Is Hershey’s Texture-Driven REESE’S PIECES Relaunch a Meaningful Shift in HSY’s Snacking Strategy?

- Earlier this month, The Hershey Company introduced REESE'S PIECES with Chocolate Cookie in the U.S., the brand's first new REESE'S PIECES product in a decade, featuring a crispy chocolate cookie center, creamy peanut butter flavor and the classic candy shell.

- This long-awaited twist on a core brand highlights Hershey's emphasis on texture-rich snacking and its focus on extending the REESE'S franchise into more everyday snacking occasions.

- Next, we'll examine how this long-awaited REESE'S PIECES texture-focused innovation may influence Hershey's broader investment narrative and growth outlook.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

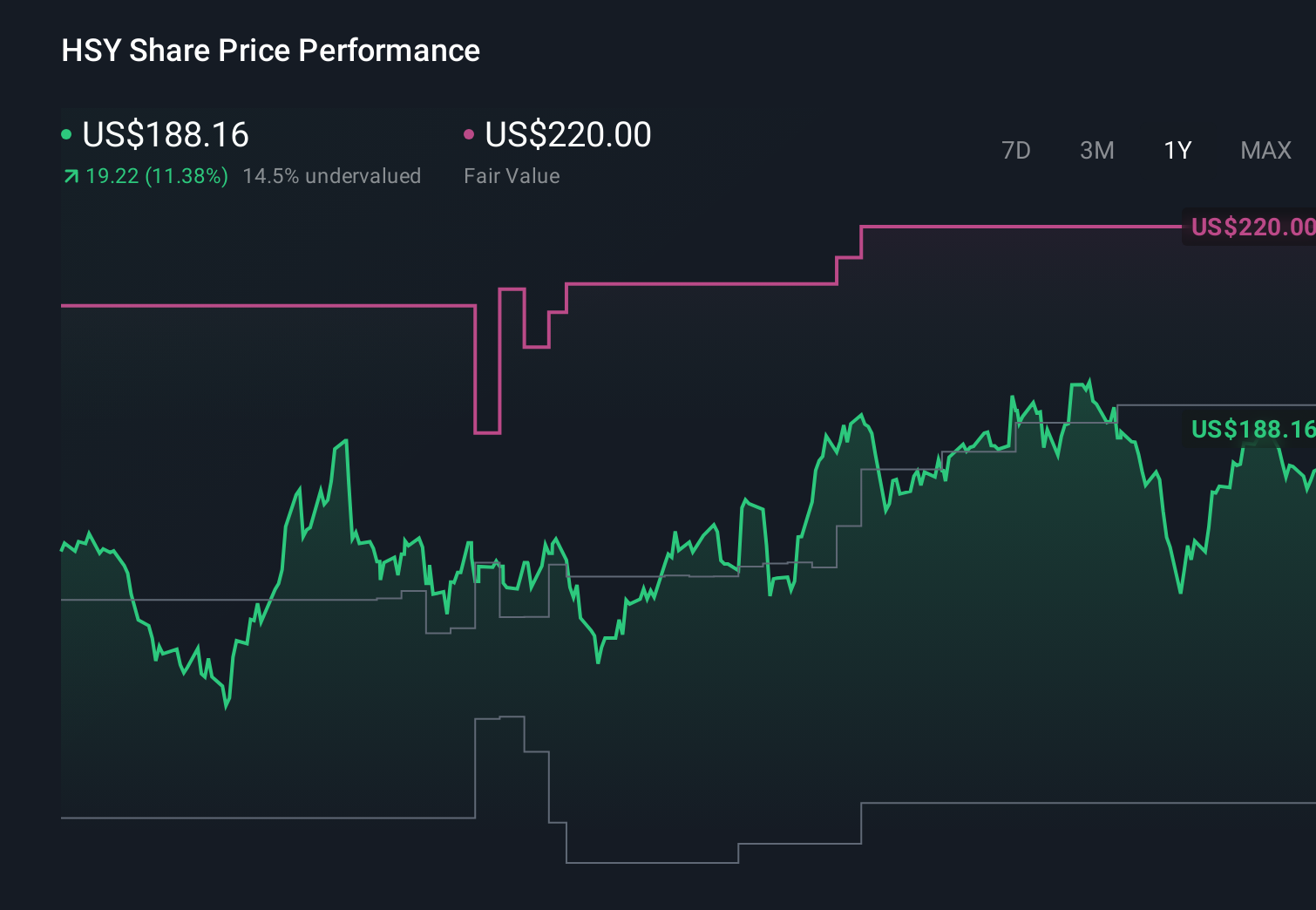

Hershey Investment Narrative Recap

To own Hershey, you generally need to believe its brands can keep earning a price premium despite higher input costs, softer consumers, and heavier competition. The new REESE'S PIECES with Chocolate Cookie fits the near term catalyst around innovation and price pack architecture, but on its own it does not change the key risk profile of margin pressure from cocoa prices and potential tariff costs.

The most relevant recent announcement here is the ONE x Reese's Peanut Butter Chocolate Layered Protein Bar, which also leans into texture and on the go snacking. Together with this new REESE'S PIECES launch, it underscores Hershey's push to stretch its brands across more snacking occasions, which could support the innovation driven growth investors are watching while cost and earnings pressures remain in focus.

Read the full narrative on Hershey (it's free!)

Hershey's narrative projects $13.1 billion revenue and $2.1 billion earnings by 2029. This requires 3.0% yearly revenue growth and about a $1.0 billion earnings increase from $1.1 billion today.

Uncover how Hershey's forecasts yield a $216.45 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Yet while some analysts see cocoa cost relief and category strength lifting earnings toward about US$2.5 billion by 2029, others worry that health trends and regulation could still...

Explore 5 other fair value estimates on Hershey - why the stock might be worth just $175.32!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hershey research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hershey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hershey's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com