3 Australian Mining Stocks With Strong Earnings Growth and Healthy Balance Sheets

With inflation paths, energy prices and bond yields all pulling at markets, investors are searching for companies that still offer solid growth potential without excessive balance sheet stress. The Healthy high growth potential screener focuses on stocks where analysts expect strong earnings growth over the next 3 years, while the companies also meet defined financial health criteria. That combination can help you concentrate on opportunities that balance growth with resilience. In this article, you will see 3 stocks from this screener, along with a clear breakdown of what stands out for each one and what to watch next.

Paladin Energy (ASX:PDN)

Overview: Paladin Energy is an Australia based uranium company that develops and explores uranium deposits across Australia, Canada and Namibia, with its flagship Langer Heinrich mine in Namibia being a key producing asset. The company focuses on supplying uranium to global utilities that rely on nuclear power for baseload electricity.

Operations: Paladin Energy currently generates all reported revenue of about US$248.5 million from its Namibian operations.

Market Cap: A$4.09b

Paladin Energy provides direct exposure to a producing uranium miner at a time when nuclear power is attracting renewed interest. It is backed by a long life mine at Langer Heinrich and a high grade growth option at Patterson Lake South. Reported revenue of US$209.05 million over the first nine months of 2026 and a move from a US$30.07 million loss to a small profit indicate a business that is edging toward sustained profitability. The stock currently appears expensive on simple valuation metrics and remains reliant on a successful production ramp up. Long term contracts, index inclusion and fresh exploration results at the Atlas zone are additional factors investors may wish to examine in more detail.

