Peloton Interactive (PTON) Could Be 23% Undervalued As Its Rebound Tests Fair Value

Peloton Interactive (PTON) is back in focus for investors after fresh performance data highlighted its mix of connected fitness hardware and subscription revenue, prompting a closer look at recent returns and profitability trends.

See our latest analysis for Peloton Interactive.

At a share price of US$6.08, Peloton Interactive has seen short term momentum pick up, with a 30 day share price return of 9.55% and 90 day share price return of 27.46%. However, the 1 year total shareholder return is still down 5.59% and the 5 year total shareholder return is down 94.87%. This points to a stock where recent optimism is emerging against a much weaker long term record and a still cautious view of risk.

If Peloton’s recent bounce has you thinking about other opportunities, this could be a good moment to see what else is moving and check out 18 top founder-led companies

Peloton Interactive’s share price rebound and the wide gap between US$6.08, analyst targets and some intrinsic value estimates raise a practical question: is the recent move already rich or still below fair value?

Most Popular Narrative: 23% Undervalued

Peloton Interactive’s most followed narrative puts fair value at $7.88 per share compared with the last close at $6.08, framing the current rebound as still below that reference point while stressing execution, competition, and profitability as key swing factors.

Peloton is leveraging advanced technologies, including AI-powered personalized coaching and human-driven community features, to broaden its offerings from cardio into holistic wellness (strength, sleep, stress, nutrition), which aligns with growing global health consciousness and should support future subscription revenue growth and higher engagement/churn reduction.

Curious what kind of revenue mix, margin lift, and earnings profile this wellness and subscription push assumes, and how that lines up with the implied future valuation multiple? The narrative sets out a detailed earnings path and required pricing for those cash flows that is worth checking against your own expectations.

Result: Fair Value of $7.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Peloton Interactive’s story also hinges on reversing declining hardware and subscription trends, as well as holding its ground against intense competition that could pressure pricing and margins.

Find out about the key risks to this Peloton Interactive narrative.

Another View on Peloton Interactive’s Valuation

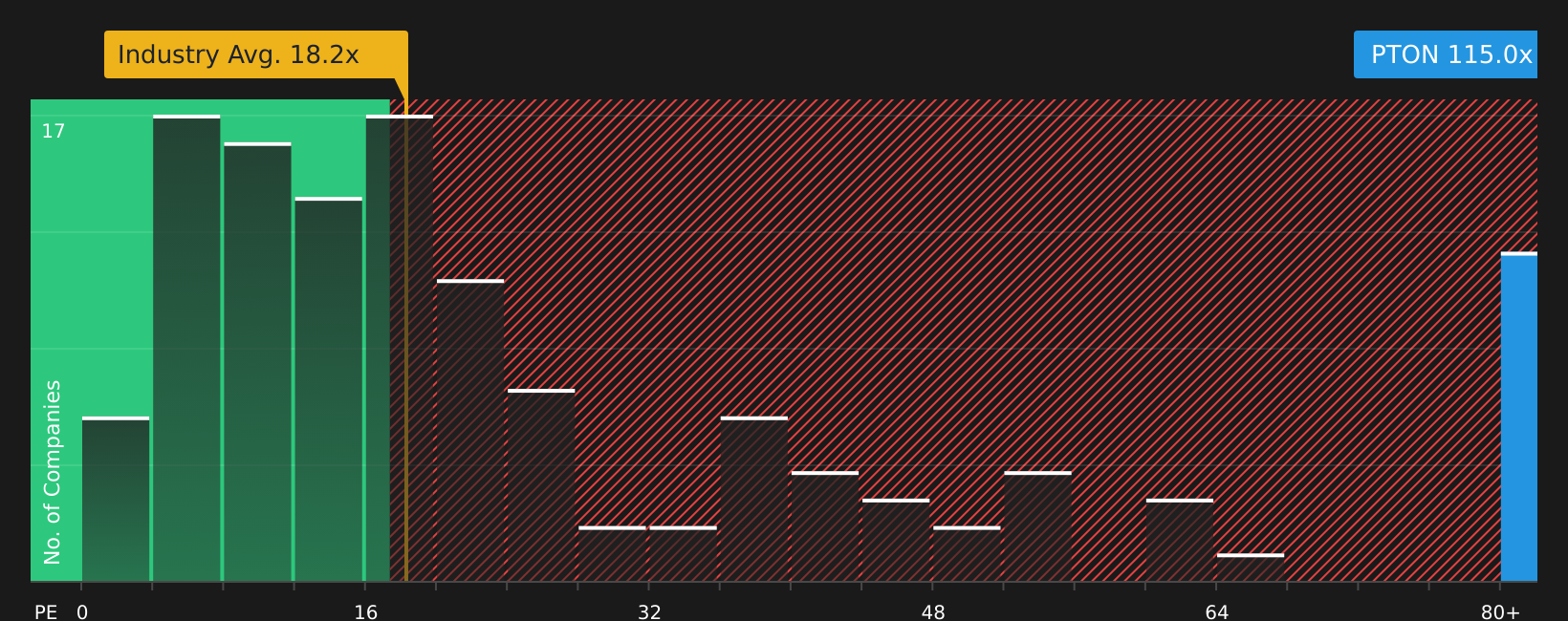

The earlier narrative leans on future earnings and analyst price targets, but the current P/E ratio of 113.5x tells a different story. Compared with a fair ratio of 30.9x, the Global Leisure industry at 18.3x and peers at 33.7x, Peloton Interactive screens expensive, which raises the question of how much optimism is already priced in.

For a closer look at what this gap could mean in practice, including how the ratio might move toward the fair ratio over time, check the valuation breakdown in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Balancing Peloton Interactive’s mixed share price history with the latest valuation signals is not straightforward. It makes sense to move fast and check the details yourself, weighing both sides of the story against your own expectations with the help of the 3 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Peloton Interactive?

Do not stop with Peloton Interactive. Use this momentum to widen your watchlist, compare different setups, and spot opportunities you would regret missing later.

- Target potential value opportunities early by scanning 46 high quality undervalued stocks, which combines quality fundamentals with prices that sit below many investors’ radars.

- Strengthen your focus on balance sheet resilience by reviewing the solid balance sheet and fundamentals stocks screener (47 results) so you can filter for companies with robust financial footing.

- Hunt for under followed stories with solid numbers by running the screener containing 20 high quality undiscovered gems before other investors catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com