Is Krystal Biotech (KRYS) Too Expensive After A 440% Return?

Krystal Biotech’s stock has delivered a very large 439.7% return over the past five years, yet its current checks lean expensive, with a low value score and the market multiples suggesting investors are paying a premium for that track record.

- Over five years, shareholders have seen a 439.7% return, which puts extra focus on whether today’s price still reflects a reasonable entry point.

- Expectations for Krystal Biotech’s future revenue and cash flow can support a premium valuation, but any disappointment in execution or clinical and regulatory progress may weigh heavily on what investors are willing to pay.

- The company only passes 2 of 6 valuation checks, which points to Krystal Biotech not being a clear bargain on the broader tests of value at current levels, according to its value score of 2.

The issue now is whether Krystal Biotech’s recent share price strength has moved the stock beyond a reasonable valuation or still leaves room for further upside based on its fundamentals.

Is Krystal Biotech Getting Expensive on Earnings?

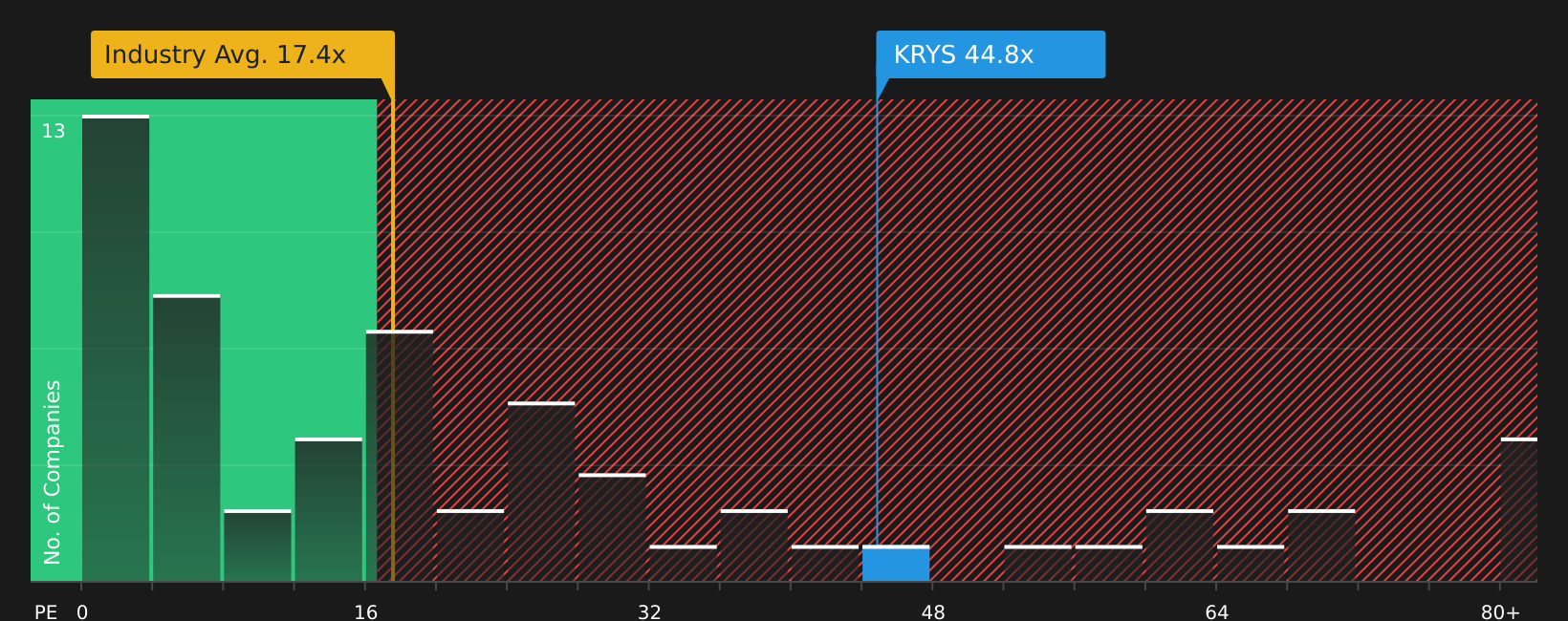

The P/E ratio is a useful way to see how much investors are paying for each dollar of Krystal Biotech’s earnings. Right now, Krystal Biotech trades on a P/E of 44.5x, compared with about 17.2x for the broader biotechs industry and 11.4x for its peer group, which points to a clear premium on this earnings measure.

The fair P/E ratio implied by the model, which blends the company’s growth profile, margins, risk and size into a tailored benchmark, is 35.8x. That is meaningfully below the current 44.5x. This suggests the stock is pricing in stronger conditions than this framework supports and leaves less cushion if expectations around Krystal Biotech’s progress or profitability shift.

On this P/E yardstick, Krystal Biotech stock currently screens as overvalued relative to both its tailored fair ratio and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Krystal Biotech Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take Krystal Biotech's valuation puzzle a step further by spelling out which assumptions about growth, margins and earnings would need to hold for the stock to be worth materially more or less than its current price. They sit on the company’s Community page. Each one turns fair value into a specific, testable view of Krystal Biotech's business so you can see how that view holds up over time.

The community is split on Krystal Biotech, with one camp seeing solid upside potential and the other arguing expectations already look stretched.

Bull case: roughly fairly valued

"The expansion of Krystal's pipeline, including imminent and near-term clinical readouts in lung disease (AATD, CF), ophthalmology, oncology (NSCLC), and aesthetics, leverages increased R&D productivity, which could drive future revenue growth and diversify earnings beyond a single product..."

Read the full Bull Case to see why Krystal Biotech could be undervalued

Bear case: 41% overvalued

"While Krystal’s HSV-1 gene therapy platform pipeline offers diversification and potential upside, heavy reliance on new clinical data readouts for multiple programs in 2025 (CF, AATD, ophthalmology, aesthetics) introduces risk, any setbacks or delays in trial outcomes could slow future adoption and revenue streams, especially given the high R&D spend and cash burn required to advance these programs..."

Read the full Bear Case to see why Krystal Biotech could be overvalued

Do you think there's more to the story for Krystal Biotech? Head over to our Community to see what others are saying!

The Bottom Line

For Krystal Biotech, the current picture points to an overvalued stock on market multiples, with the P/E sitting well above both its tailored fair ratio and sector benchmarks. That premium leaves less room for error if clinical timelines slip, regulatory outcomes disappoint or profitability trends fall short of what the price already implies. The core question from here is whether Krystal Biotech can deliver the revenue growth and cash flow scale that would keep investors comfortable paying such a rich multiple, or whether expectations eventually reset closer to the broader industry.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com