Top European Dividend Stocks To Consider In July 2026

As geopolitical tensions and energy market volatility continue to impact the European markets, the pan-European STOXX Europe 600 Index recently experienced a decline of 1.79%. In this environment, investors may find value in dividend stocks, which can offer a steady income stream and potentially provide some stability amidst market fluctuations.

Top 10 Dividend Stocks In Europe

| Name | Dividend Yield | Dividend Rating |

| Zurich Insurance Group (SWX:ZURN) | 4.08% | ★★★★★★ |

| Teleperformance (ENXTPA:TEP) | 8.63% | ★★★★★★ |

| Telekom Austria (WBAG:TKA) | 4.20% | ★★★★★★ |

| Swiss Re (SWX:SREN) | 4.88% | ★★★★★★ |

| Rubis (ENXTPA:RUI) | 6.60% | ★★★★★★ |

| Logista Integral (BME:LOG) | 5.93% | ★★★★★★ |

| Hannover Rück (XTRA:HNR1) | 5.00% | ★★★★★★ |

| Edel SE KGaA (XTRA:EDL) | 6.28% | ★★★★★★ |

| DKSH Holding (SWX:DKSH) | 3.80% | ★★★★★★ |

| Cembra Money Bank (SWX:CMBN) | 4.51% | ★★★★★★ |

Click here to see the full list of 212 stocks from our Top European Dividend Stocks screener.

We'll examine a selection from our screener results.

UIE (CPSE:UIE)

