Discover Griffin Mining And 2 More UK Stocks Believed To Be Trading Below Intrinsic Value

The United Kingdom's stock market has recently experienced a downturn, with the FTSE 100 and FTSE 250 indices both closing lower amid weak trade data from China, which continues to grapple with post-pandemic economic challenges. In such an environment, identifying stocks that are potentially trading below their intrinsic value can be appealing for investors looking to capitalize on market inefficiencies and potential long-term growth opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Playtech (LSE:PTEC) | £3.982 | £7.30 | 45.4% |

| Morgan Advanced Materials (LSE:MGAM) | £2.165 | £3.92 | 44.7% |

| M&G (LSE:MNG) | £3.463 | £6.22 | 44.3% |

| Kistos Holdings (AIM:KIST) | £2.80 | £5.40 | 48.1% |

| Kainos Group (LSE:KNOS) | £7.87 | £14.46 | 45.6% |

| Eurocell (LSE:ECEL) | £1.11 | £2.17 | 48.8% |

| Entain (LSE:ENT) | £5.582 | £10.86 | 48.6% |

| AstraZeneca (LSE:AZN) | £126.10 | £228.67 | 44.9% |

| Advanced Medical Solutions Group (AIM:AMS) | £2.795 | £4.95 | 43.5% |

| Accsys Technologies (AIM:AXS) | £0.75 | £1.46 | 48.7% |

Let's take a closer look at a couple of our picks from the screened companies.

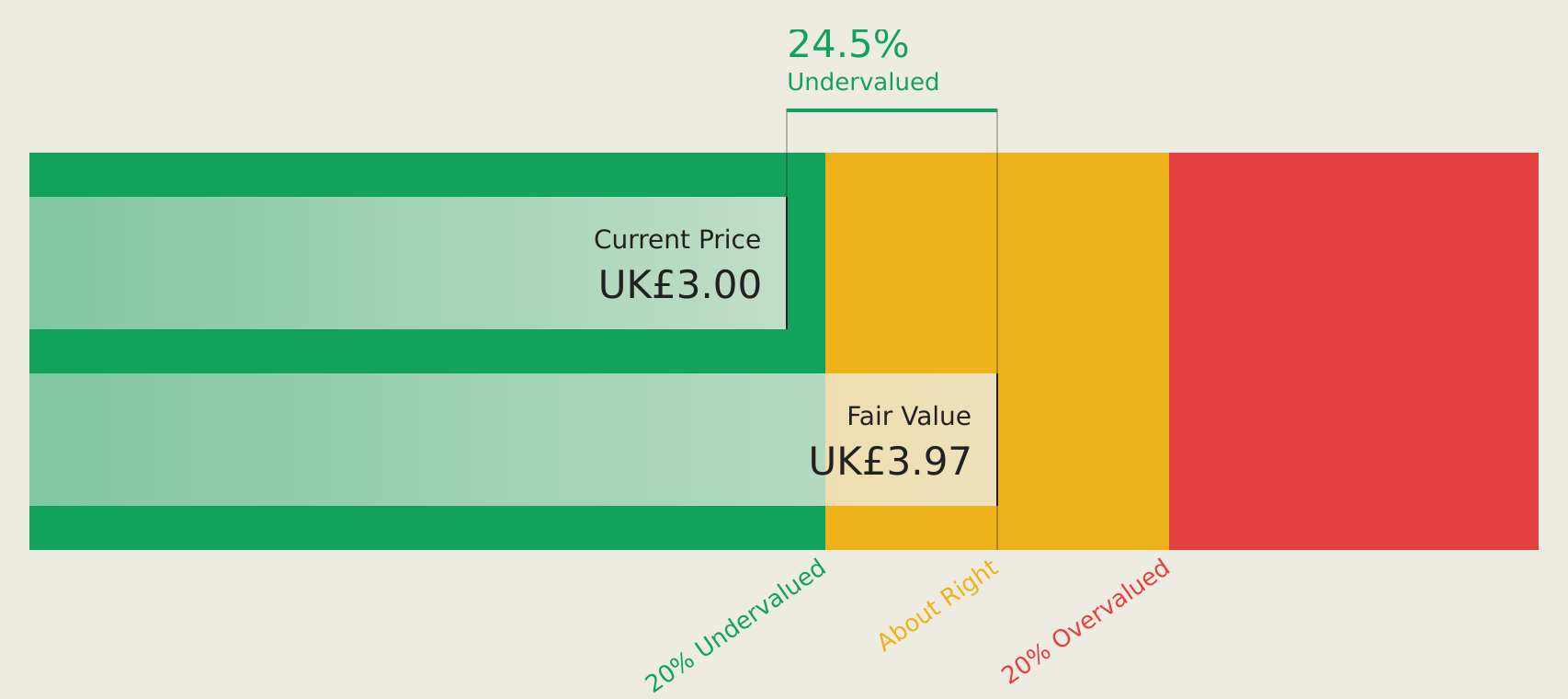

Griffin Mining (AIM:GFM)

Overview: Griffin Mining Limited is a mining and investment company focused on the exploration, development, and operation of mineral properties, with a market cap of £533.31 million.

