NS Solutions (TSE:2327) Tightens Parent Deposit Rules, Is The Valuation Already Full?

NS Solutions (TSE:2327) is back in focus after shareholders approved amendments to its Articles of Incorporation to restrict deposits with its parent company and to require more detailed disclosure on related deposit terms and policies.

See our latest analysis for NS Solutions.

The governance changes around deposits with its parent sit against a mixed price backdrop for NS Solutions, with a 30 day share price return of 19.79% contrasting with a year to date share price decline of 12.06% and a 3 year total shareholder return of 104.08%. This suggests that longer term holders have still seen strong value creation, even as shorter term momentum has been uneven.

If you are weighing how this kind of corporate governance shift could matter elsewhere in your portfolio, it may be a good moment to scan for other opportunities using the 11 top founder-led companies

Bulls will point to NS Solutions’ governance clean up and long term shareholder returns, while bears will flag the parent deposit issue and recent share price weakness. How does the current valuation stack up against that tug of war?

Preferred P/E of 22.8x for NS Solutions: Is it justified?

On the numbers, NS Solutions is trading on a P/E of 22.8x, which sits above several benchmarks and raises a question about how much future earnings strength is already reflected in the ¥3,850 share price.

The P/E multiple compares the current share price with earnings per share, so a higher ratio usually means investors are paying more today for each unit of earnings. For an IT solutions provider like NS Solutions, this often reflects expectations around future profit growth, the resilience of its client base and the perceived quality of recurring work such as outsourcing, cloud and data center services.

In this case, the current P/E of 22.8x is higher than the JP IT industry average of 15.5x, the peer average of 19.6x and the estimated fair P/E of 19.9x. This puts the stock at a premium to sector peers and above a level the fair ratio suggests the market could eventually move towards if sentiment or growth expectations shift.

Explore the SWS fair ratio for NS Solutions

Result: Price-to-earnings of 22.8x (OVERVALUED)

However, NS Solutions still faces risks if earnings do not support a 22.8x P/E, or if governance concerns around deposits with its parent company resurface.

Find out about the key risks to this NS Solutions narrative.

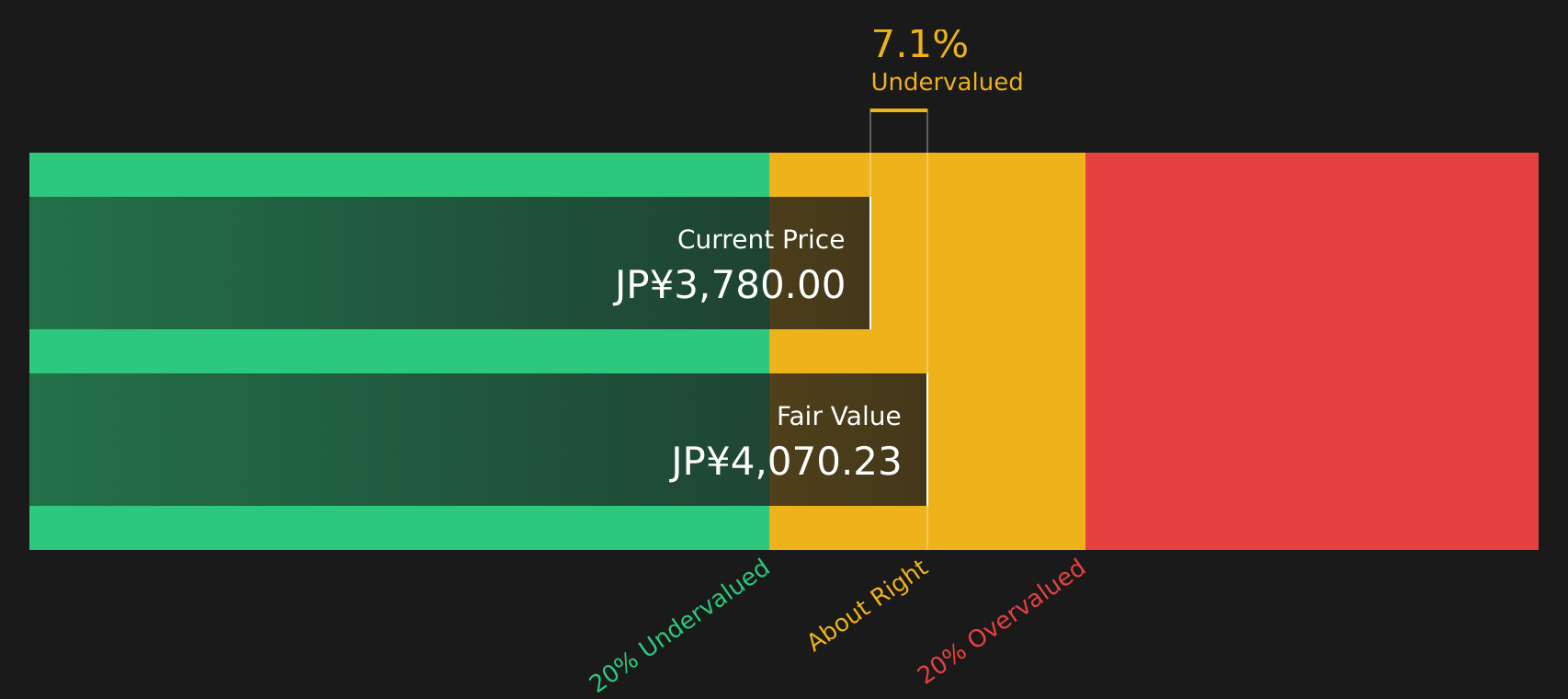

Another View on NS Solutions: DCF Points the Other Way

While the 22.8x P/E suggests NS Solutions is on the expensive side, the SWS DCF model tells a different story, with an estimated value of ¥4,208 per share compared with today’s ¥3,850. If cash flows support that, is the premium multiple really as stretched as it looks?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NS Solutions for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 19 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With NS Solutions presenting both risks and rewards in this review, use the data to respond promptly and form your own view, beginning with the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond NS Solutions?

NS Solutions might be high on your watchlist, but the next opportunity in your portfolio could come from stocks you have not reviewed yet.

- Spot potential value candidates before the crowd by checking companies highlighted in the 19 high quality undervalued stocks.

- Strengthen your defensive side by focusing on companies with the solid balance sheet and fundamentals stocks screener (38 results).

- Target resilient income streams by searching for companies in the 44 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com