Undiscovered Gems in Asia to Explore This July 2026

As global markets navigate renewed geopolitical tensions and energy market volatility, the Asian equities landscape presents unique opportunities for discovery. With small-cap stocks in focus, investors may find potential in companies that demonstrate resilience and innovation amidst these broader market dynamics.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| Management SolutionsLtd | 10.02% | 26.20% | 33.40% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

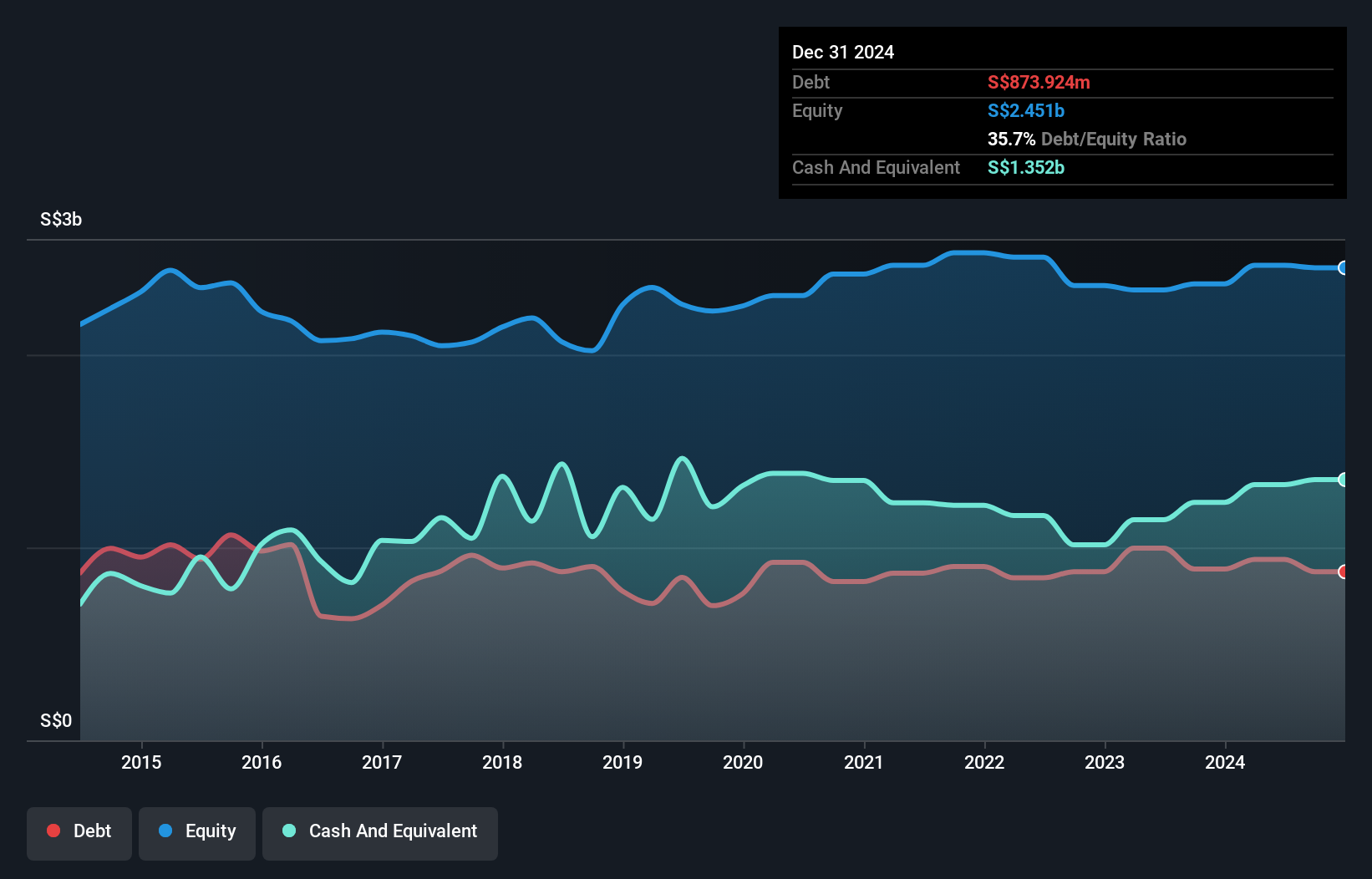

Hong Leong Asia (SGX:H22)

