Wallenstam (OM:WALL B) Returns To Profit On Q2 Earnings As Fair Value Doubts Linger

Why Wallenstam’s latest earnings matter for shareholders

Wallenstam (OM:WALL B) has moved back into profit in the second quarter of 2026, reporting net income of SEK 210 million after a net loss in the same period a year earlier.

The company’s updated figures, together with its pre recorded H1 2026 earnings call, provide fresh information on how its property portfolio and rental operations are feeding through to the bottom line this year.

See our latest analysis for Wallenstam.

The latest move back into profit appears to have given Wallenstam’s share price some support, with a 1-month share price return of 5.57% and a year-to-date share price return of 2.06%, even though the 1-year total shareholder return is down 6.34%.

If Wallenstam’s rebound has you reassessing real asset exposure, it could be a good moment to broaden your search with our 34 power grid technology and infrastructure stocks

For Wallenstam, the share price uptick has arrived just as earnings move back into the black. The key question is how much of this shift reflects the underlying rental and property business rather than a swing in sentiment alone.

Most Popular Narrative: 19.1% Overvalued

The most followed valuation view on Wallenstam puts fair value at SEK35 per share, which sits below the latest close at SEK41.70 and points to a higher required return for owning the stock at current levels.

Persistently higher interest rates and tighter monetary policy are likely to significantly increase Wallenstam's financing costs over time, especially as less of the loan book is currently interest rate hedged and more new loans are being issued at variable rates. This is expected to reduce net profit and constrain future earnings growth.

This narrative leans on modest revenue growth, thinner profit margins and a richer future earnings multiple that together have to justify a lower fair value than today.

Result: Fair Value of SEK35 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if Wallenstam maintains high occupancy and continues to expand its residential pipeline, resilient rental income could challenge the more pessimistic earnings and valuation assumptions.

Find out about the key risks to this Wallenstam narrative.

Another view on Wallenstam’s valuation

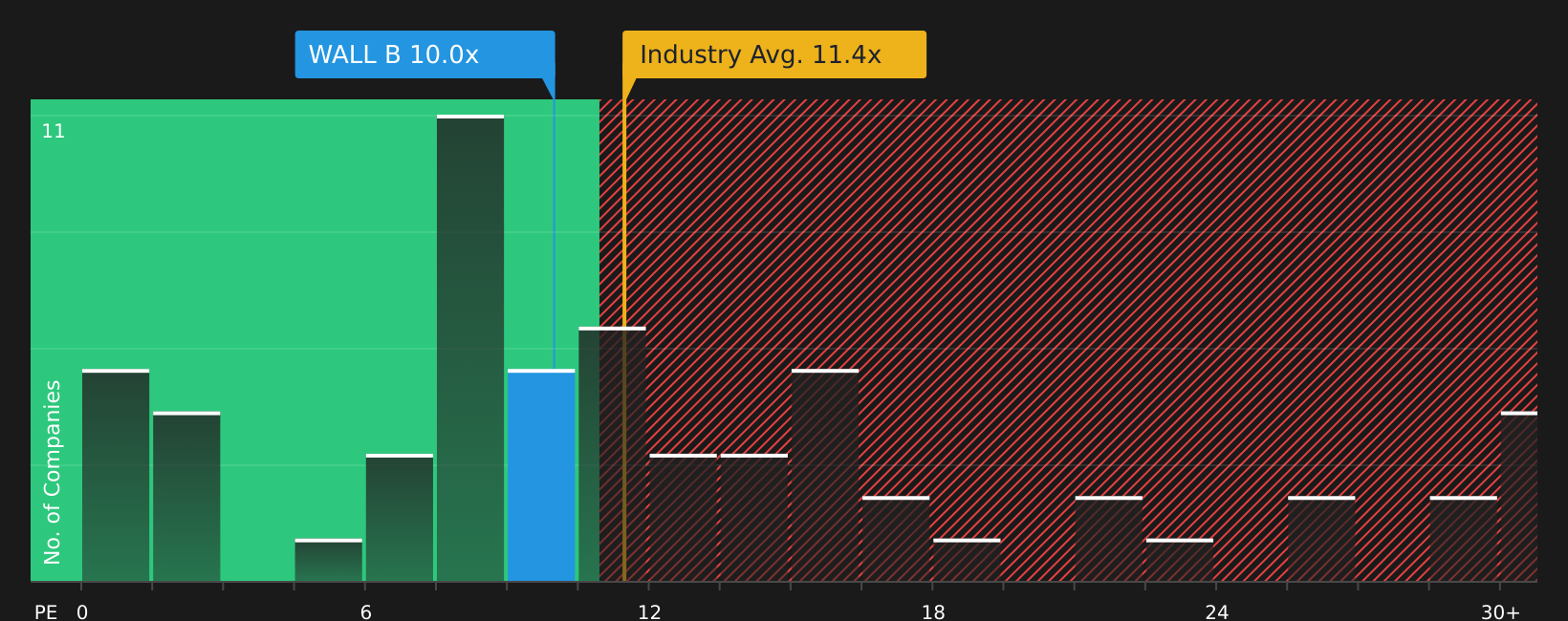

While the bearish fair value of SEK35 suggests Wallenstam is 19.1% overvalued, the current P/E of 10x looks very different. It sits well below peers at 24.4x and only slightly above a fair ratio of 9.3x. This keeps valuation risk more finely balanced than the narrative alone implies.

For investors weighing which signal to rely on, the key question is whether earnings quality and future profit trends support that small gap to the fair ratio or call for a wider discount.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Uncertain whether Wallenstam’s mixed signals lean more toward risk or reward? Act quickly, assess the full risk reward balance, and shape your own view with 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Wallenstam?

If Wallenstam has sharpened your focus on where capital works hardest, do not stop here. Broaden your watchlist now to avoid missing other compelling setups.

- Target potential mispricings by scanning for companies that look attractively valued on both quality and price using the 213 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies with higher yields that still aim for resilience through the 474 dividend fortresses.

- Prioritise resilience by zeroing in on companies with robust financial footing using the solid balance sheet and fundamentals stocks screener (420 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com