BYD Stock Leads 3 Auto Shares Under Pressure From Europe’s Cost Squeeze

Global automakers are under pressure as profit falls, job cut plans and rising competition from Chinese rivals reshape expectations for costs and market share. Volkswagen’s sharp drop in operating profit from €22.6b to €8.9b, weaker China and US sales and talk of up to 100,000 job cuts underline how intense the squeeze has become. For investors, this kind of stress can create both potential opportunity and risk. The following sections look at three European auto stocks exposed to these headlines, with one that may be comparatively better positioned and two where the news may point to tougher conditions ahead.

Daimler Truck Holding (XTRA:DTG)

Overview: Daimler Truck Holding is a global commercial vehicle group that manufactures trucks, buses and related components across brands such as Mercedes Benz, Freightliner and FUSO, and supports customers with financing, leasing and charging services for zero emission fleets.

Operations: Daimler Truck Holding generates most of its revenue in trucks, with Mercedes Benz Trucks at about €19.9b and Trucks North America at about €17.2b, alongside €5.9b from Daimler Buses and €3.4b from Financial Services, partly offset by reconciliation and segment adjustment items.

Market Cap: €31.97b

Daimler Truck Holding may look interesting at first glance, with shares trading below one estimate of fair value and analyst forecasts that point to faster earnings growth than the wider German market. However, the picture is far from comfortable. Profit margins have slipped to 2.7%, last year’s earnings fell more than 50%, and a large one off loss of €559m plus weaker cash coverage of debt raise questions about how easily the company can fund its zero emission transition. At the same time, Volkswagen’s difficulties highlight shared pressures on German manufacturers from higher costs, tariffs and labor restructuring. For investors, the key question is whether Daimler Truck’s technology and global reach can offset these headwinds before funding and profitability risks build further.

Daimler Truck’s shrinking margins, large one off loss and funding needs for zero emission fleets suggest the real tension is on its balance sheet and future flexibility, so weighing up the full Daimler Truck Holding financial health report

Stellantis (BIT:STLAM)

Overview: Stellantis is a global automaker that designs and builds passenger cars, SUVs, light commercial vehicles and related parts, and also offers financing, leasing, mobility and data services across well known brands including Jeep, Fiat, Peugeot, Opel, Citroën, Dodge, Chrysler, Maserati and Alfa Romeo.

Operations: Stellantis generates most of its revenue in North America at about €62.6b and Enlarged Europe at about €58.0b, with smaller contributions from South America at about €16.1b, Middle East and Africa at about €9.8b, Asia Pacific at about €1.8b and other activities and adjustments.