Simply Wall St Value Rating: ★★★★★★

Overview: Hong Leong Asia Ltd. is an investment holding company that manufactures and distributes powertrain solutions, building materials, and rigid packaging products across China, Singapore, Malaysia, and internationally with a market capitalization of approximately SGD2.10 billion.

Operations: The company generates significant revenue from its powertrain solutions segment, amounting to SGD4.48 billion, with building materials contributing SGD682.70 million. The net profit margin trends provide key insights into the company's profitability dynamics over time.

Hong Leong Asia's recent performance paints an intriguing picture. The company's earnings grew by 29.1% in the past year, outpacing the Machinery industry's 5.4% growth, and are forecasted to grow at nearly 20% annually. Trading at a significant discount of about 58.8% below its estimated fair value suggests potential upside for investors seeking hidden opportunities in smaller stocks. With a debt-to-equity ratio reduced from 34% to 29.3% over five years and more cash than total debt, financial stability appears robust. Recent strategic moves include a SGD145 million equity offering and dividend affirmations, indicating proactive capital management strategies.

Beijing Caishikou Department StoreLtd (SHSE:605599)

Simply Wall St Value Rating: ★★★★★★

Overview: Beijing Caishikou Department Store Co., Ltd. operates in the retail sector, focusing on gold and jewelry, with a market capitalization of approximately CN¥10.94 billion.

Operations: The company generates revenue primarily from its gold and jewelry retail segment, amounting to CN¥34.87 billion. Its financial performance includes a notable net profit margin trend, which stands at 3.5% in the latest reporting period.

Beijing Caishikou Department Store, a modestly sized player in the retail sector, shows promising financial health with no debt on its books and a significant earnings growth of 58.1% over the past year, outpacing the industry average of 12.3%. The company reported impressive sales figures for 2025 at CNY 28.79 billion, up from CNY 20.21 billion in the prior year, while net income climbed to CNY 1.13 billion from CNY 719 million. Trading at an estimated value significantly below its fair price and boasting high-quality non-cash earnings, it appears well-positioned for continued growth within its market segment.

- Click here to discover the nuances of Beijing Caishikou Department StoreLtd with our detailed analytical health report.

Learn about Beijing Caishikou Department StoreLtd's historical performance.

