Chugoku Marine Paints (TSE:4617) Lifted Full Year Guidance, Is It Still 30% Below Fair Value?

Chugoku Marine Paints (TSE:4617) has updated its full year outlook after earlier uncertainty around Middle East related raw material risks. The company is providing detailed forecasts supported by firm marine and industrial coatings demand and ongoing selling price adjustments.

See our latest analysis for Chugoku Marine Paints.

Chugoku Marine Paints’ clearer guidance comes after a mixed share price pattern, with the stock up 7.72% over 30 days and 13.26% over 90 days, while year to date it is down 19.33%, set against a 39.42% 1 year total shareholder return and very strong multi year total shareholder returns.

If this guidance update has you thinking about where else to put fresh capital to work, this could be a moment to scan 12 top founder-led companies

For Chugoku Marine Paints, the share price swings and the more detailed guidance suggest different explanations: one points to a stronger grip on the underlying business, and the other to changing sentiment. Which is driving the current valuation setup?

Preferred P/E of 16.4x: Is it justified?

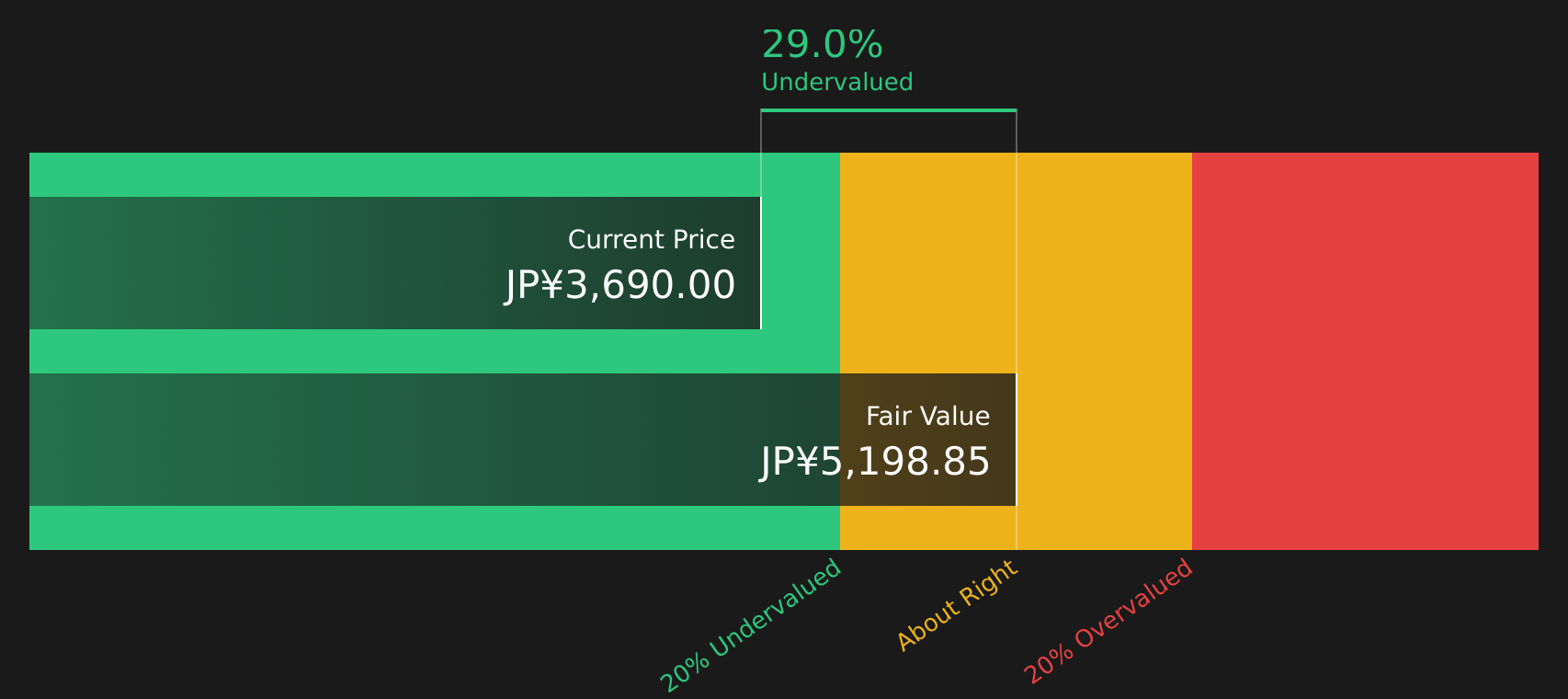

For Chugoku Marine Paints, the signals from its valuation checks point to a stock that screens as undervalued relative to some benchmarks, even though the P/E ratio of 16.4x is higher than the JP Chemicals industry average of 13.2x.

The P/E ratio compares the share price to earnings per share and is a common way to gauge how much investors are paying for current profits. In this case, the company is assessed as good value based on its P/E of 16.4x relative to both an estimated fair P/E of 16.4x and the peer average of 18.4x. It is also trading at a 30.2% discount to an estimated fair value and below an estimated future cash flow value of ¥5,200.94 per share.

The tension for investors is clear. On one side, the stock is flagged as expensive versus the broader JP Chemicals industry, where the average P/E is 13.2x. On the other side, it screens as good value versus peers and internal fair value estimates, suggesting the current P/E level could be a point the market eventually converges toward if forecasts and cash flow assumptions hold.

Explore the SWS fair ratio for Chugoku Marine Paints

Result: Preferred multiple of 16.4x P/E (ABOUT RIGHT)

However, Chugoku Marine Paints still faces risks such as renewed raw material disruption and any slowdown in marine or industrial coatings demand, which could challenge current expectations.

Find out about the key risks to this Chugoku Marine Paints narrative.

Another View: What Does the SWS DCF Model Say?

Alongside the P/E checks for Chugoku Marine Paints, the SWS DCF model offers a different perspective, with an estimated future cash flow value of ¥5,200.94 per share compared with the current ¥3,630, implying the stock is trading at a 30.2% discount. Is the market too cautious here?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Chugoku Marine Paints for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 20 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

So with Chugoku Marine Paints showing both potential rewards and clear risks, are you leaning cautious or optimistic? Act while the information is fresh, review the data in detail, and weigh both sides by checking the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Chugoku Marine Paints?

If Chugoku Marine Paints has sharpened your focus, do not stop here. Use this moment to widen your watchlist with targeted ideas built from real fundamentals.

- Spot potential bargains early by scanning screener containing 57 high quality undiscovered gems that pair solid underlying metrics with limited market attention.

- Build a core watchlist from solid balance sheet and fundamentals stocks screener (37 results) so you are focusing on companies with stronger financial footing when conditions get tougher.

- Lower overall portfolio stress by assessing 55 resilient stocks with low risk scores that score well on resilience factors many investors overlook until it is too late.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com