3 Japanese Stocks Trading Below Fair Value on Cash Flow Estimates

With inflation worries, shifting interest rate expectations and energy driven price swings back in focus, many investors are looking for shelter in companies where cash flows do most of the talking. The Undervalued Stocks Based On Cash Flows screener targets businesses that the SWS DCF valuation suggests are trading below a fair value estimate, even as global headlines keep volatility high. By focusing on cash flow potential rather than hype or short term momentum, this approach can help you concentrate on what you are paying versus what you are getting. Below, find 3 stocks from this screener that stand out right now.

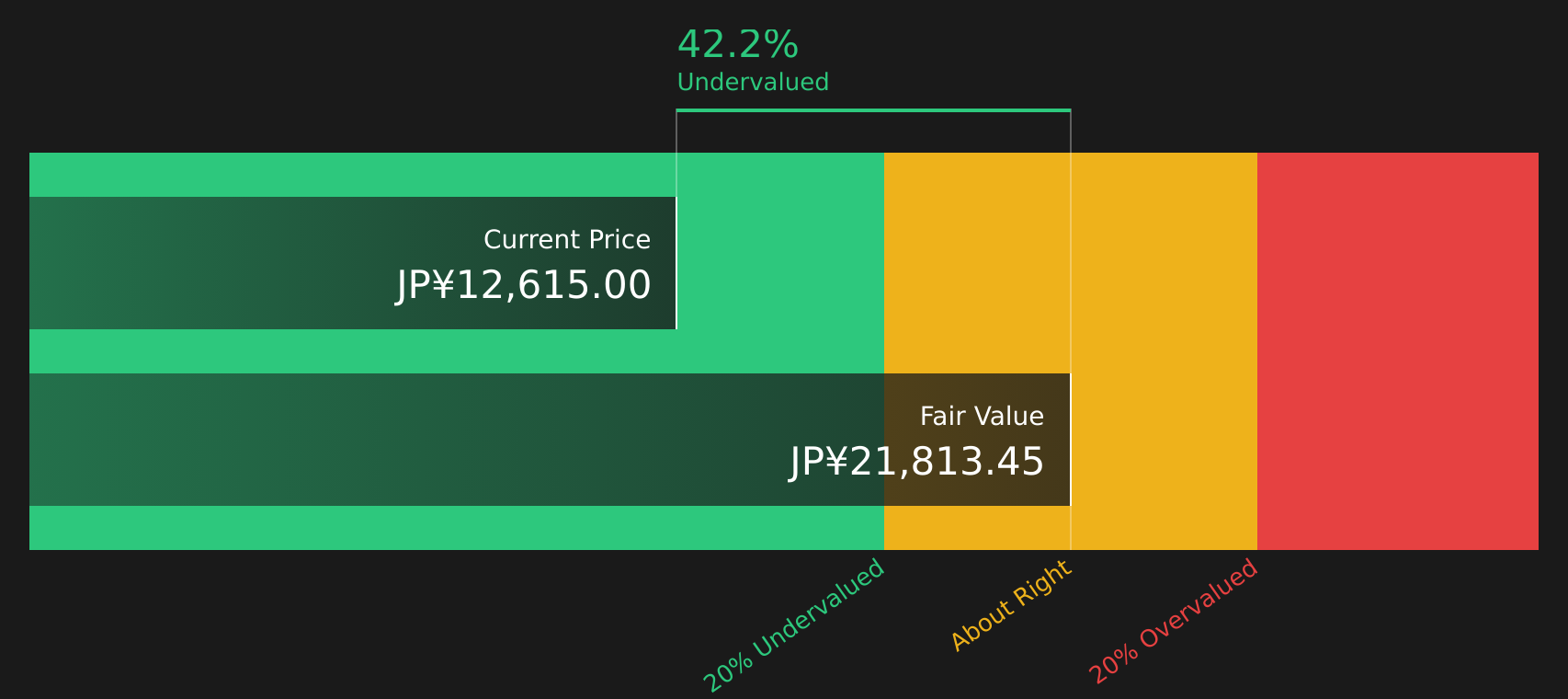

Recruit Holdings (TSE:6098)

Overview: Recruit Holdings is a Tokyo based HR and marketing solutions group that runs online job platforms, global staffing services and lifestyle marketplaces that connect people with work, housing, travel, dining and other everyday services. Through its HR Technology, Staffing and Marketing Matching Technologies segments, the company links job seekers, employers and consumers across Japan, the United States and other international markets.

Operations: Recruit Holdings generates most of its revenue from Staffing at ¥1.7t, followed by HR Technology at about ¥1.5t and Marketing Matching Technologies at about ¥565b, with Japan as its largest region alongside substantial contributions from the United States and other overseas markets.