Operations: The company's revenue is primarily derived from the Caijiaying Zinc Gold Mine, contributing $137.50 million.

Estimated Discount To Fair Value: 24.6%

Griffin Mining appears undervalued, trading 24.6% below its estimated fair value of £4.01 per share, with a current price of £3.02. The company reported a notable increase in net income to US$22.06 million for 2025, nearly doubling from the previous year, and earnings are forecast to grow significantly at 30.8% annually over the next three years—outpacing both revenue growth and the broader UK market's profit growth rate.

- The growth report we've compiled suggests that Griffin Mining's future prospects could be on the up.

- Dive into the specifics of Griffin Mining here with our thorough financial health report.

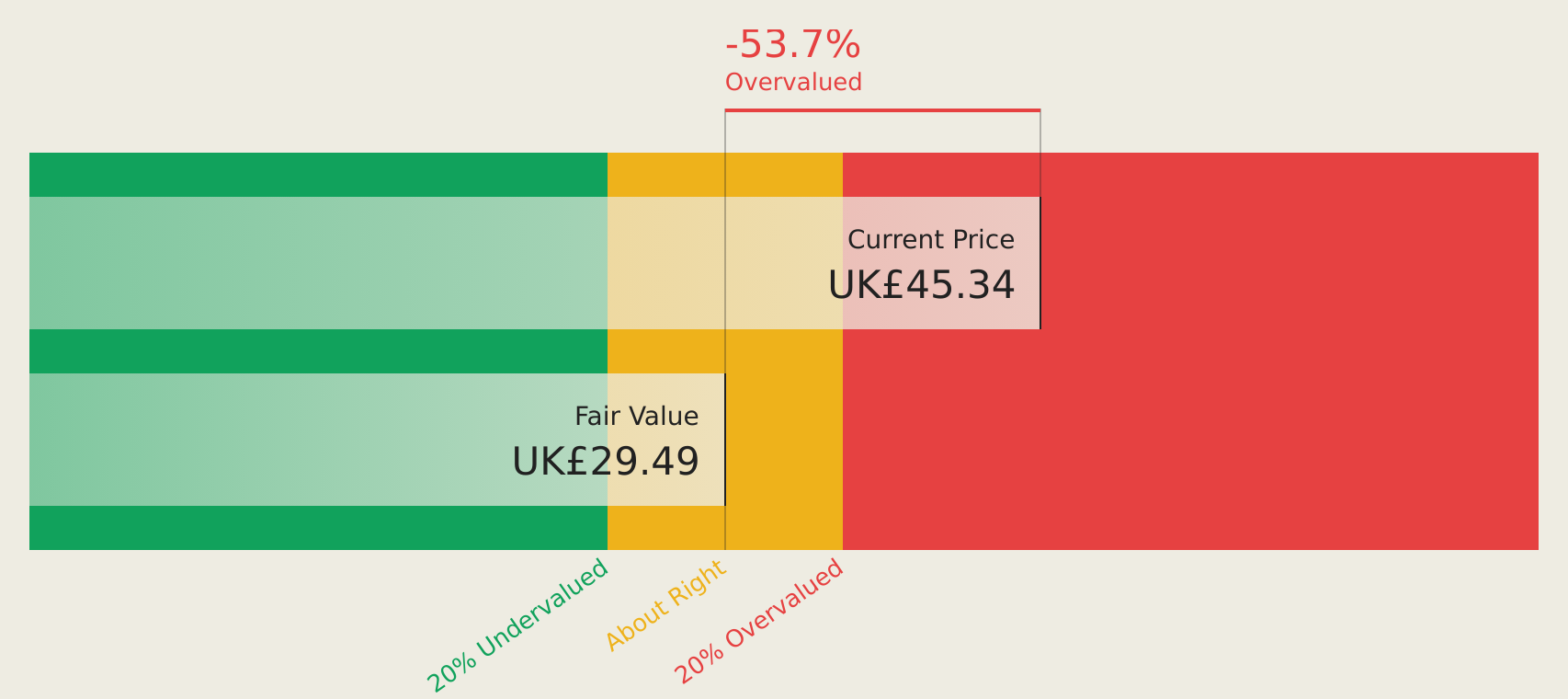

Computacenter (LSE:CCC)

Overview: Computacenter plc provides technology and services to corporate and public sector organizations across the United Kingdom, Germany, Western Europe, North America, and internationally, with a market cap of £4.79 billion.

Operations: The company generates revenue from its Computer Services segment, totaling £9.19 billion.

Estimated Discount To Fair Value: 10.3%

Computacenter is trading at £45.62, below its estimated future cash flow value of £50.86, suggesting it may be undervalued. Earnings are expected to grow at 12.1% annually, outpacing the UK market's 11.5% growth forecast, while revenue growth is also set to exceed the market average at 8.8%. Despite a decline in profit margins from last year, Computacenter was recently added to the FTSE 100 Index and approved a final dividend increase to 51 pence per share.