Simply Wall St Dividend Rating: ★★★★☆☆

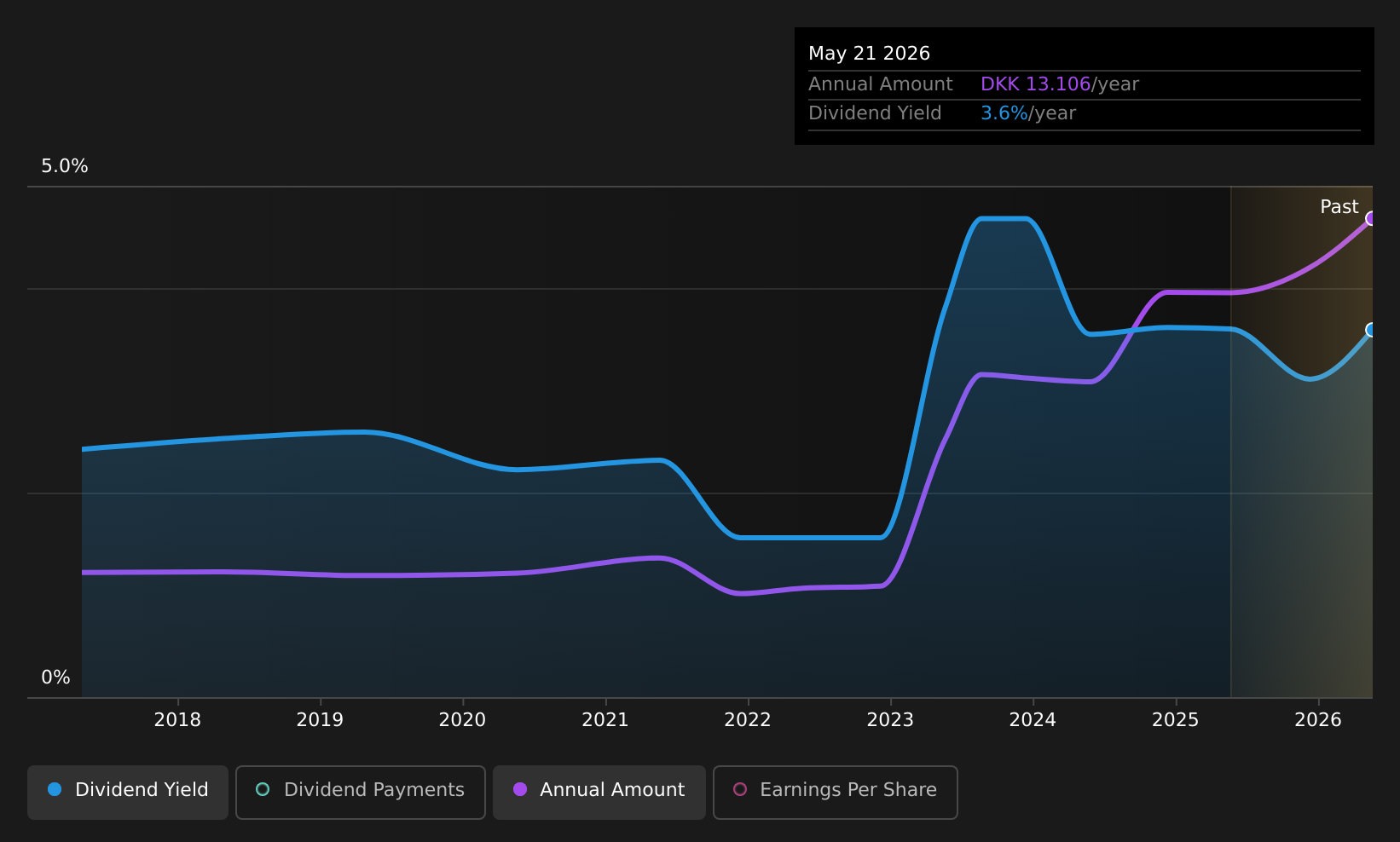

Overview: UIE Plc is an investment company focusing on the agro-industrial and industrial and technology sectors across Malaysia, Indonesia, the United States, Europe, and internationally, with a market cap of DKK11.39 billion.

Operations: UIE Plc generates revenue from its investment in United Plantations Berhad, amounting to $632.63 million.

Dividend Yield: 3.6%

UIE's recent approval of a final dividend of US$1.02 per share highlights its commitment to shareholder returns, although the company's dividend history has been volatile over the past decade. Despite this instability, dividends are well-covered by both earnings and cash flows, with payout ratios at 56.4% and 39.2%, respectively. While trading significantly below estimated fair value, UIE's dividend yield of 3.59% remains lower than top-tier Danish market payers but reflects stable coverage from financial performance metrics.

- Unlock comprehensive insights into our analysis of UIE stock in this dividend report.

- In light of our recent valuation report, it seems possible that UIE is trading beyond its estimated value.

Sparebanken Møre (OB:MORG)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Sparebanken Møre, along with its subsidiaries, offers banking services to both retail and business markets in Norway and has a market cap of NOK5.54 billion.

Operations: Sparebanken Møre generates revenue from several segments, including NOK1.05 billion from retail, NOK804 million from corporate, and NOK41 million from real estate brokerage.

Dividend Yield: 6.3%

Sparebanken Møre's dividend payments have been volatile and unreliable over the past decade, though they have increased during this period. Despite a low allowance for bad loans at 21%, the bank maintains a reasonable payout ratio of 74.3%, ensuring dividends are currently covered by earnings and forecasted to remain so in three years with a 71.7% payout ratio. Trading at 38.5% below fair value, its dividend yield of 6.26% is lower than top-tier Norwegian payers' yields.

- Dive into the specifics of Sparebanken Møre here with our thorough dividend report.

- Our valuation report unveils the possibility Sparebanken Møre's shares may be trading at a discount.

