ASX Penny Stocks To Watch In July 2026

The Australian share market is currently searching for direction, with ASX 200 futures slightly down amid global uncertainties such as surging oil prices and potential interest rate hikes in the U.S. As investors navigate these turbulent waters, penny stocks—though a somewhat outdated term—remain an intriguing area of investment, especially when they are supported by strong financial health. These smaller or newer companies can offer unique growth opportunities that larger firms might overlook, making them worth watching for those seeking under-the-radar investments with long-term potential.

Underneath we present a selection of stocks filtered out by our screen.

BKI Investment (ASX:BKI)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: BKI Investment Company Limited is a publicly owned investment manager with a market cap of A$1.49 billion.

Operations: The company's revenue is derived entirely from the Securities Industry, amounting to A$70.33 million.

Market Cap: A$1.49B

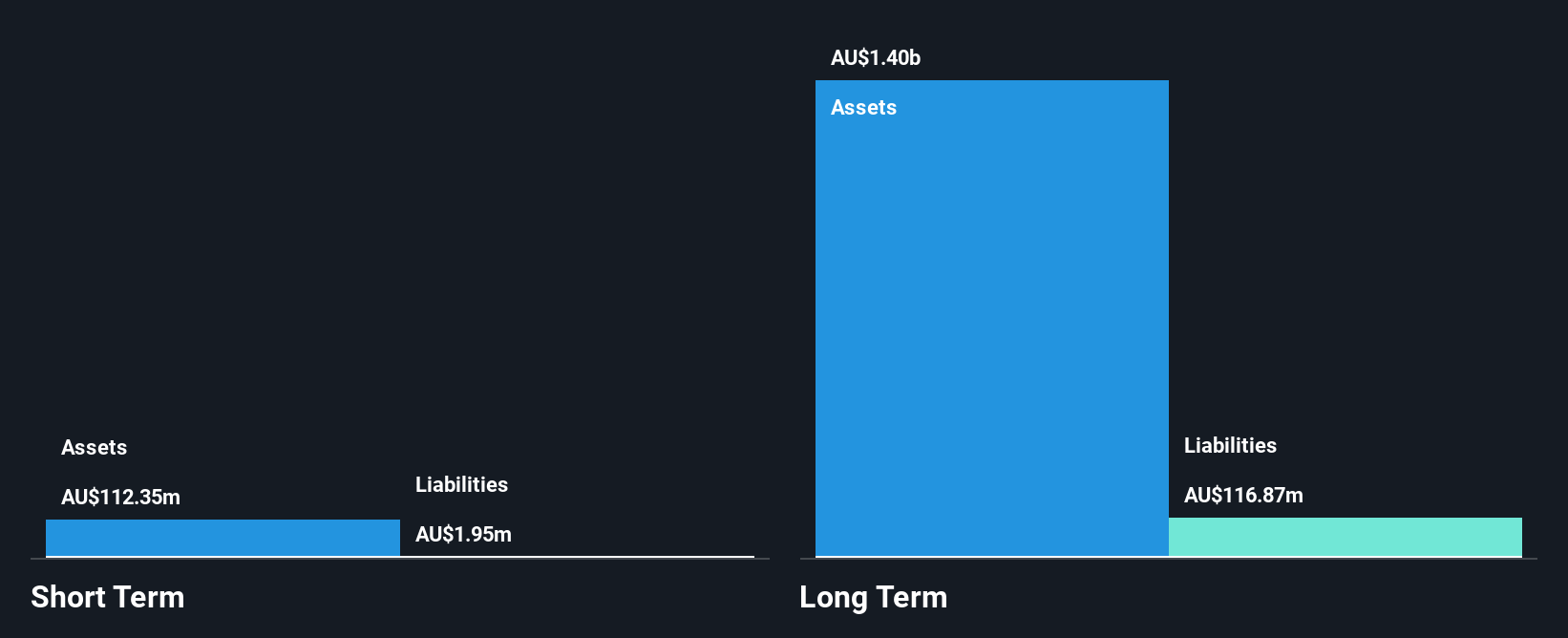

BKI Investment Company Limited, with a market cap of A$1.49 billion, demonstrates stability through its consistent weekly volatility of 2% and high-quality earnings. Despite being debt-free and having a seasoned board with an average tenure of 22.8 years, BKI faces challenges such as a low Return on Equity at 4.5% and insufficient coverage of long-term liabilities by short-term assets (A$82.1M vs A$137.8M). While its dividend yield of 4.32% is not well covered by earnings or cash flows, the company has shown modest profit growth over the past year at 6.3%.

- Unlock comprehensive insights into our analysis of BKI Investment stock in this financial health report.

- Gain insights into BKI Investment's historical outcomes by reviewing our past performance report.

Bathurst Resources (ASX:BRL)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Bathurst Resources Limited is involved in the exploration, development, and production of bituminous and coking coal in New Zealand and Canada, with a market cap of A$122.43 million.