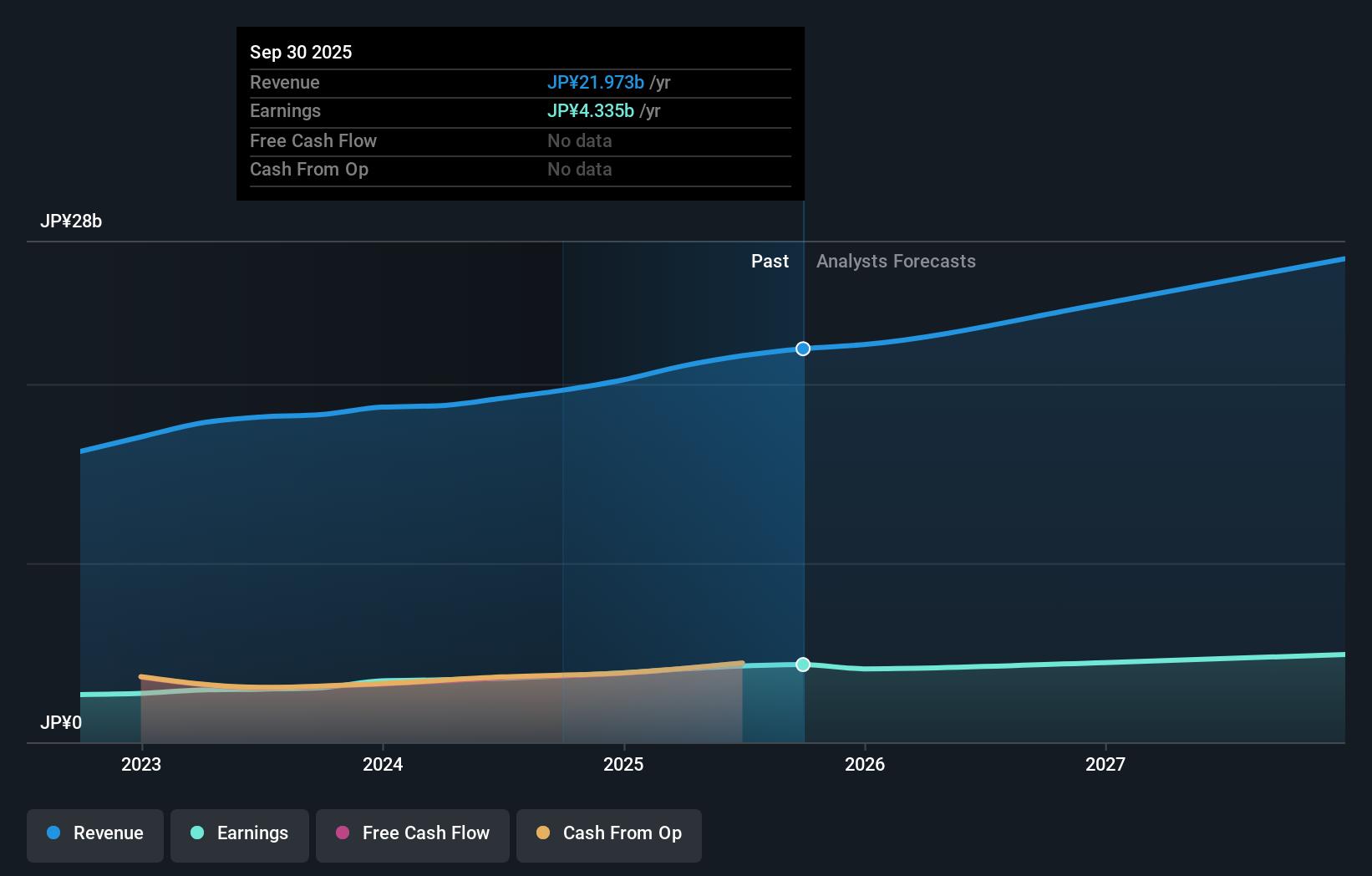

Base (TSE:4481)

Simply Wall St Value Rating: ★★★★★★

Overview: Base Co., Ltd., along with its subsidiaries, is involved in computer software development and related activities in Japan, with a market capitalization of ¥57.34 billion.

Operations: Base Co., Ltd. generates revenue primarily from its Software Contract Development Business, which reported ¥21.70 billion in revenue.

Base Co., Ltd. stands out with its debt-free status, a notable improvement from five years ago when the debt-to-equity ratio was 6.9%. Trading at 29% below estimated fair value, it offers attractive prospects for investors. Despite earnings growth of 0.9% over the past year lagging behind the IT industry's 13%, Base has achieved an impressive annual earnings growth rate of 17.6% over five years, showcasing its potential for sustained performance. Recent quarterly results showed sales at ¥5,472 million and net income at ¥1,008 million, reflecting a slight decrease from last year’s figures but maintaining profitability with high-quality earnings.

- Unlock comprehensive insights into our analysis of Base stock in this health report.

Review our historical performance report to gain insights into Base's's past performance.

Next Steps

- Gain an insight into the universe of 110 Asian Undiscovered Gems With Strong Fundamentals by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com