Market Cap: ¥17.6t

Recruit Holdings may appeal to investors who focus on cash flow supported growth, with the HR Technology segment investing heavily in AI and automation to improve matching efficiency, while management focuses on cost control and share buybacks. Earnings and margins have been improving, guidance points to higher revenue and net income, and analysts see potential for further upside if profitability continues to trend higher. At the same time, weakness in global staffing demand, slower adoption of new platforms like Indeed PLUS in Japan and reliance on external funding for liabilities introduce risks, which is why a closer look at how Recruit balances growth investments, capital returns and competitive threats can be important.

Recruit Holdings is pouring resources into AI, automation and buybacks, yet the balance between growth, cash flows and staffing risks is easy to misread, so walk through the 3 key rewards and 1 important warning sign

JX Advanced Metals (TSE:5016)

Overview: JX Advanced Metals is a Japan based materials company that supplies copper and rare metal products used in semiconductors, electronics and industrial applications, from sputtering targets and copper foil to specialty powders, catalysts and recycling services. Its products feed into semiconductor fabrication, information and communication technology hardware and broader manufacturing supply chains around the world.

Operations: JX Advanced Metals generates most of its revenue from Base Materials at ¥407,877m, Information and Communication Materials at ¥318,744m and Semiconductor Materials at ¥177,195m, with smaller contributions from Others and unallocated adjustments.

Market Cap: ¥3.7t

JX Advanced Metals provides exposure to materials that sit at the heart of semiconductors and electronics, supported by forecast earnings growth of 14.85% per year and an 11.8% net margin that currently sits above the prior year level. The stock screens as undervalued against the Simply Wall St cash flow estimate, even though the P/E is higher than many Metals & Mining peers. This suggests investors are already paying up for its quality of earnings. At the same time, a 15.4% ROE, funding that relies on external borrowing and a highly volatile share price keep risk firmly on the table. Recent large buybacks and index inclusions add another layer that is worth unpacking before making a call.

JX Advanced Metals sits at the crossroads of semiconductor materials and premium valuation, with investors paying up for quality earnings and cash flow support. Get the full story behind that higher P/E, recent buybacks and volatility in the analysis report for JX Advanced Metals

Murata Manufacturing (TSE:6981)

Overview: Murata Manufacturing is a Japan based electronics company that makes ceramic capacitors, sensors, batteries and communication modules that sit inside smartphones, cars, data centers, wearables and industrial equipment worldwide.

Operations: Murata Manufacturing generates most of its revenue from Components at ¥1.2t and Devices and Modules at ¥656.0b, with smaller contributions from Others at ¥69.7b and Elimination/Corporate adjustments of ¥70.1b.

Market Cap: ¥16.5t

Murata Manufacturing is involved in key themes such as AI servers, smartphones, automotive electronics and IoT. Earnings and revenue are forecast to grow at double digit rates over the next few years, and analysts have recently lifted their estimates. A large share buyback program of up to ¥150b and a higher dividend indicate management’s confidence in future cash flows, while new sensor and automotive grade capacitor launches are intended to support that growth. However, the company currently trades at a very high P/E multiple, has experienced historically soft earnings growth and has shown a volatile share price, so investors are effectively paying for quality and momentum. Assessing how the company’s cash flow prospects compare with these risks is important when considering whether the current valuation appears reasonable.

Murata Manufacturing’s double digit growth forecasts and premium P/E hint at a story that is still unfolding, but the real question is how that growth stacks up against cash flow and volatility risks in the analyst forecasts for Murata Manufacturing

The three stocks covered here are only a starting point, with the full Undervalued Stocks Based On Cash Flows screener surfacing 54 more companies that pair discounted DCF valuations with cash flow stories that could be just as compelling as Recruit Holdings, JX Advanced Metals and Murata Manufacturing. Identify and analyze the specific catalysts that matter to you, from cash flow durability to balance sheet strength, by running the Undervalued Stocks Based On Cash Flows screener.

Take Control of Your Investment Journey

If Recruit Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves

Fresh stock ideas can start breaking out while most investors are still watching yesterday’s winners. Use these under the radar picks before their momentum is fully caught, and consider acting sooner rather than later.

- Target reliable income streams by scanning companies in the 43 dividend fortresses that focus on keeping payouts flowing while prices and yields still look appealing.

- Spot potential future leaders by reviewing the 57 high quality undiscovered gems that highlight quality businesses still flying under most investors’ radar for now.

- Focus on durability first by checking the list of solid balance sheet and fundamentals (37 results) and quickly filter for companies built to hold up when conditions get tougher.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com