Operations: The company generates revenue from two primary segments: NZ$248.35 million from export sales and NZ$136.41 million from domestic sales.

Market Cap: A$122.43M

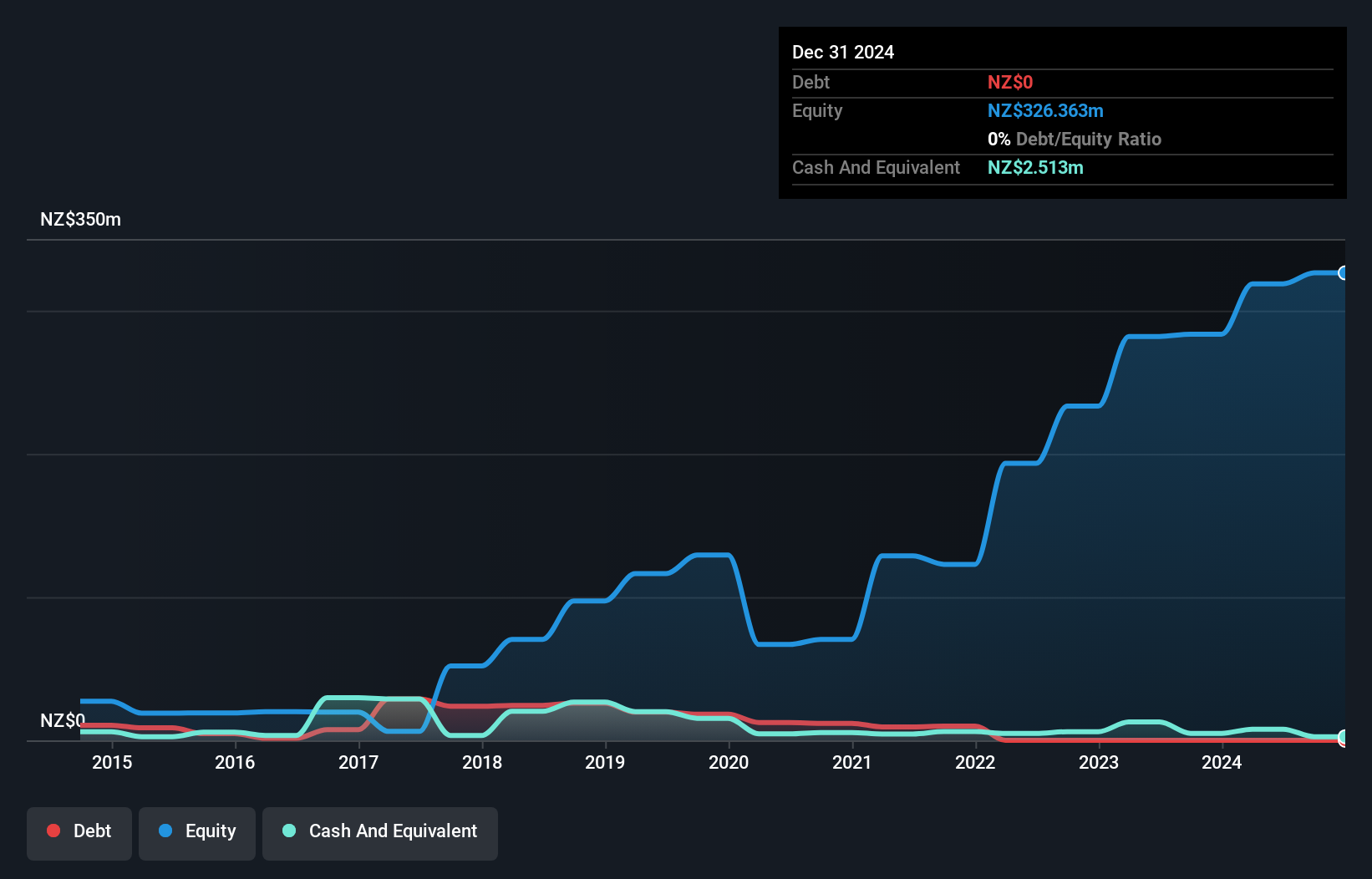

Bathurst Resources Limited, with a market cap of A$122.43 million, operates without debt, eliminating concerns over interest payments and enhancing financial flexibility. Despite its unprofitability and negative Return on Equity (-2.03%), the company benefits from experienced management and board teams with average tenures of 5.5 and 11.3 years respectively. While short-term assets (NZ$37.5M) cover both short-term (NZ$10.1M) and long-term liabilities (NZ$16M), losses have increased by 7.1% annually over five years, posing a challenge to future profitability despite forecasted earnings growth of 23.67% per year.

- Get an in-depth perspective on Bathurst Resources' performance by reading our balance sheet health report here.

- Examine Bathurst Resources' earnings growth report to understand how analysts expect it to perform.

Omni Bridgeway (ASX:OBL)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Omni Bridgeway Limited, with a market cap of A$482.25 million, offers dispute and litigation finance services across various regions including Australia, the United States, Canada, Latin America, Asia, New Zealand, Europe, the Middle East, and Africa.

