Discovering Asia's Hidden Stock Gems In July 2026

As geopolitical tensions and fluctuating energy prices impact global markets, Asia's small-cap stocks present intriguing opportunities amid broader market volatility. Identifying promising stocks in this dynamic environment requires a keen understanding of sectors poised for growth, resilience to external shocks, and alignment with emerging economic trends.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Hyundai Home Shopping Network | 6.43% | 16.06% | -2.84% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Shengda ResourcesLtd (SZSE:000603)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Shengda Resources Co., Ltd., with a market cap of CN¥14.88 billion, operates in China through its subsidiaries focusing on the mining, beneficiation, and sale of precious and non-ferrous metal ores.

Operations: Shengda Resources Co., Ltd. generates revenue primarily from the mining, beneficiation, and sale of precious and non-ferrous metal ores in China. The company has a market cap of CN¥14.88 billion.

Shengda Resources, a nimble player in the Asian market, has been making waves with its impressive financial performance. Over the past year, earnings soared by 48.3%, outpacing the industry average of 21.7%. The company's net debt to equity ratio stands at a satisfactory 33.3%, indicating prudent financial management. Shengda trades at an attractive value, estimated to be 77.6% below its fair value, offering potential upside for investors seeking opportunities in metals and mining. Recent results highlight strong growth; Q1 revenue jumped to CNY 384 million from CNY 353 million last year and net income surged to CNY 79 million from CNY 8 million previously.

- Click here and access our complete health analysis report to understand the dynamics of Shengda ResourcesLtd.

Gain insights into Shengda ResourcesLtd's past trends and performance with our Past report.

