3 Asian Growth Companies With Insider Ownership Up To 36%

As geopolitical tensions in the Middle East and fluctuating energy prices capture global attention, Asian markets are navigating these challenges with a focus on growth sectors such as technology and consumer goods. In this environment, companies demonstrating robust insider ownership can be particularly appealing to investors, as it often signals confidence from those closest to the company's operations and prospects.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Underneath we present a selection of stocks filtered out by our screen.

Farsoon Technologies (SHSE:688433)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Farsoon Technologies Co., Ltd. manufactures and supplies industrial polymer and metal laser powder bed fusion systems across various regions including China, North America, the Asia Pacific, Europe, the Middle East, and Africa; it has a market cap of CN¥34.93 billion.

Operations: The company's revenue segment is primarily derived from its Machinery & Industrial Equipment division, which generated CN¥719.05 million.

Insider Ownership: 11.5%

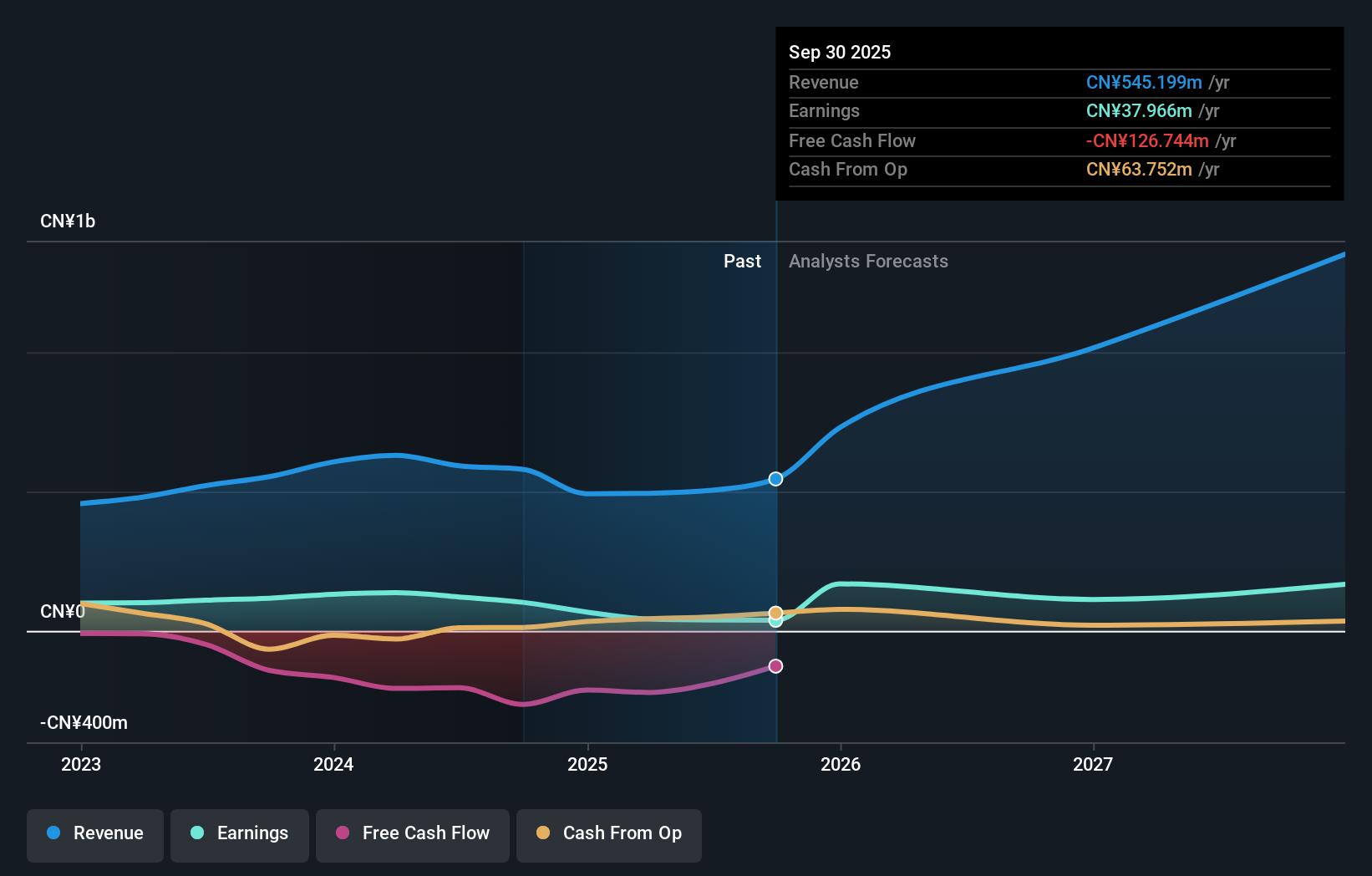

Farsoon Technologies demonstrates potential as a growth company with high insider ownership, despite recent challenges. The company's revenue is forecast to grow at 29.1% annually, outpacing the Chinese market average of 16.7%. However, it reported a net loss of CNY 3.64 million in Q1 2026 compared to a profit previously, indicating volatility. A significant private placement aims to raise up to CNY 3.91 billion for expansion and strategic initiatives, reflecting confidence from insiders and investors alike.

- Unlock comprehensive insights into our analysis of Farsoon Technologies stock in this growth report.

- Our expertly prepared valuation report Farsoon Technologies implies its share price may be too high.

Capitalonline Data Service (SZSE:300846)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Capitalonline Data Service Co., Ltd. offers cloud hosts and bare metal products across China, the Americas, Europe, and the Asia Pacific with a market cap of CN¥10.04 billion.

Operations: Capitalonline Data Service Co., Ltd. generates its revenue through the provision of cloud hosts and bare metal products across various regions including China, the Americas, Europe, and the Asia Pacific.

Insider Ownership: 23.5%

Capitalonline Data Service is poised for significant growth, with revenue projected to increase by 26.9% annually, surpassing the Chinese market average. Despite a net loss of CNY 21.52 million in Q1 2026, this marks an improvement from the previous year's loss of CNY 39.74 million, indicating progress toward profitability within three years. The absence of recent insider trading activity suggests stability in ownership structure as the company navigates its path to profitability and expansion.

- Click here and access our complete growth analysis report to understand the dynamics of Capitalonline Data Service.

- Upon reviewing our latest valuation report, Capitalonline Data Service's share price might be too optimistic.

Round One (TSE:4680)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Round One Corporation operates indoor leisure complex facilities and has a market cap of ¥346.99 billion.

Operations: Revenue segments for the company include amusement facilities generating ¥102,000 million, bowling contributing ¥52,000 million, karaoke at ¥25,000 million and sports entertainment bringing in ¥15,000 million.

Insider Ownership: 36.1%

Round One Corporation demonstrates potential for growth with forecasted earnings increasing by 13.6% annually, outpacing the Japanese market's average. Recent sales data shows a year-on-year increase of approximately 17% as of June 2026, highlighting strong revenue momentum. Trading at a discount to its estimated fair value, the company benefits from high insider ownership, which can align management interests with shareholders. Despite slower revenue growth projections compared to some peers, its return on equity is expected to remain robust.

- Delve into the full analysis future growth report here for a deeper understanding of Round One.

- Our valuation report here indicates Round One may be undervalued.

Make It Happen

- Take a closer look at our Fast Growing Asian Companies With High Insider Ownership list of 480 companies by clicking here.

- Ready To Venture Into Other Investment Styles? These 26 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com