Will Komatsu’s (TSE:6301) Buyback and New Green Bond Shift Its Capital Allocation Narrative?

- In early July 2026, Komatsu Ltd. completed a share repurchase of 9,586,700 shares for ¥61,707.97 million and issued two unsecured straight bonds totaling ¥50.00 billion, including a ¥20.00 billion green bond due 2029 and a ¥30.00 billion bond due 2031.

- This combination of balance sheet reshaping through buybacks and the issuance of a labeled green bond highlights Komatsu’s evolving capital structure and sustainability-focused funding approach.

- We’ll now consider how Komatsu’s completion of this sizeable buyback could influence its existing investment narrative and future return drivers.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Komatsu Investment Narrative Recap

To own Komatsu today, you need to believe its core construction and mining franchises can stabilise earnings despite softer demand and margin pressure in key regions. The latest buyback completion and new bond issues appear more like incremental capital structure moves than game changers for near term catalysts, while the biggest risk remains prolonged weakness in core equipment demand and potential tariff or input cost pressures that could further squeeze margins.

Among recent announcements, the April 2026 guidance for fiscal 2027 stands out alongside this buyback. Management outlined net sales of ¥4,118,000 million and net income of ¥318,000 million, framing investor expectations for earnings as the company adjusts its capital structure. Against that backdrop, retiring 1.06% of shares and raising ¥50,000 million in unsecured bonds, including a green bond, will now be assessed against how effectively Komatsu can defend profitability in its core segment.

Yet against these shareholder friendly moves, investors should be aware that prolonged softness in Construction, Mining & Utility equipment demand could still...

Read the full narrative on Komatsu (it's free!)

Komatsu's narrative projects ¥4,536.9 billion revenue and ¥436.9 billion earnings by 2029. This requires 3.2% yearly revenue growth and about a ¥60.7 billion earnings increase from ¥376.2 billion today.

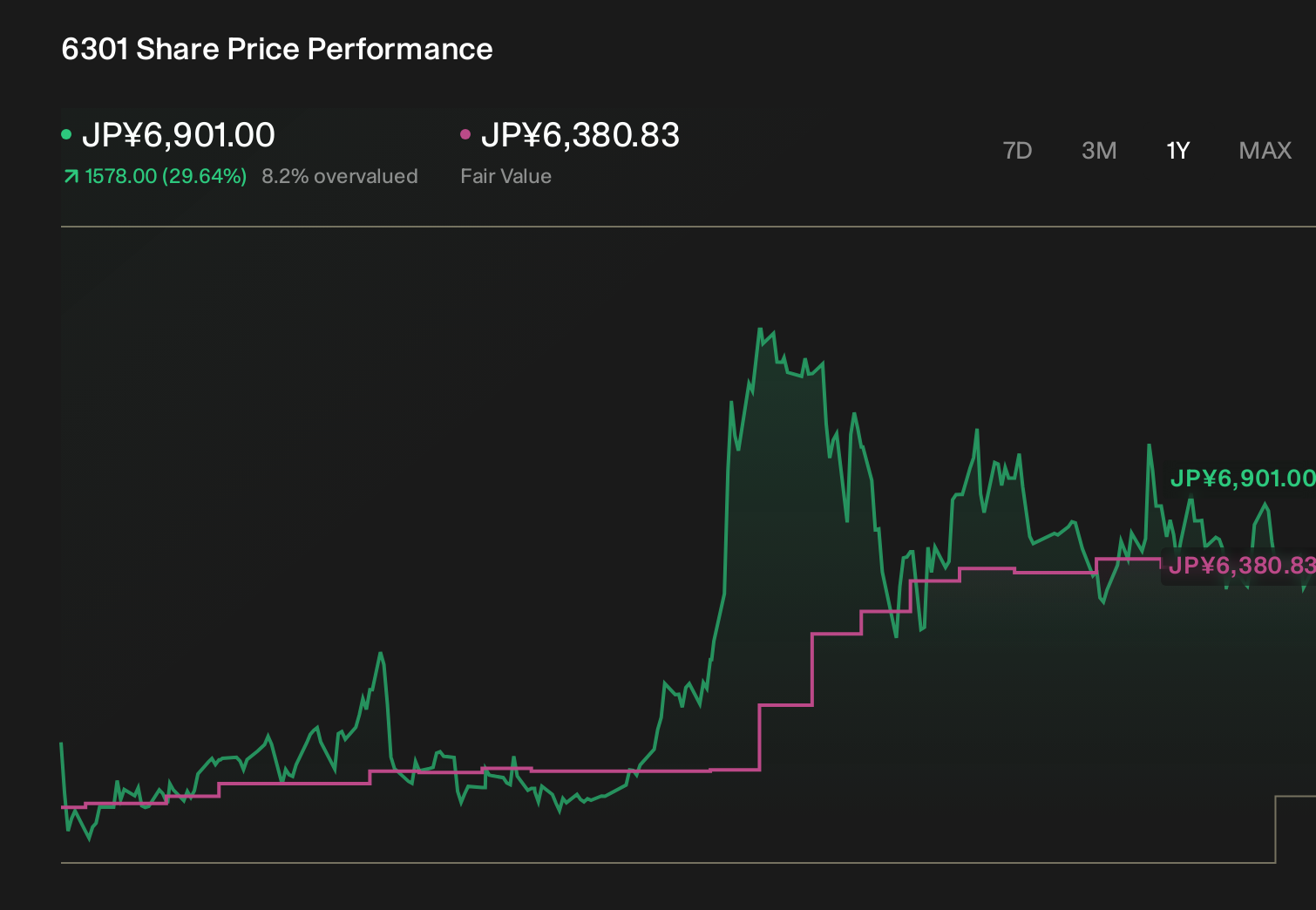

Uncover how Komatsu's forecasts yield a ¥6381 fair value, in line with its current price.

Exploring Other Perspectives

Some analysts were already more optimistic, assuming earnings could reach about ¥520,700 million by 2029, but if tariffs and input costs rise further, that upbeat view may...

Explore 2 other fair value estimates on Komatsu - why the stock might be worth just ¥6381!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Komatsu research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Komatsu research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Komatsu's overall financial health at a glance.

No Opportunity In Komatsu?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com