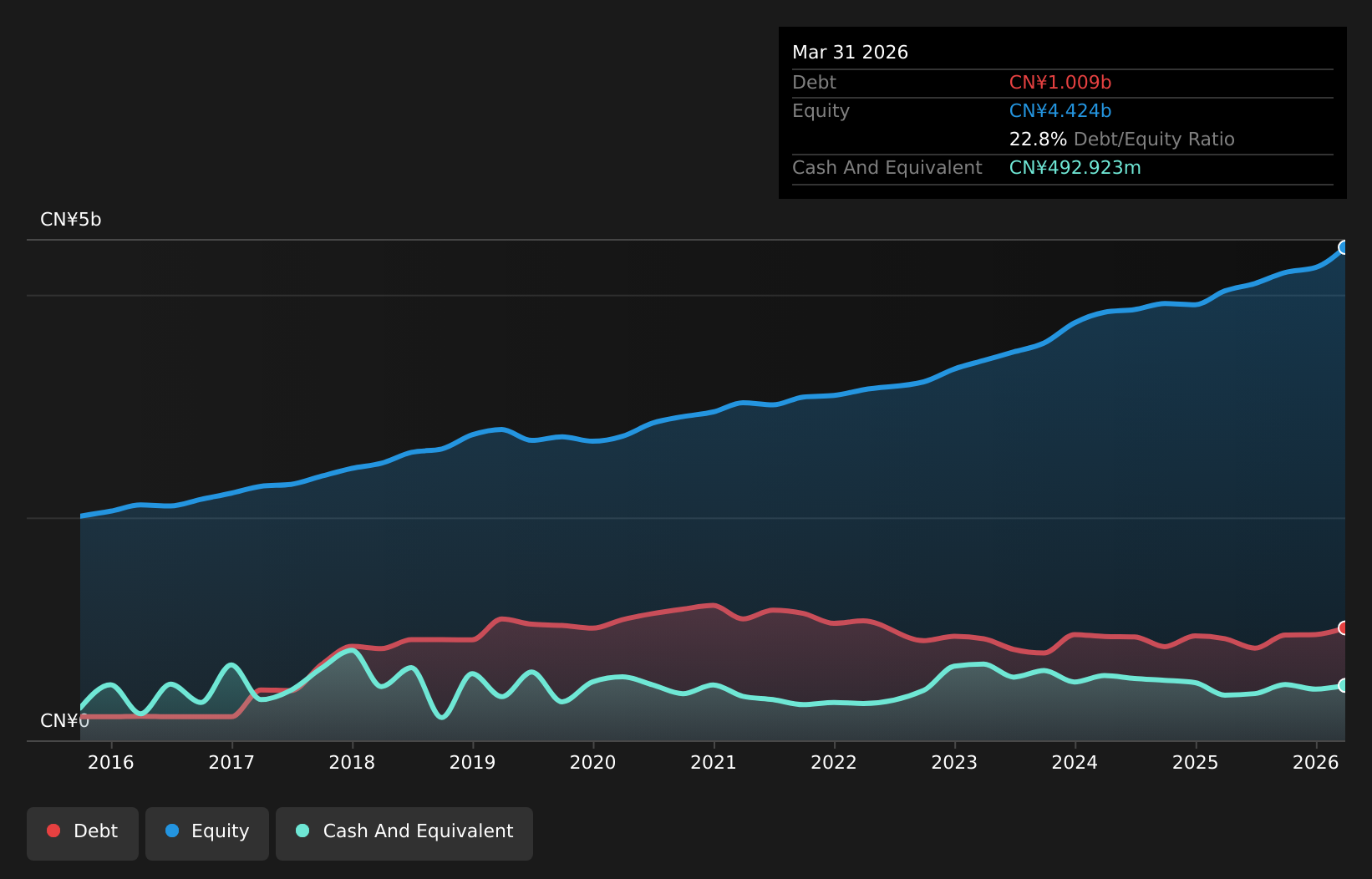

ZYNP (SZSE:002448)

Simply Wall St Value Rating: ★★★★★★

Overview: ZYNP Corporation focuses on the research, development, manufacture, and sales of automotive components both in China and internationally, with a market cap of CN¥6.62 billion.

Operations: ZYNP Corporation generates revenue primarily from the sales of automotive components. The company's net profit margin has shown variability, reflecting changes in cost structures and market conditions.

With a notable earnings growth of 119.8% over the past year, ZYNP has shown impressive performance, outpacing the Auto Components industry average of 5.4%. The company's debt to equity ratio has improved from 36% to 22.8% over five years, reflecting prudent financial management. Trading at a value significantly below its estimated fair price by 36.5%, it presents an attractive opportunity for investors seeking undervalued stocks in Asia's dynamic markets. Recent quarterly results highlight robust sales growth from CNY 950 million to CNY 1,191 million and net income increasing from CNY 111 million to CNY 198 million compared to last year.

- Unlock comprehensive insights into our analysis of ZYNP stock in this health report.

Gain insights into ZYNP's historical performance by reviewing our past performance report.

