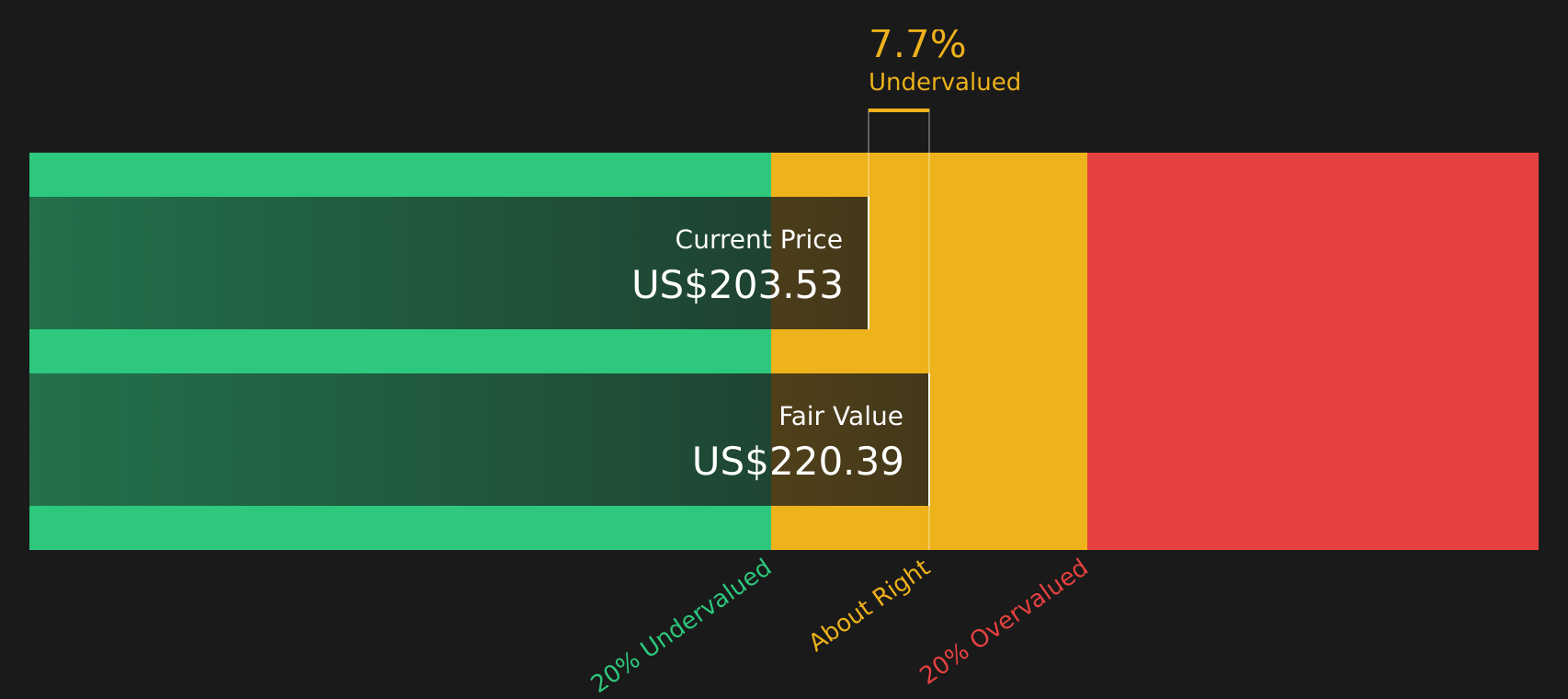

Does NVIDIA Look Fairly Valued on Cash Flow?

The Discounted Cash Flow (DCF) model used here estimates what NVIDIA’s future cash generation could be worth in today’s dollars. Over the latest twelve months, NVIDIA generated about $119.4b of free cash flow, and the model assumes those cash flows continue growing rather than shrinking, consistent with a 2 Stage Free Cash Flow to Equity framework.

Based on these assumptions, the DCF points to an estimated intrinsic value of about $220 per share, which is only slightly above the current market price. This implies the stock screens roughly 4.1% undervalued instead of offering a large margin of safety. Recent concerns about AI capital expenditure sustainability and sector-wide sell-offs help explain why the market is not assigning NVIDIA a significantly higher premium over this intrinsic value estimate, even with ongoing substantial AI infrastructure commitments from major customers.

Overall, the discounted cash flow analysis indicates that NVIDIA’s stock currently appears roughly fairly valued rather than clearly cheap or clearly expensive.

