Is Okuma (TSE:6103) Fully Priced On Its Buyback And Recent Rally?

Okuma (TSE:6103) has completed a share buyback program, repurchasing 1,801,300 shares, or 3% of its equity, for ¥7,358.43 million. This total includes 559,900 shares acquired in the latest quarter.

See our latest analysis for Okuma.

Okuma’s recent buyback comes alongside strong share price momentum, with a 30 day share price return of 19.09% and a year to date share price return of 36.26%. In addition, the 5 year total shareholder return of 118.81% points to solid long term value creation.

If this buyback has you looking beyond Okuma, it could be a good moment to scan the market for other robotics and automation opportunities using the 33 robotics and automation stocks

Okuma has been rewarding shareholders and the share price has moved sharply higher, but a strong business is not automatically a good deal at any price. So how does the current valuation stack up after this buyback?

Price-to-Earnings of 23.3x: Is it justified?

At a last close of ¥4,960, Okuma is trading on a P/E of 23.3x, which is high compared to both its peers and the broader JP Machinery industry.

The P/E multiple compares the current share price with earnings per share, so a higher P/E usually reflects stronger profit expectations or a willingness to pay more for each unit of earnings. For Okuma, solid recent earnings growth of 30.9% over the past year and 7.2% per year over five years helps explain why the market may be comfortable with a richer earnings multiple.

However, that 23.3x P/E is well above the peer average of 15.9x and the JP Machinery industry average of 14.9x, and it also exceeds the estimated fair P/E of 18.8x. The current valuation implies investors are paying a premium that is higher than both sector norms and the level that the SWS fair ratio suggests the market could move toward if sentiment or expectations cool.

Explore the SWS fair ratio for Okuma

Result: Preferred multiple of 23.3x price-to-earnings (OVERVALUED)

However, investors in Okuma still face the risk that current profit growth or demand from key sectors like automotive and semiconductors could cool and put pressure on this premium valuation.

Find out about the key risks to this Okuma narrative.

Another view on Okuma’s value

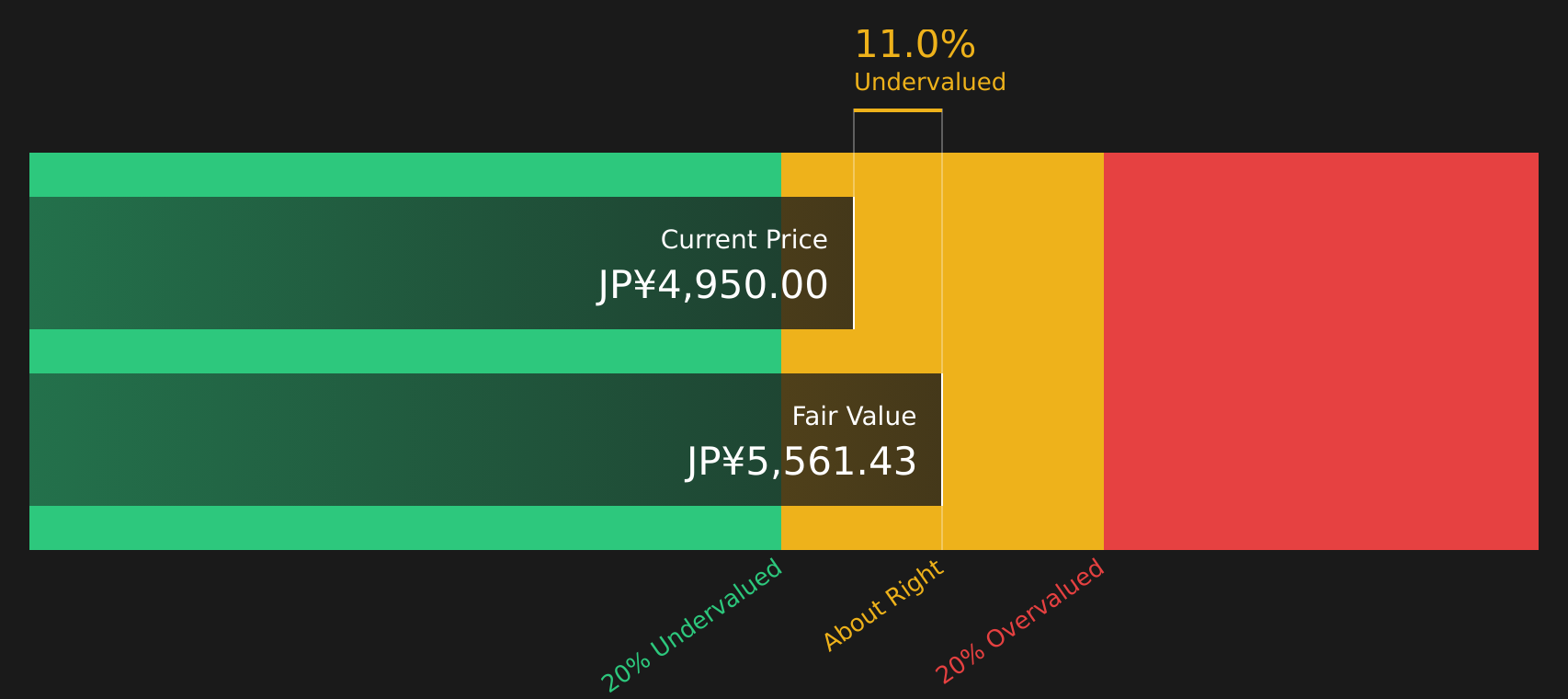

While Okuma looks expensive on a 23.3x P/E against peers, the SWS DCF model provides a different perspective. On that basis, the stock at ¥4,960 sits about 10.7% below an estimated fair value of ¥5,556.51, which indicates a potential valuation cushion rather than a premium.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Okuma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 19 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Curious whether the mixed signals around Okuma add up to a compelling case or a reason to be cautious? Move quickly to review the latest data, weigh both the concerns and the bright spots, and judge the balance of 3 key rewards and 2 important warning signs

Looking for more ideas beyond Okuma?

If Okuma has sharpened your focus, do not stop there. Use high quality screeners to spot other stocks that could fit your portfolio before the crowd catches on.

- Target value potential by checking companies that screen as quality yet priced for caution using the 19 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that currently show up as reliable payers via the 44 dividend fortresses.

- Protect your downside by scanning for companies that currently rank well on resilience using the 54 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com