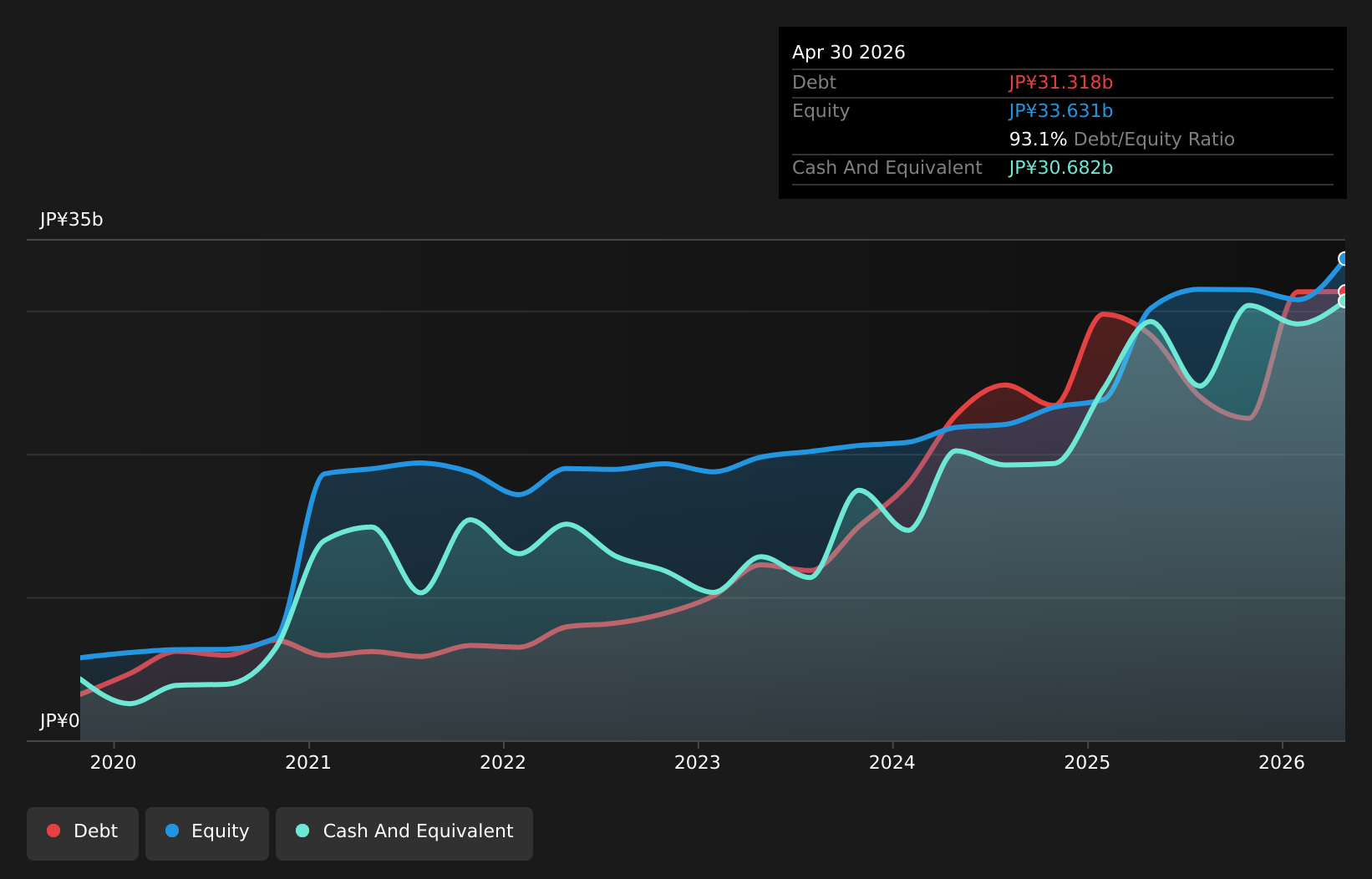

GA technologies (TSE:3491)

Simply Wall St Value Rating: ★★★★☆☆

Overview: GA technologies Co., Ltd. operates a real estate brokerage platform and has a market capitalization of approximately ¥56.94 billion.

Operations: The company generates revenue primarily through its RENOSY Marketplace, contributing ¥272.94 billion, and ITANDI segment, adding ¥6.89 billion.

GA Technologies, a promising player in Asia's tech scene, has shown impressive growth with earnings up 21.5% over the past year, outpacing the industry average of 18.2%. Despite its small size, it trades at a remarkable 70.7% below its estimated fair value and maintains satisfactory debt levels with a net debt to equity ratio of just 1.9%. However, recent volatility in share price and earnings slightly dipping from JPY 2,143 million to JPY 1,997 million highlight some challenges. Looking ahead, forecasts suggest robust annual earnings growth of about 39%, pointing to potential future gains for investors.

- Click here to discover the nuances of GA technologies with our detailed analytical health report.

Understand GA technologies' track record by examining our Past report.

Turning Ideas Into Actions

- Unlock more gems! Our Asian Undiscovered Gems With Strong Fundamentals screener has unearthed 105 more companies for you to explore.Click here to unveil our expertly curated list of 108 Asian Undiscovered Gems With Strong Fundamentals.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com