SiteOne Landscape Supply (SITE) Stock Looks Cheap On Cash Flow While Earnings Look Pricey

SiteOne Landscape Supply stock has fallen 38.7% over the past five years, yet the current intrinsic value estimate using a Discounted Cash Flow (DCF) approach suggests the shares may still trade below that modelled value, while the broader valuation checks paint a less generous picture.

- Over five years, SiteOne Landscape Supply has declined 38.7%, which places extra focus on whether the current price reflects the company’s longer term cash flow potential.

- Future cash generation from its distribution network and customer base can support the intrinsic value case, while any sustained pressure on margins or higher capital needs may limit how much of that value is realised for shareholders.

- SiteOne Landscape Supply scores 2 out of 6 on valuation checks, which suggests the stock does not screen as a clear bargain on the wider set of metrics.

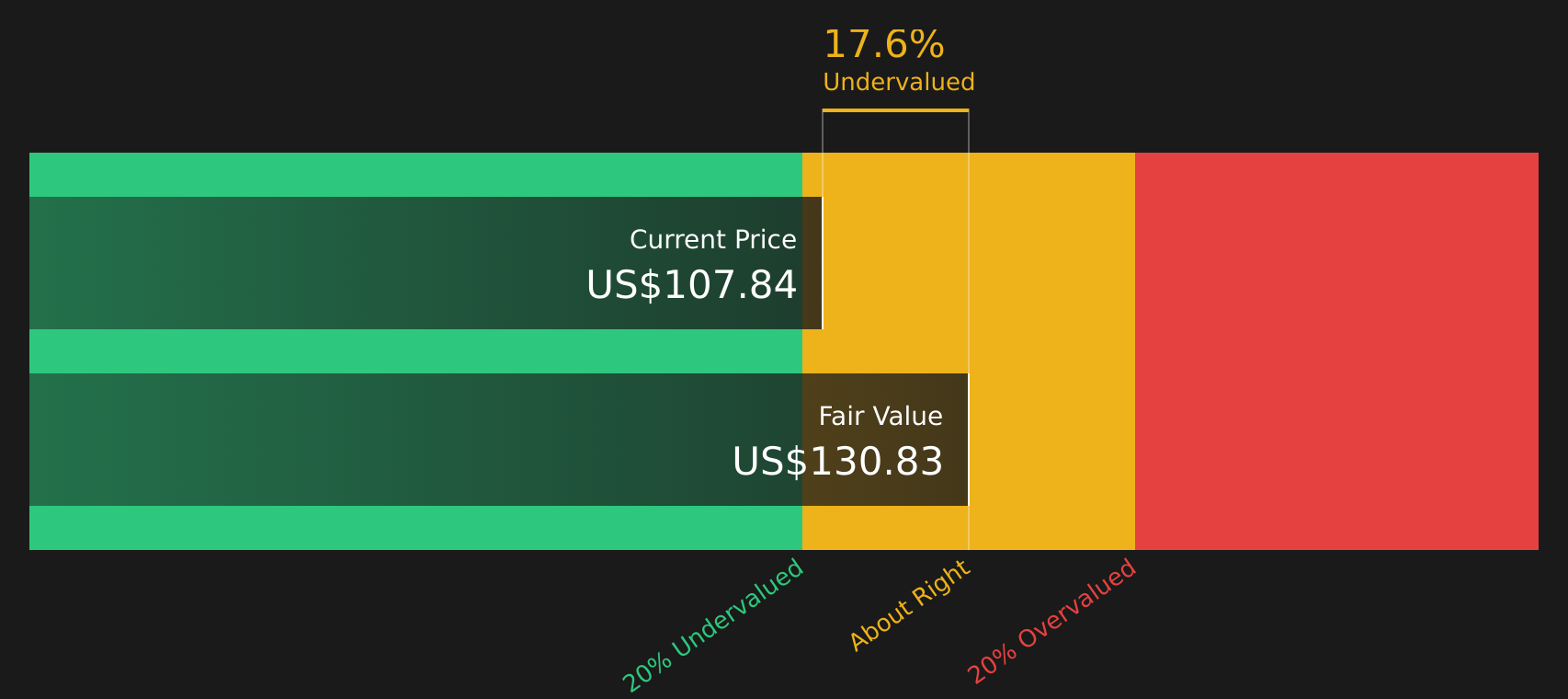

The issue now is whether the current share price of US$105.84 offers enough upside relative to the intrinsic value estimate to compensate for the risks around execution and profitability.

Is SiteOne Landscape Supply a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what SiteOne Landscape Supply could be worth today. On this basis, the company generated about $254 million of free cash flow over the latest twelve months, with the model assuming that cash flows continue to grow rather than contract over time.

Feeding those cash flows into a two stage DCF framework leads to an estimated intrinsic value of about $132 per share, compared with the current share price of $105.84. That gap implies the stock trades at roughly a 19.9% discount to this intrinsic value estimate, suggesting the market is pricing SiteOne Landscape Supply more cautiously than the cash flow model does.

Taken together, the DCF workup indicates SiteOne Landscape Supply stock currently appears undervalued on a cash flow basis according to this model.

Our Discounted Cash Flow (DCF) analysis suggests SiteOne Landscape Supply is undervalued by 19.9%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does SiteOne Landscape Supply Look Fairly Valued on Earnings?

