Is Celsius Holdings (CELH) Below Fair Value As Revenue Growth And Rockstar Marketing Expand?

Recent updates around Celsius Holdings (CELH) are drawing attention as the company pairs ongoing revenue growth and market expansion with a refreshed marketing push for Rockstar Energy, including a return to NASCAR and focused sports and music branding.

See our latest analysis for Celsius Holdings.

At a share price of US$30.14, Celsius Holdings has seen mixed momentum, with the 1-month share price return up 3.29% but the year-to-date share price return down 36.88%. The 5-year total shareholder return of 37.86% contrasts with weaker 1-year and 3-year total shareholder returns, suggesting earlier gains have cooled even as new branding efforts for Rockstar Energy and ongoing expansion keep the story in focus.

If Celsius has you thinking about where growth stories could emerge next, it may be worth scanning 18 top founder-led companies as a way to surface other interesting possibilities.

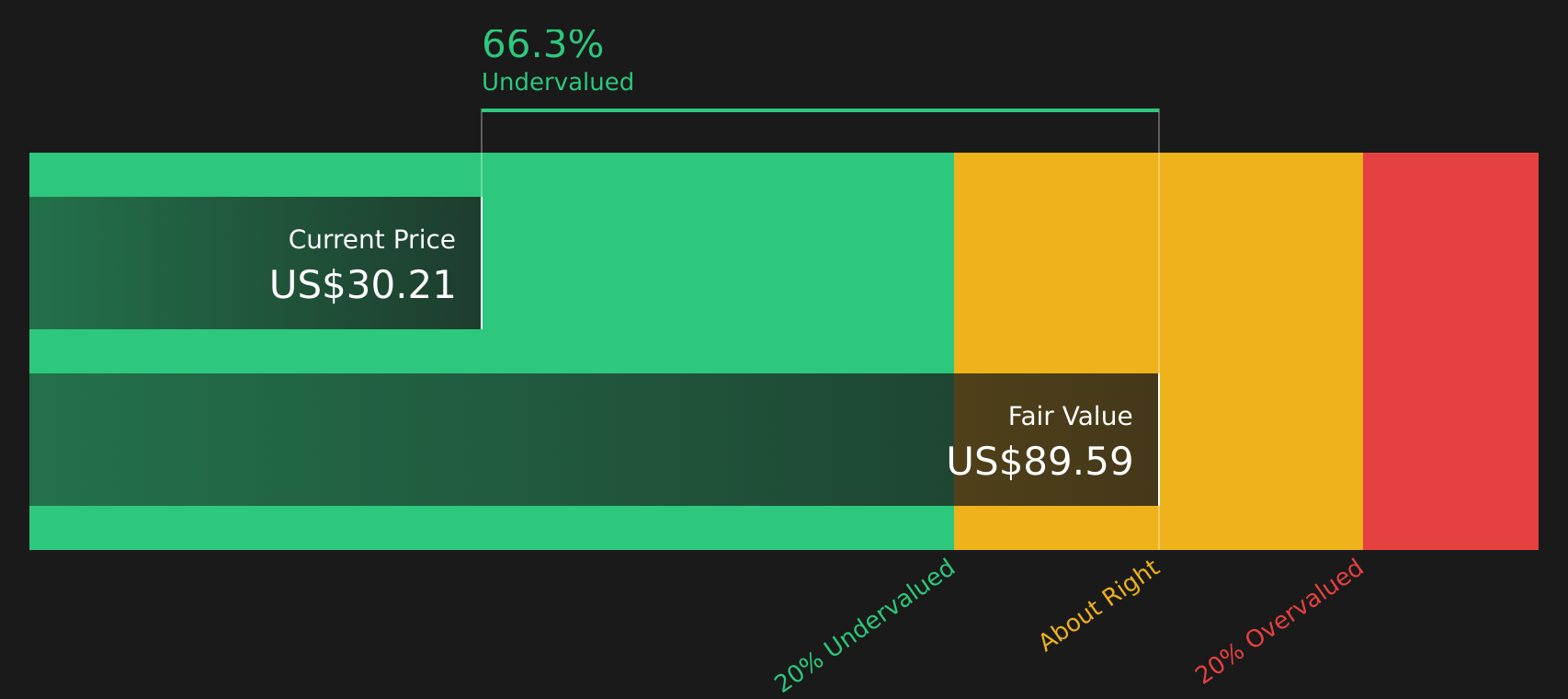

Celsius Holdings now trades at US$30.14 while analyst targets and intrinsic value estimates sit much higher. How wide is that gap in practical terms, and what does the valuation range really suggest?

Most Popular Narrative: 45.6% Undervalued

At $30.14, Celsius Holdings is priced well below the narrative fair value of $55.43, which frames the current pullback as part of a much longer story.

A 17-Year Story That Most Investors Only Discovered in the Last Three. In 2010, Celsius Holdings (CELH) was generating roughly US$5 million in annual revenue, a forgotten energy drink with niche distribution in Scandinavian gyms and a handful of US health food stores. By the end of 2025, the company had crossed US$2 billion in trailing twelve-month revenue and acquired two major energy drink brands. It secured PepsiCo as both its primary distributor and an 11% equity holder. Most retail investors only discovered this stock near the peak in 2023. The ones who understood what actually happened in 2024 and why the crash was a channel inventory problem, not a brand problem, had the best entry point in a decade. This narrative is about understanding which of those two situations you are looking at right now, as the company enters an entirely new chapter.

Want to see what sits behind a $55.43 fair value for Celsius Holdings at a 9% discount rate? The narrative leans heavily on profitable expansion, acquired brands bedding in, and a future earnings multiple usually reserved for larger consumer leaders. Curious which revenue mix, margin path, and growth runways have to hold together to justify that view? The full storyline joins those dots in detail.

Result: Fair Value of $55.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, even a well framed Celsius Holdings narrative can be upended if PepsiCo reduces support or if the Rockstar acquisition drags on margins and brand equity.

Find out about the key risks to this Celsius Holdings narrative.

Another View: Celsius Holdings Through the P/E Lens

The SWS DCF model points to Celsius Holdings trading below an estimated future cash flow value of $89.59 at a share price of $30.14. This reinforces the narrative fair value of $55.43 and frames the P/E ratio of 67.3x as a trade off between growth expectations and valuation risk. Is that a level you are comfortable with?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Given the mix of confidence and caution around Celsius Holdings, it makes sense to look at the full picture and move quickly to your own judgment. To see how the current valuation, downside risks and potential upside fit together, start with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Celsius Holdings?

If Celsius Holdings has sharpened your focus on where your capital works hardest, do not stop here. The next opportunity you miss could be the one that matters.

- Target reliable income by reviewing companies with strong yields and resilience through the 8 dividend fortresses.

- Spot potential value opportunities early by scanning the screener containing 20 high quality undiscovered gems before they gain wider attention.

- Prioritise capital preservation by filtering for resilience using the 79 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com