How Investor Rotation Into AI Monetization Plays Could Reframe Marqeta’s (MQ) Embedded Finance Narrative

- Earlier today, payments software company Marqeta attracted strong buying interest as investors shifted away from AI infrastructure chipmakers toward enterprise software names seen as benefiting from AI monetization trends.

- This rotation highlighted Marqeta’s positioning at the intersection of software and payments, where its platform is viewed as a way for customers to turn AI-driven financial services into revenue-generating products.

- We’ll now examine how this renewed focus on AI monetization within software affects Marqeta’s existing investment narrative around payments and embedded finance.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

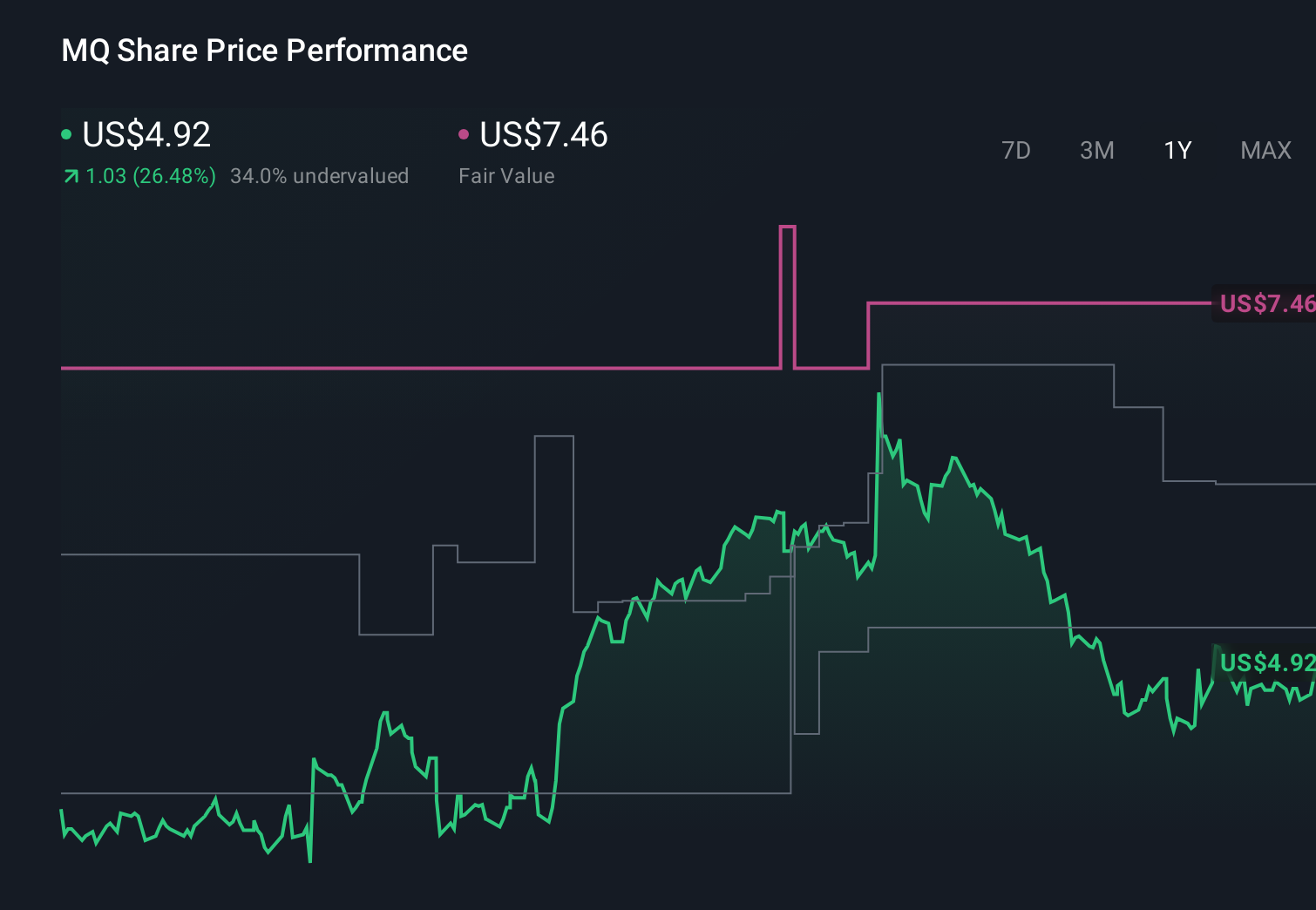

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe that card-based embedded finance and its API platform can keep attracting volume as digital payments grow, while the company manages customer concentration and rising competition. Today’s rotation into AI monetization stories may support sentiment around its AI-enabled fraud and decisioning tools, but it does not materially change the near term catalyst of proving consistent profitability or the key risk from reliance on a few large customers.

In this context, Marqeta’s March launch of AI-enabled risk scoring within its Real-Time Decisioning suite stands out. It ties directly into the AI monetization narrative behind today’s move, as investors look for software platforms that can help clients reduce fraud and false declines and potentially justify premium pricing. This type of value-added service sits at the heart of the thesis that Marqeta can deepen customer relationships while working toward more durable margins.

Yet against this improving AI story, investors should be aware of how concentrated Marqeta still is in a single major customer and how that could...

Read the full narrative on Marqeta (it's free!)

Marqeta's narrative projects $969.2 million revenue and $73.1 million earnings by 2029. This requires 14.2% yearly revenue growth and about a $70.9 million earnings increase from $2.2 million today.

Uncover how Marqeta's forecasts yield a $5.24 fair value, a 68% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming revenue of about US$941.4 million and earnings of just US$34.4 million by 2029, which contrasts sharply with the recent enthusiasm around AI powered services and shows how differently you and others might assess Marqeta’s potential path from here.

Explore 3 other fair value estimates on Marqeta - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com