Is Pre‑Earnings Focus On Recurring Revenue And Deals Altering The Investment Case For Ingersoll Rand (IR)?

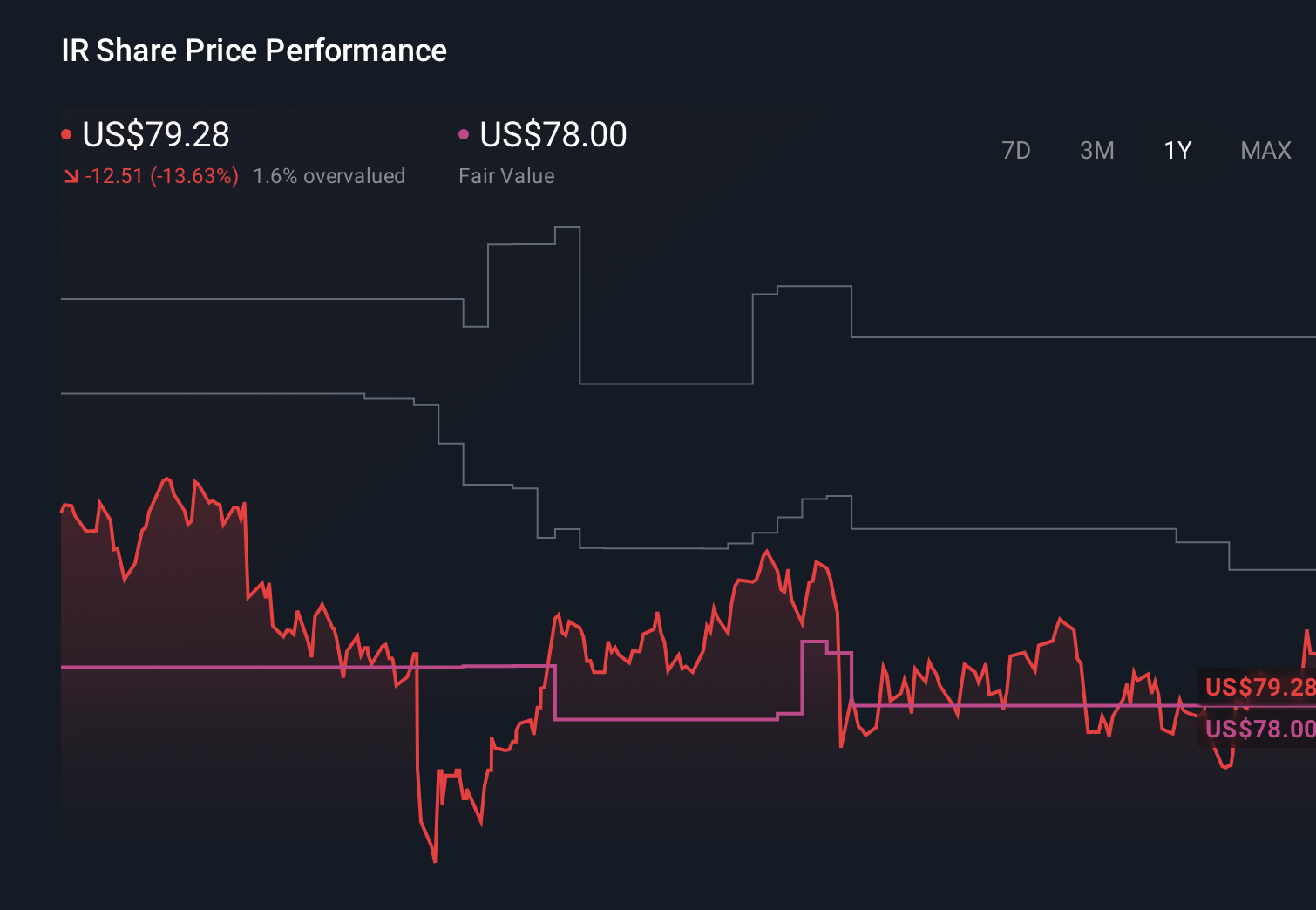

- Ingersoll Rand recently drew attention ahead of its fiscal second-quarter 2026 earnings release, with analysts projecting diluted earnings of US$0.80 per share versus US$0.77 a year earlier and debating whether the stock is undervalued based on differing valuation methods.

- Investors are also weighing the benefits of Ingersoll Rand’s growing recurring, high-margin aftermarket revenue against risks from its acquisition-heavy growth model and exposure to shifting global trade policies that could pressure profitability.

- We’ll now examine how this pre-earnings focus on recurring revenue growth and acquisition risk could reshape Ingersoll Rand’s broader investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand today, you need to be comfortable paying a relatively full multiple for a company leaning heavily on recurring aftermarket revenue and bolt‑on acquisitions to support earnings. The immediate catalyst is the upcoming Q2 2026 earnings print, where projected diluted EPS of US$0.80 will test whether the aftermarket story is translating into profit consistency. The biggest near term risk remains that acquisition complexity and changing trade policies continue to weigh on margins and compress the earnings profile. So far, this new pre‑earnings news sharpens that focus but does not fundamentally alter it.

Among recent announcements, the multiyear alliance with Garrett Motion to develop next‑generation oil free air technologies stands out as most relevant. It ties directly into the higher margin, recurring service and lifecycle solutions theme that analysts see as supporting earnings resilience, while also intersecting with earlier product innovations like CompAir Ultima and EVO Series pumps. How well these cleaner, more efficient offerings gain traction could influence whether the current valuation debate tilts toward upside or downside.

Yet against that opportunity, investors also need to be aware of how heavy reliance on acquisitions could interact with shifting global trade policies and...

Read the full narrative on Ingersoll Rand (it's free!)

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029.

Uncover how Ingersoll Rand's forecasts yield a $93.20 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in roughly US$9.4 billion of revenue and US$1.5 billion of earnings by 2029, which is far more upbeat than the baseline view tied to recurring aftermarket growth and acquisition risk, and shows just how differently you might interpret today’s pre earnings headlines.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth just $86.69!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com