Stellantis (BIT:STLAM) Stock May Be Reasonable As New Model Push Builds

Stellantis stock is coming off a difficult stretch, with the share price down about 65.0% over the past three years. Its current valuation checks still suggest the market may be pricing it cheaply relative to fundamentals.

- The roughly 65.0% share price decline over three years signals that sentiment has been weak for a prolonged period and that expectations for Stellantis have reset significantly.

- New product launches and technology partnerships can support expectations for future cash flows, while ongoing recall and inventory challenges may limit how much investors are willing to pay for that potential.

- Stellantis currently passes most of Simply Wall St’s valuation checks, with 5 out of 6 suggesting the stock looks cheap compared to several common yardsticks.

The issue now is whether Stellantis’ weak long term share performance already reflects these risks, or if today’s pricing still offers enough margin of safety to appeal to value focused investors.

Find out why Stellantis' -41.4% return over the last year is lagging behind its peers.

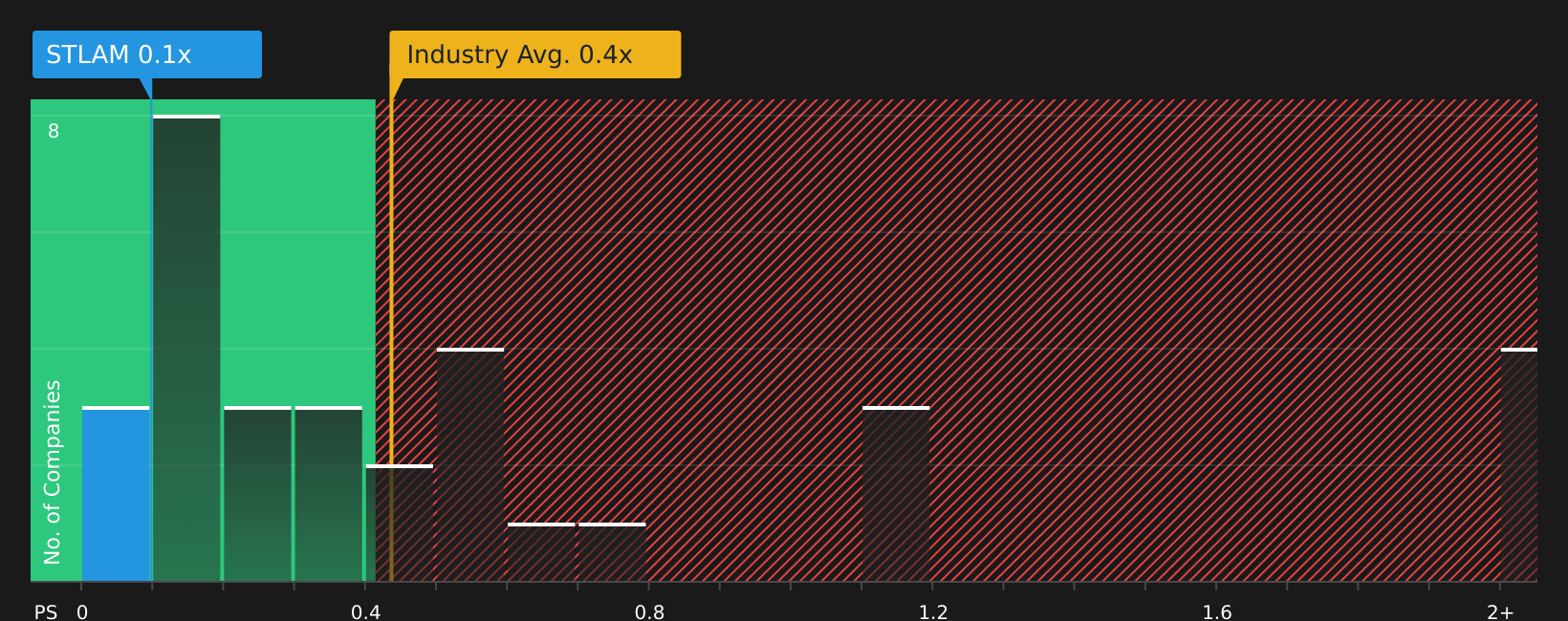

Does Stellantis Look Undervalued on Sales?

The P/S ratio is a useful lens for Stellantis because it ties the stock price directly to the revenue base that supports its many brands and regions. Stellantis trades at a P/S of about 0.1x, which is far below the Auto industry average of 0.6x and well under the broader peer group at roughly 2.6x.

The more tailored fair P/S ratio for Stellantis is 0.4x, based on factors such as its size, margins, sector and risk profile. Compared with the current 0.1x, that suggests the stock is trading at a steep discount to what this model indicates might be reasonable, even after accounting for issues like recalls, U.S. inventory concerns and competition. Despite recent headlines around cost pressures and delays in expected savings, the current P/S still values Stellantis as if its revenue stream deserves a much lower valuation than peers with similar business characteristics.

On the P/S multiple, Stellantis stock appears undervalued relative to both its tailored fair ratio and the wider Auto sector.

See what the numbers say about this price — find out in our valuation breakdown.

The Stellantis Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Stellantis pick up where this valuation puzzle leaves off by spelling out which paths for growth, margins and earnings would need to play out for Stellantis' stock to be worth meaningfully more or less than today's price. Each narrative links its number to a clear view of how Stellantis' growth, profitability and risks could evolve, giving you a reference point you can revisit as new information comes through.

Community views on Stellantis sit far apart, with some investors focused on recovery potential and others fixated on execution risks and margin pressure.

Bull case: 34% undervalued

"Sequential improvements in operating margins and halved cash flow outflows from 2H 2024 to 1H 2025, combined with a robust liquidity position, indicate underlying operational progress that could drive higher future net margins and cash generation as near-term headwinds subside…"

Read the full Bull Case to see why Stellantis could be undervalued

Bear case: 25% overvalued

"Stellantis' heavy reliance on internal combustion engine vehicles, particularly in North and Latin America, puts it at a structural disadvantage as emissions regulations and consumer preferences shift rapidly toward electric vehicles worldwide. This will likely continue to put downward pressure on revenue growth and operating margins as ICE sales erode faster than the company can scale profitable EVs…"

Read the full Bear Case to see why Stellantis could be overvalued

Do you think there's more to the story for Stellantis? Head over to our Community to see what others are saying!

The Bottom Line

For Stellantis, the core question is whether a low P/S multiple and strong overall valuation checks reflect undue pessimism or a realistic appraisal of its recall, inventory and transition risks. The stock currently screens as undervalued on market multiples, but that discount only helps if Stellantis can protect margins and turn its product and technology plans into resilient cash flows. From here, the debate largely comes down to whether current concerns about execution and the shift away from internal combustion vehicles are already fully reflected in the price, or whether they point to a value trap that deserves to stay discounted.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com