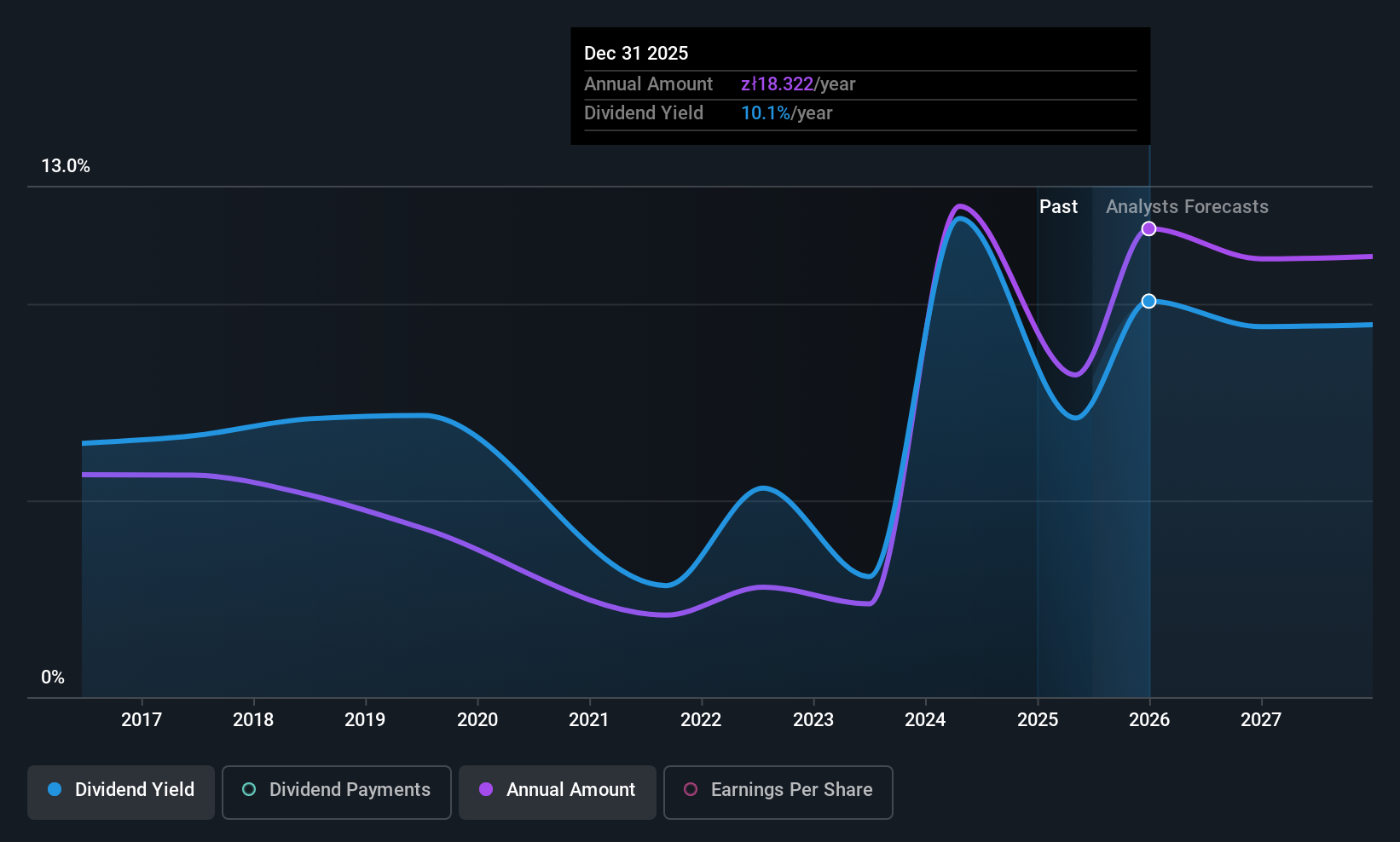

Bank Polska Kasa Opieki (WSE:PEO)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Bank Polska Kasa Opieki S.A. is a commercial bank offering a range of banking products and services to both retail and corporate clients in Poland, with a market cap of PLN64.12 billion.

Operations: Bank Polska Kasa Opieki S.A. generates revenue primarily from Retail & Private Banking (PLN7.75 billion), Corporate and Investment Banking (PLN3.46 billion), and Enterprise Banking (PLN1.93 billion).

Dividend Yield: 8.1%

Bank Polska Kasa Opieki's dividend yield is among the top 25% in Poland, supported by a current payout ratio of 79.1%, which is forecast to decrease to 66.5% in three years, indicating sustainable coverage by earnings. Despite trading at a good value and having increased dividends over the past decade, its payments have been volatile with periods of significant drops. The bank also faces challenges with a high level of bad loans at 4.3%.

- Click here and access our complete dividend analysis report to understand the dynamics of Bank Polska Kasa Opieki.

- The analysis detailed in our Bank Polska Kasa Opieki valuation report hints at an deflated share price compared to its estimated value.

Taking Advantage

- Get an in-depth perspective on all 212 Top European Dividend Stocks by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com