Market Cap: €14.0b

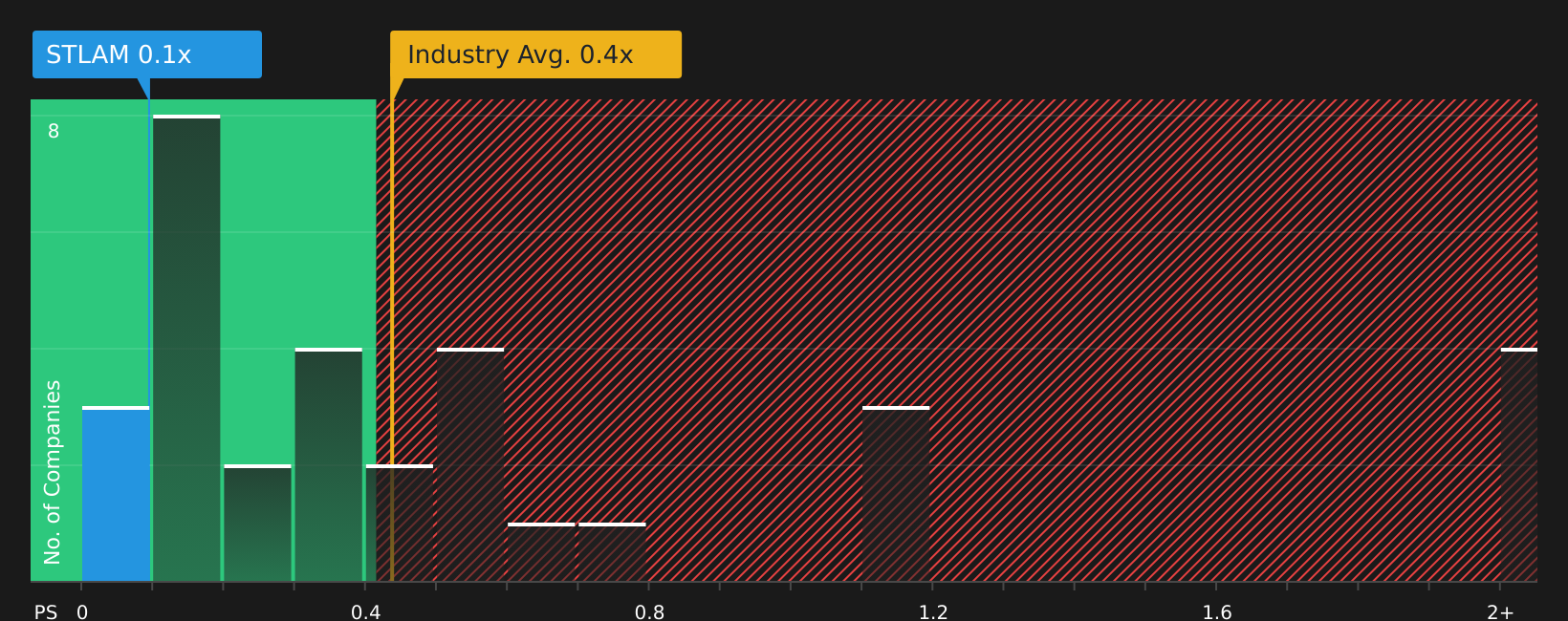

Stellantis gives investors a complex mix of potential recovery and clear warning signs, which is why it deserves attention. The company is working through a steep pullback in adjusted operating income from €24.3b to €8.6b as higher industrial costs, tariffs and tougher pricing in Europe weigh on margins. Management openly describes Europe as a very competitive market with profitability headwinds from electric vehicles. At the same time, the stock trades at a low P/S multiple and analysts expect earnings to rebound from a large loss to profitability within a few years, although recent target cuts and rating downgrades underline how uncertain that path looks. How Stellantis handles cost cutting, rising Chinese competition and its heavy external funding load will be crucial to the story investors are missing today.

Stellantis faces an earnings story that looks stalled, with low P/S and heavy external funding hinting at risks many investors may be glossing over. For more detail, it is worth reading the full 3 key rewards and 1 important warning sign

BYD (SEHK:1211)

Overview: BYD is a Chinese technology group that builds electric and hybrid vehicles, batteries and components, and also supplies mobile handset parts, energy storage systems and rail transit solutions for customers in China and overseas markets.

Market Cap: HK$852.5b

BYD sits at the center of the pressure Volkswagen is feeling, as a vertically integrated Chinese automaker able to produce its own batteries, powertrains and chips at lower cost while pushing aggressively into Europe with new plants and fast charging networks. The company is leaning on its Blade Battery and hybrid platforms to support export led growth and large scale projects such as energy storage for Abu Dhabi. However, current profit margins of 3.5%, year on year margin pressure and reliance on external borrowing show that growth is not without strain. For investors, the attraction is a business that combines autos and energy technology at scale, while the real debate is how comfortably that growth can be funded and converted into stronger profitability as European competition intensifies.

BYD’s mix of autos and energy tech at scale could be more than a growth story; it may hinge on how future earnings stack up against today’s expectations, so reviewing the analyst forecasts for BYD might reveal what the market has not fully priced in yet

Take Control of Your Investment Journey

If Stellantis or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond European Autos?

Fresh ideas move first, not last. Before the next breakout gains momentum and early pricing edges start flying away, scan under the radar for now, act now.

- Target steadier compounding potential by reviewing a curated 475 dividend fortresses built to prioritize payout strength, balance sheet resilience and consistency while those yields are still available.

- Spot fast moving niches by scanning 52 AI infrastructure stocks that may benefit from the build out behind AI momentum before the crowd fully catches on.

- Ride structural demand shifts by checking a focused 34 power grid technology and infrastructure stocks aligned with long term grid upgrades while valuations still reflect today’s expectations and not tomorrow’s headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com