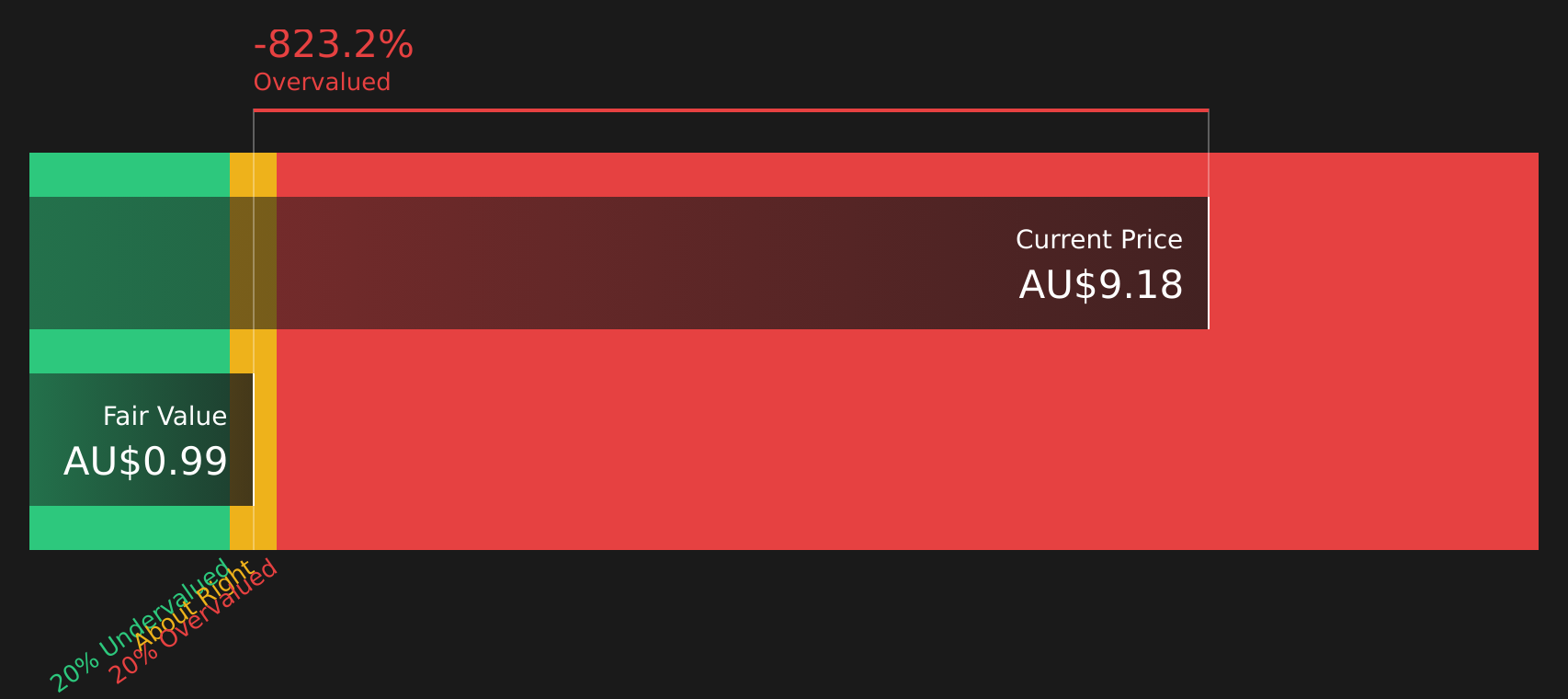

Paladin Energy’s shift from loss to profit and its uranium exposure are drawing attention, but the main focus may be on how the current price compares with its future cash flows in the DCF valuation analysis for Paladin Energy

Westgold Resources (ASX:WGX)

Overview: Westgold Resources is a Perth based gold producer that explores, develops, and operates gold mines across its Murchison and Southern Goldfields hubs in Western Australia, supplying refined gold to the global market.

Operations: Westgold Resources generates all its reported A$2.0b in revenue from Australia, with about A$1.3b from Murchison and A$690.8m from Southern Goldfields.

Market Cap: A$4.46b

Westgold Resources may appeal to investors who want exposure to gold with scale, improving profitability and a clearer asset base. Earnings growth has been very strong, margins have improved from 2.4% to 12.8%, and analysts expect both revenue and earnings to grow faster than the broader Australian market. At the same time, the company is integrating the Karora acquisition, upgrading processing hubs and divesting non core projects like Chalice and Peak Hill, while relying heavily on external borrowing and facing ore grade and cost pressures. How those moving parts interact with a stock that some analysts see trading well below estimated fair value is central to the current Westgold Resources investment story.

Westgold Resources’ earnings and margins are moving, but the real story may be how the current share price stacks up against analyst expectations in the analyst forecasts for Westgold Resources, including one factor that could flip the script.

Lynas Rare Earths (ASX:LYC)

Overview: Lynas Rare Earths mines and processes rare earth minerals from its Mt Weld operation in Western Australia and refines them into specialised materials at plants in Kalgoorlie and Malaysia, supplying essential inputs for electric vehicles, wind turbines and advanced electronics. The company focuses on both light and heavy rare earths, from lanthanum and cerium through to neodymium, dysprosium and other magnet materials.

Operations: Lynas Rare Earths generates about A$715.9 million in revenue from its Rare Earth Operations segment.

Market Cap: A$16.35b

Lynas Rare Earths is attracting interest because it sits at the centre of rare earth supply outside China, with earnings that have rebounded 62% over the past year, revenue growth forecast above 20% a year and a new long term magnet partnership with JS Link running through 2038. At the same time, the stock trades below some fair value estimates and analyst targets, even as the company leans heavily on external borrowing and faces regulatory and execution risk around its Malaysian expansion and downstream move into magnets. For investors who want exposure to electrification materials but are weighing rich valuation multiples against growth, funding risk and policy uncertainty, the key consideration is how these pieces fit together for Lynas over the next few years.

Lynas Rare Earths sits at the crossroads of growth, funding risk and policy pressure, and the missing piece is how analysts see that playing out in the analyst forecasts for Lynas Rare Earths

The three stocks here are just the starting point. The full Healthy high growth potential screen surfaces 95 more companies that pair strong forecast earnings growth with financial profiles that can support it in different ways through the Healthy high growth potential screener. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you, so you can focus on the highest conviction ideas within that broader list.

Take Control of Your Investment Journey

If Lynas Rare Earths or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the sharpest breakouts start quietly, while momentum builds under the radar for now. Before the crowd catches on and prices start flying, scan these fresh ideas and consider whether they fit your approach.

- Spot companies quietly building strength with the list of solid balance sheet and fundamentals (20 results) and focus on businesses that pair staying power with room for renewed momentum.

- Review the 33 elite gold producer stocks curated for producers that may be positioned to respond if sentiment shifts toward hard assets.

- Explore the 52 AI infrastructure stocks to narrow in on companies supporting the underlying infrastructure of the AI trend while it is still developing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com