Operations: The company's revenue is primarily derived from funding and providing services related to legal dispute resolution, amounting to A$200.52 million.

Market Cap: A$482.25M

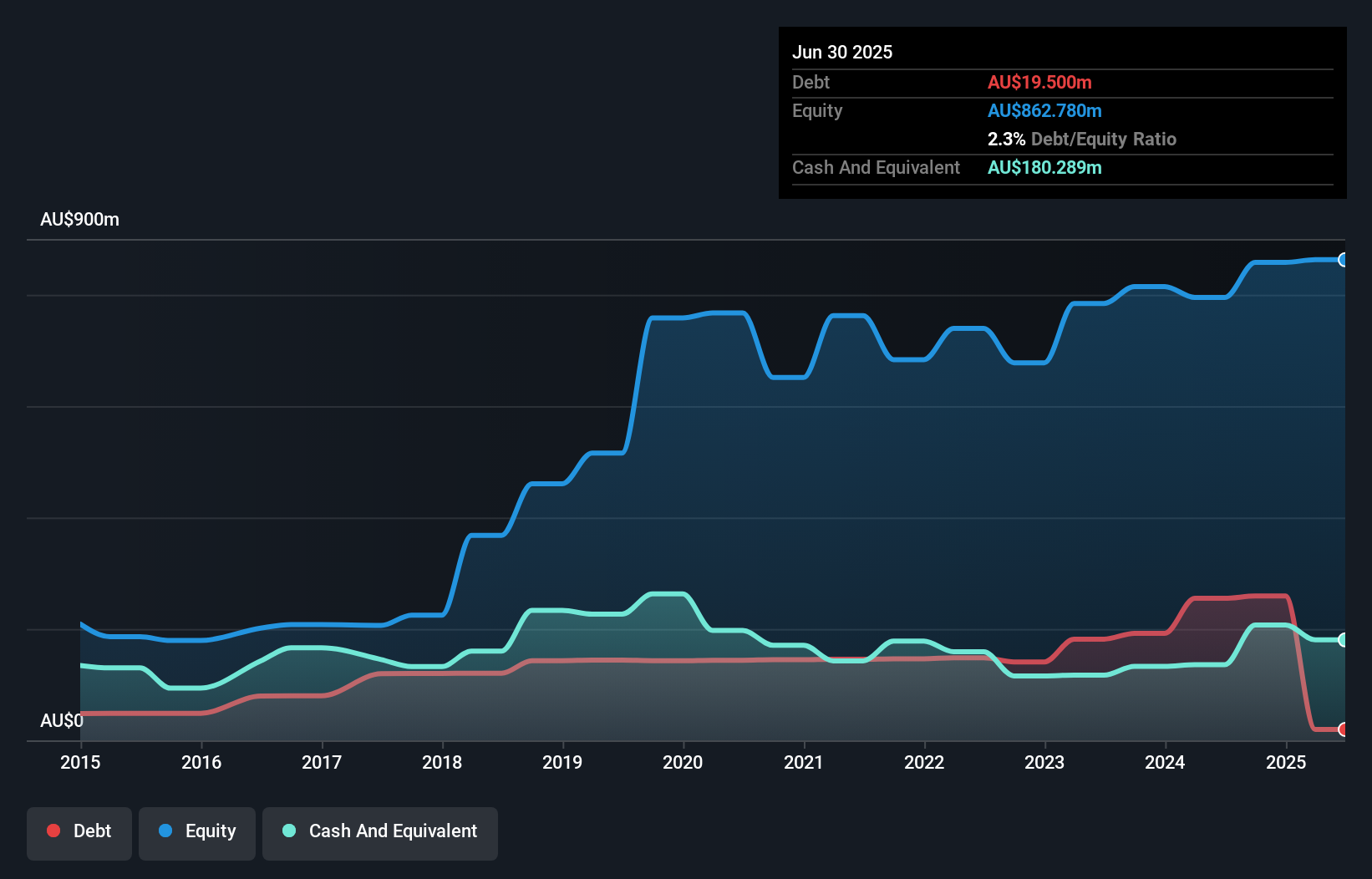

Omni Bridgeway Limited, with a market cap of A$482.25 million, has recently achieved profitability after five years of growth, with earnings increasing by 62.5% annually. The company is financially robust; its short-term assets exceed both short-term and long-term liabilities, while cash surpasses total debt. Despite negative operating cash flow impacting debt coverage, the firm benefits from an outstanding Return on Equity at 52.2% and trades at a favorable price-to-earnings ratio compared to the Australian market. Its experienced management and board teams further bolster confidence in its operational stability amidst industry challenges.

- Jump into the full analysis health report here for a deeper understanding of Omni Bridgeway.

- Gain insights into Omni Bridgeway's outlook and expected performance with our report on the company's earnings estimates.

Make It Happen

- Gain an insight into the universe of 405 ASX Penny Stocks by clicking here.

- Want To Explore Some Alternatives? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com