What Wesfarmers (ASX:WES)'s Bunnings Trade Integration Means For Shareholders

- Wesfarmers has recently expanded Bunnings by integrating Blackwoods and Workwear Group into a larger trade-focused unit, creating a broader platform in trade, safety equipment and industrial supplies to better serve commercial customers.

- This reshaping of Bunnings’ trade offering could deepen relationships with higher-frequency trade buyers, potentially increasing recurring activity across Wesfarmers’ broader retail and industrial ecosystem.

- We’ll now explore how this integration of Blackwoods and Workwear Group into Bunnings may influence Wesfarmers’ investment narrative and long-term positioning.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Wesfarmers Investment Narrative Recap

To own Wesfarmers, you need to believe its core retail brands can keep converting everyday traffic into reliable cash flow, while newer platforms in health, lithium and digital add incremental growth without eroding returns. The key near term swing factor remains cost inflation versus productivity gains, and the biggest risk is margin pressure across Bunnings and Kmart. The Blackwoods and Workwear integration into Bunnings looks directionally helpful for trade relevance, but not a material near term catalyst or risk on its own.

The June 1, 2026 announcement that Blackwoods and Workwear Group will be folded into Bunnings from July 2026 is the most relevant backdrop here. It connects directly with the existing catalyst around omnichannel and commercial capability across Bunnings, Kmart and Officeworks, potentially reinforcing Wesfarmers’ ability to deepen trade relationships and support more consistent activity, even as Australian SMEs and the residential building sector remain soft.

Yet against this stronger trade story, investors should be aware that...

Read the full narrative on Wesfarmers (it's free!)

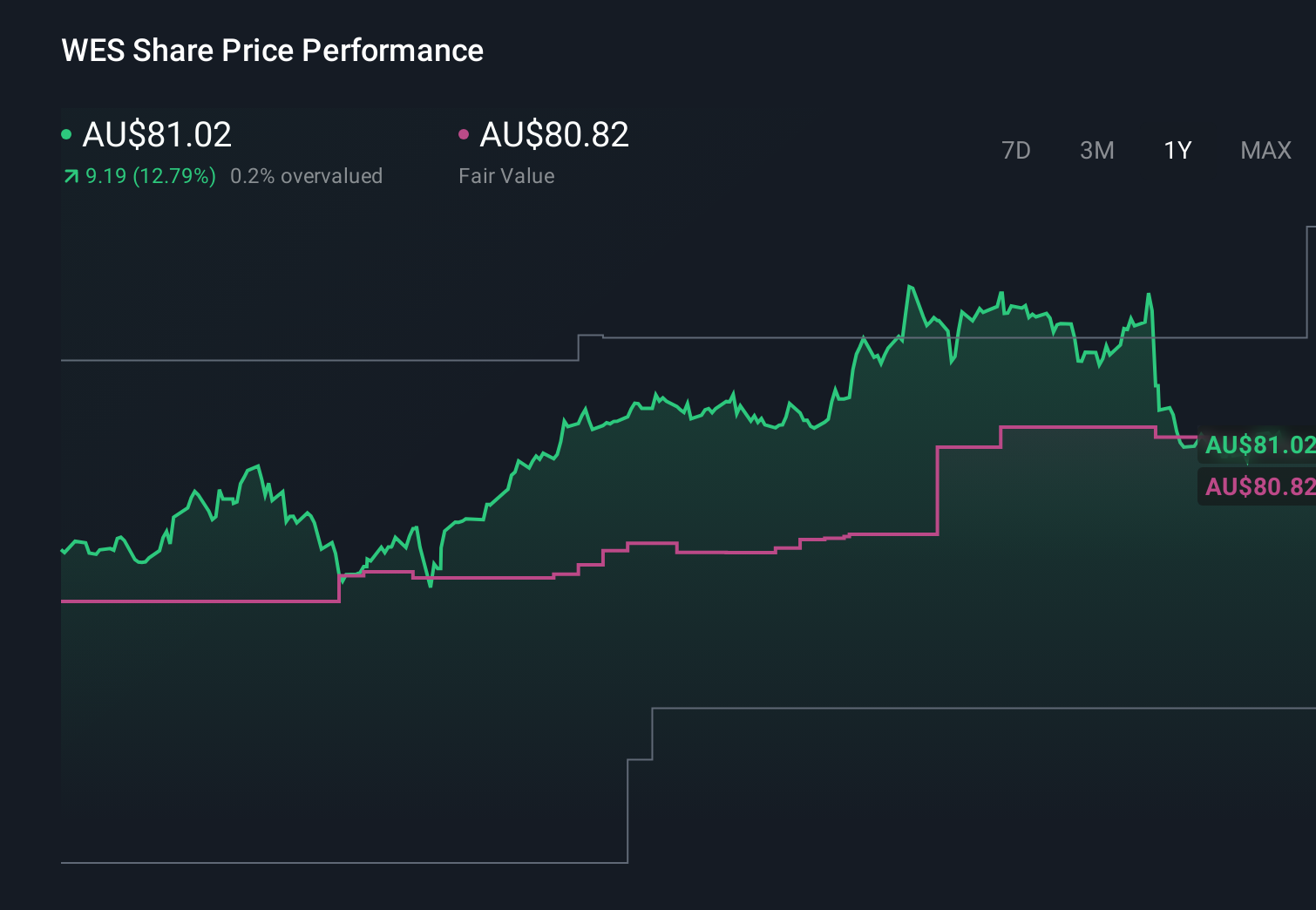

Wesfarmers' narrative projects A$52.8 billion revenue and A$3.5 billion earnings by 2029. This requires 4.4% yearly revenue growth and about A$0.4 billion earnings increase from A$3.1 billion today.

Uncover how Wesfarmers' forecasts yield a A$76.16 fair value, a 17% downside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already assuming Wesfarmers could lift revenue to about A$54.7 billion and earnings to around A$3.8 billion by 2029, so if you worry about rising labor and compliance costs squeezing margins, this new Bunnings trade move might either ease those fears or sharpen them, depending on how you think it changes Wesfarmers’ cost base and pricing power.

Explore 7 other fair value estimates on Wesfarmers - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Wesfarmers research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wesfarmers research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wesfarmers' overall financial health at a glance.

No Opportunity In Wesfarmers?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com