- Our comprehensive growth report raises the possibility that Computacenter is poised for substantial financial growth.

- Click here to discover the nuances of Computacenter with our detailed financial health report.

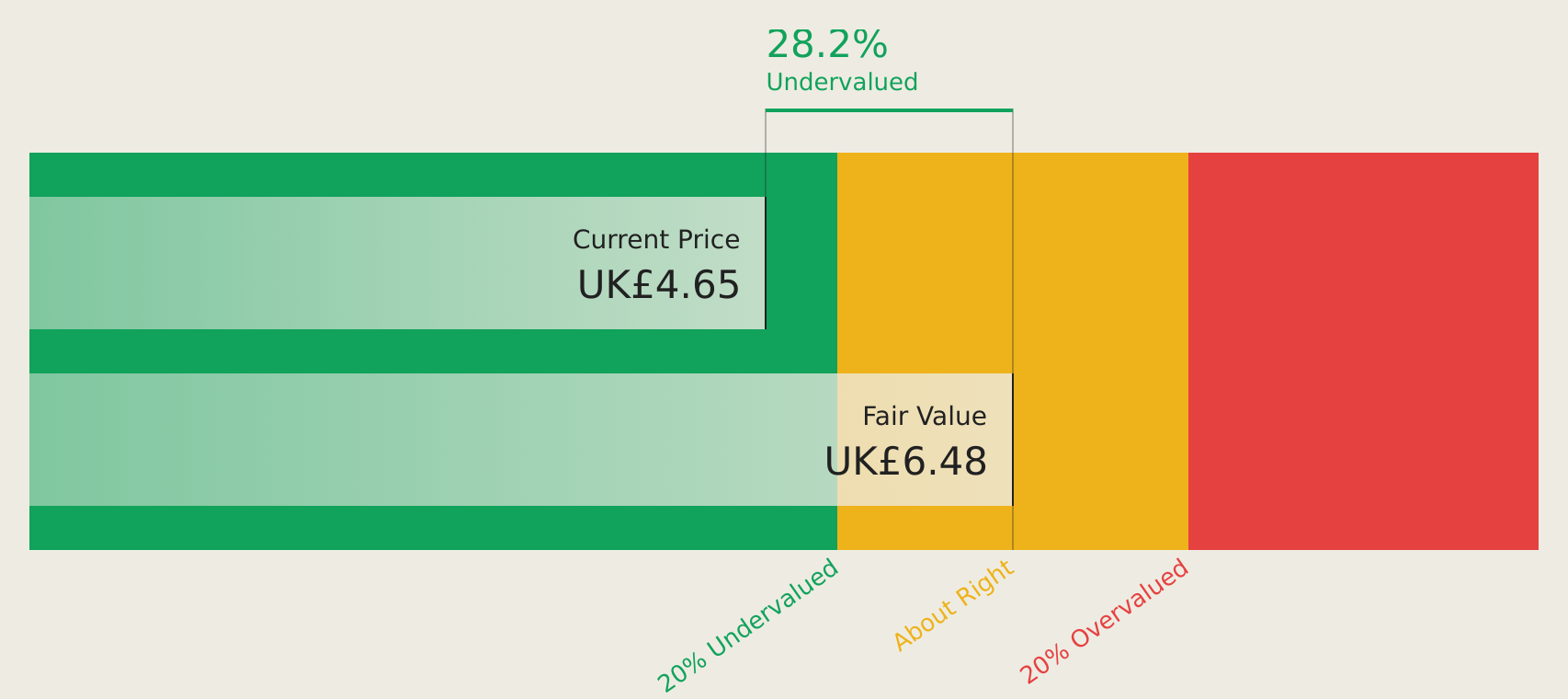

James Fisher and Sons (LSE:FSJ)

Overview: James Fisher and Sons plc is a marine services company with operations across the UK, Europe, the Middle East, Africa, the Americas, and the Asia-Pacific, and has a market cap of £232.23 million.

Operations: The company's revenue is derived from segments including Energy (£158.90 million), Defence (£88.80 million), and Maritime Transport (£147 million).

Estimated Discount To Fair Value: 28.8%

James Fisher and Sons, trading at £4.60, is below its estimated future cash flow value of £6.46, highlighting potential undervaluation. Forecasted earnings growth of 46.63% per year positions it for profitability within three years, surpassing average market growth expectations. Despite anticipated revenue expansion of 5.1% annually being modest compared to higher benchmarks, the company remains attractive due to trading at 28.8% below fair value estimates and recent strategic insights shared during its Analyst/Investor Day in May 2026.

- Our earnings growth report unveils the potential for significant increases in James Fisher and Sons' future results.

- Click here and access our complete balance sheet health report to understand the dynamics of James Fisher and Sons.

Taking Advantage

- Get an in-depth perspective on all 38 Undervalued UK Stocks Based On Cash Flows by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com