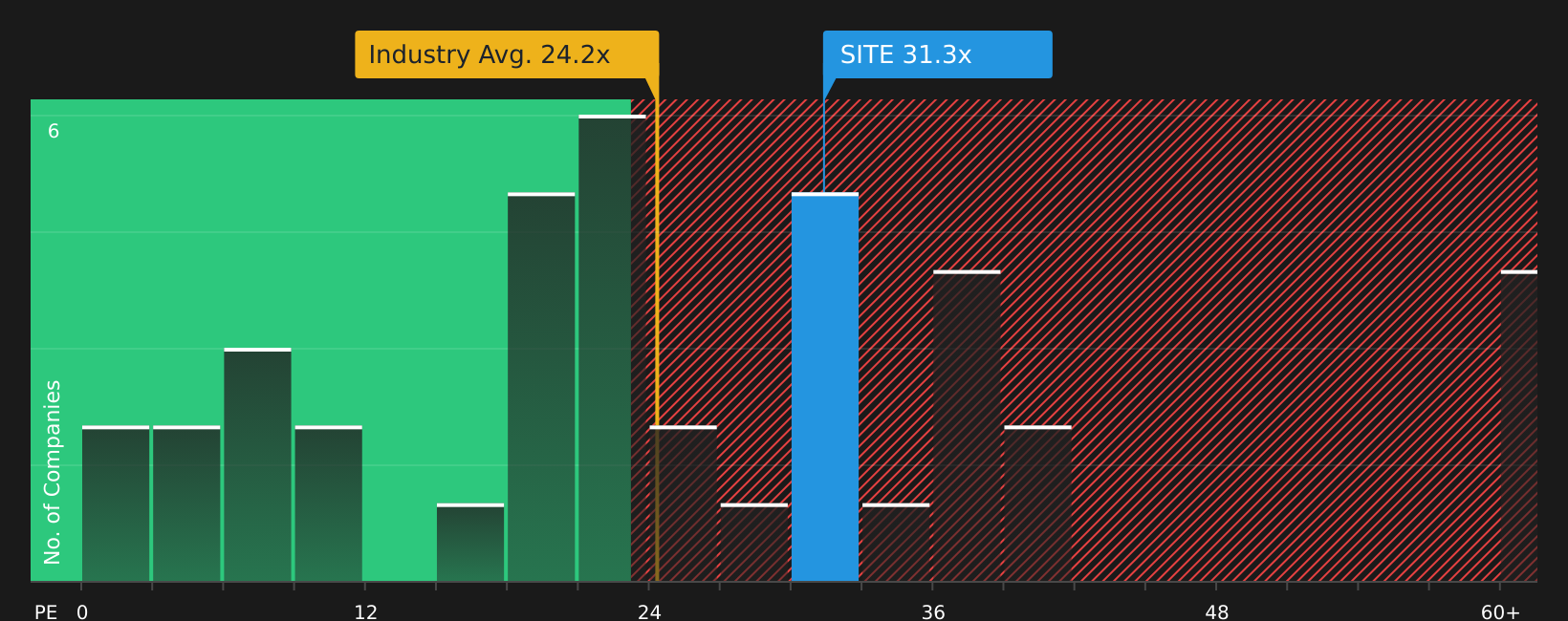

The P/E ratio is a useful cross check for SiteOne Landscape Supply because it ties the current share price directly to reported earnings. At a P/E of 30.8x, the stock trades above both the Trade Distributors industry average of 23.8x and the broader peer group average of 22.4x, so the market is already assigning a premium to its earnings.

Simply Wall St's model suggests a fair P/E of 29.7x for SiteOne Landscape Supply, which is only slightly below the current multiple. That leaves a modest premium of around 1.1x relative to the modelled fair ratio and points to a valuation that is not far from what might be expected given the company’s profile and risks.

Overall, SiteOne Landscape Supply appears to be priced at roughly a fair level on its P/E multiple, with only a small premium to the modelled fair value.

See what the numbers say about this price — find out in our valuation breakdown.

The SiteOne Landscape Supply Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for SiteOne Landscape Supply pick up where the valuation work leaves off by spelling out which future paths for SiteOne Landscape Supply's growth, margins and earnings would need to play out for the stock to be worth materially more or less than today's price on the Community page. Instead of a single ratio or model output, they describe the underlying future that figure rests on so you can watch how closely reality tracks those assumptions over time.

One of the top community narratives on SiteOne Landscape Supply: 19% undervalued

Its strength lies in serving a professional customer base with recurring needs, supported by scale, logistics, and product depth that smaller competitors struggle to match...

Read one of the top narratives on SiteOne Landscape Supply

Do you think there's more to the story for SiteOne Landscape Supply? Head over to our Community to see what others are saying!

The Bottom Line

For SiteOne Landscape Supply, the Discounted Cash Flow (DCF) work points to an intrinsic value above the current share price, while the P/E view suggests the stock is priced at about the going rate for its earnings. That split, combined with weaker scores on broader valuation checks, means the apparent discount hinges heavily on how reliably future cash flows materialise relative to capital needs and margins. The key question from here is whether SiteOne Landscape Supply can sustain the cash generation implied by the DCF without eroding profitability, or whether the current pricing already reflects those execution risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com