NVIDIA is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

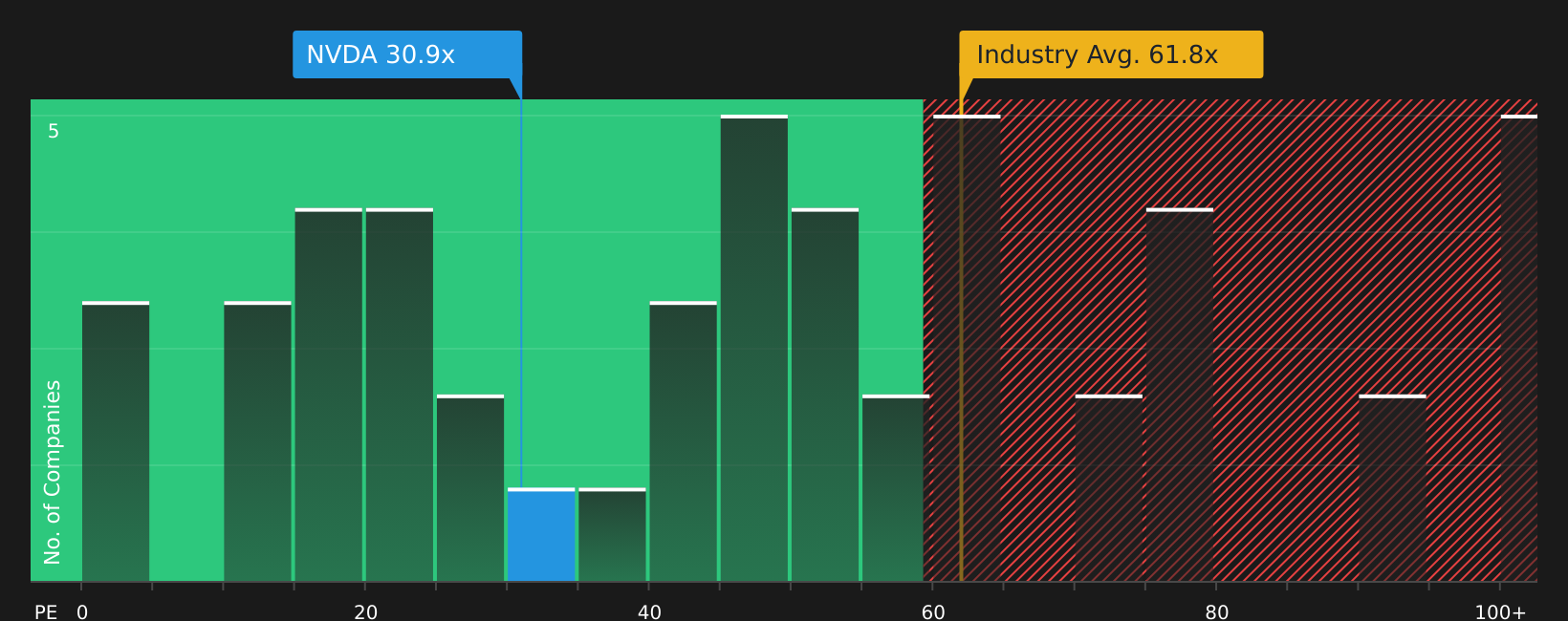

Is NVIDIA Still Cheap on Earnings?

The P/E ratio is a useful cross check for NVIDIA because earnings are now a key part of how investors frame the AI story. NVIDIA trades on about 32.0x earnings, compared with a Semiconductor industry average of about 65.1x and a peer average of roughly 88.3x. That is a sizable discount to both the sector and closest high growth peers.

On Simply Wall St’s “fair” P/E of about 64.9x, which adjusts for NVIDIA’s size, margins, growth profile and risks, the current multiple looks low. The model implies the stock could trade on roughly double today’s P/E before it lined up with that tailored benchmark, even after recent concerns about AI capex intensity and rising in house chip competition from major customers.

On earnings, NVIDIA appears clearly undervalued, with its current P/E well below both the industry averages and the fair multiple implied by its fundamentals.

See what the numbers say about this price — find out in our valuation breakdown.

The NVIDIA Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for NVIDIA pick up where this valuation puzzle leaves off by spelling out which assumptions about NVIDIA’s future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price on the Community page. Each narrative links a specific set of catalysts and risks to an estimated fair value, so you can track over time which version of NVIDIA’s story is closest to what actually unfolds.

The NVIDIA community is split between a scenario where the AI engine still has plenty of runway and one where the story is already priced for perfection.

Bull case: 38% undervalued

"Nvidia will hit $400b annual revenue in 5 years time, ~90% of revenue will come from data centre customers…"

Read the full Bull Case to see why NVIDIA could be undervalued

Bear case: 103% overvalued

"The extraordinary surge of GPU demand was front-loaded by the initial AI gold rush, once hyperscalers build capacity, incremental growth in training may slow sharply…"

Read the full Bear Case to see why NVIDIA could be overvalued

Do you think there's more to the story for NVIDIA? Head over to our Community to see what others are saying!

The Bottom Line

For NVIDIA, the Discounted Cash Flow (DCF) view suggests the stock is trading close to intrinsic value, so the recent move does not leave a wide margin of safety on cash generation alone. The earnings multiple view still screens the stock as undervalued, but that sits alongside broader checks that look mixed rather than emphatically cheap. The gap between the two views comes down to how you weigh heavy capital needs and cash flow timing against expectations for AI driven growth and sentiment. What ultimately matters from here is whether NVIDIA can sustain attractive economics on AI infrastructure as competition and customer in house chips evolve.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com