Delta Air Lines (DAL) After Fresh 2026 Guidance And Q2 Results Faces A Fair Value Debate

Delta Air Lines (DAL) stock is in focus after the company issued fresh third quarter and full year 2026 earnings guidance alongside its second quarter results, outlining expected revenue growth and detailed profit metrics.

See our latest analysis for Delta Air Lines.

At a share price of $87.39, Delta Air Lines has seen short term momentum cool, with the 7 day share price return down 4.68%. However, the 90 day share price return of 21.88% and 1 year total shareholder return of 52.56% point to stronger underlying interest building over a longer horizon.

If Delta Air Lines' recent move has you thinking about where else growth and sentiment could line up, it may be worth scanning 18 top founder-led companies

Delta Air Lines now trades around a 15% discount to analyst price targets and a wider gap to some fair value estimates. At the same time, guidance and recent profit trends keep investors cautious. How does that tension show up in the numbers next?

Most Popular Narrative: 38.3% Overvalued

According to the most followed narrative on Delta Air Lines, the current share price of $87.39 sits well above an assessed fair value of $63.21, which creates a clear gap investors will want to understand before relying on the market price alone.

Atlanta's flag carrier, so to speak, remains the lode star in the US network carrier heaven, with its profitability the current envy of the industry. Total revenue per available seat mile (TRASM) in Q4/25 stood at 21.94 cents, with total cost per available seat mile (CASM) at 19.93 cents, thus yielding a net profit of some 2 cents per available seat mile. This is simply oustanding, particularly for a legacy carrier.

Want to see how that unit profit per seat ties into the fair value for Delta Air Lines? The narrative leans heavily on revenue per mile, cost discipline and a tighter profit multiple to back into its $63.21 figure without assuming aggressive expansion or unusually high growth.

Result: Fair Value of $63.21 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, even for Delta Air Lines, weaker travel demand or renewed balance sheet pressure could quickly challenge assumptions around unit economics and that $63.21 fair value anchor.

Find out about the key risks to this Delta Air Lines narrative.

Another View on Delta Air Lines’ Valuation

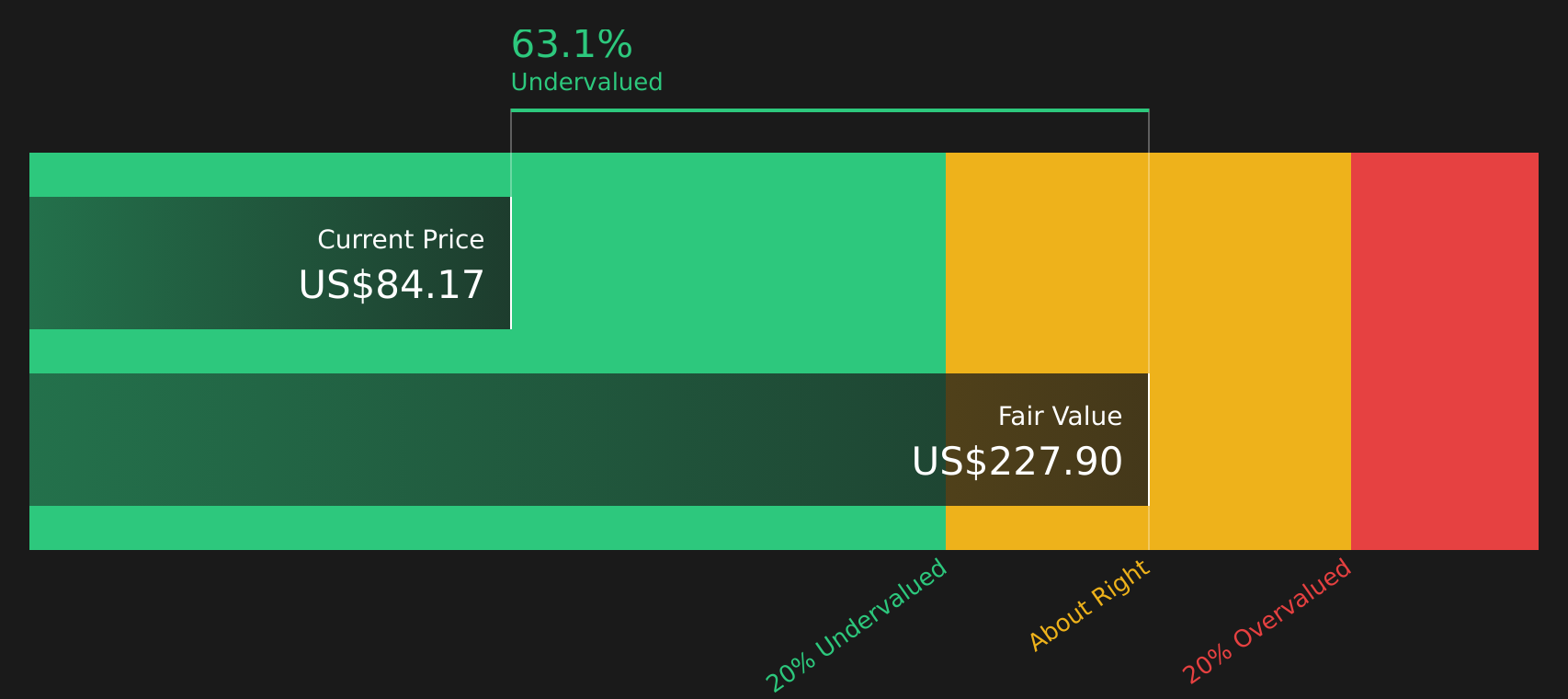

That first fair value of $63.21 suggests Delta Air Lines is 38.3% overvalued, but our DCF model points in a very different direction. On those cash flow assumptions, Delta screens as undervalued at $87.39 versus an estimated future cash flow value of $156.34. Which story feels more reasonable to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Delta Air Lines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed messages on Delta Air Lines valuation leave you undecided, do not wait on others to interpret the story for you. Instead, weigh the positives and negatives yourself with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Delta Air Lines?

If Delta Air Lines has sharpened your focus on valuation and risk, do not stop here. Put that curiosity to work by scanning other opportunities with targeted screeners.

- Target cash rich quality by reviewing companies in the solid balance sheet and fundamentals stocks screener (47 results) that pair sturdier finances with fundamental strength.

- Hunt for potential value opportunities by checking the 45 high quality undervalued stocks that highlight stocks priced below their assessed quality.

- Prioritise resilience by scanning the 78 resilient stocks with low risk scores that flags businesses with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com