Antec: Polysilicon prices are weakly declining, and the average price of n-type compound feed is 32,500 yuan/ton

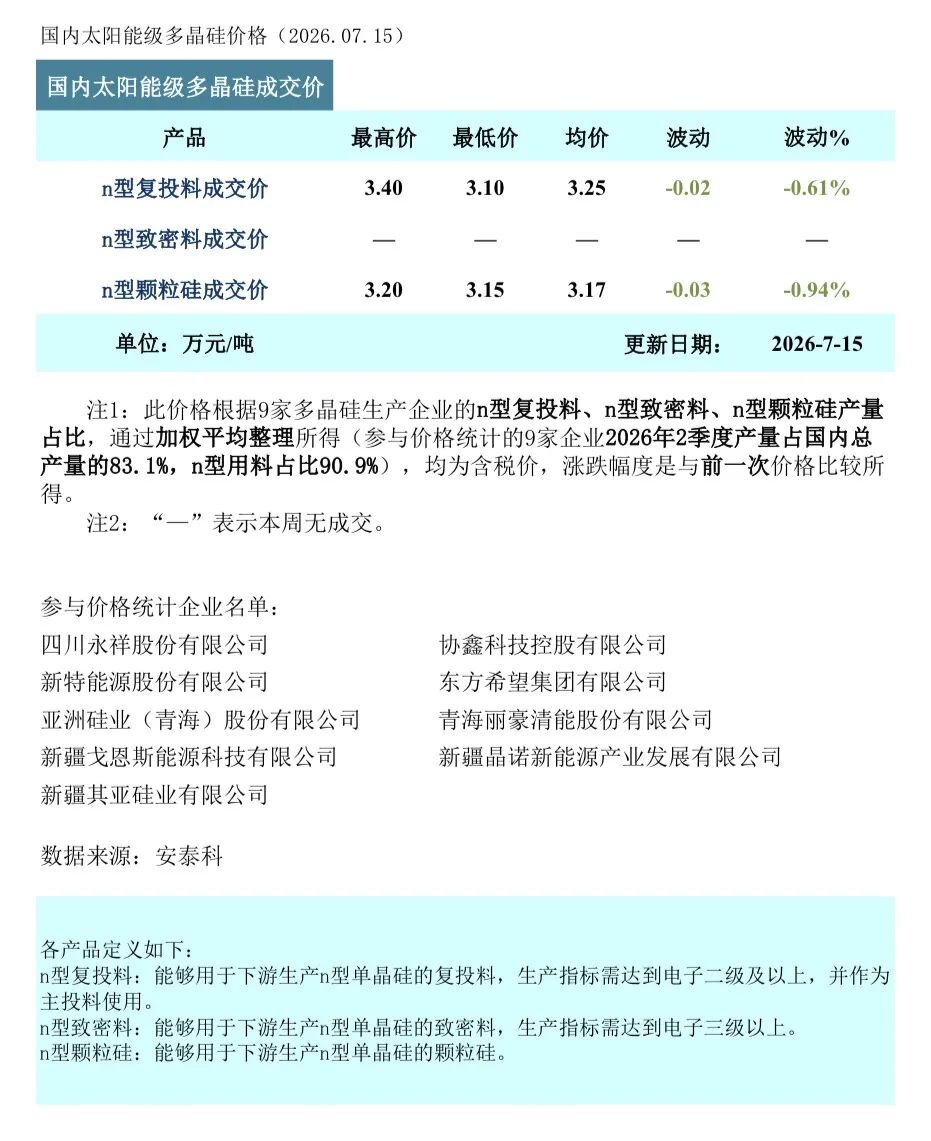

Zhitong Finance App learned that according to Antech statistics, this week's n-type compound feed (rod-shaped silicon) transaction price range was 3.10-34,000 yuan/ton, with an average transaction price of 32,500 yuan/ton, down 0.61% from month to month; the transaction price range for n-type granular silicon was 315-32,000 yuan/ton, with an average transaction price of 31,700 yuan/ton, down 0.94% from month to month.

The domestic polysilicon market continued its weak trend this week, and the focus of transactions continued to decline slightly. The overall transaction atmosphere was still light. Although the number of companies that signed new orders increased to 6, the number of orders did not improve, mostly scattered purchases. Currently, the high inventory pressure in the industry continues to fluctuate, and there has been no substantial reversal of the situation where demand for terminal installations is weak. Downstream silicon wafer companies have always been cautious in their procurement mentality, adhere to the rhythm of replenishing stocks as needed, and are less willing to take the initiative to prepare goods.

The supply side showed a fragmentation trend this week. Although production was steadily climbing due to the resumption of production by leading companies, it was hedged by additional individual companies' full-line maintenance, and the overall increase was limited. According to the comprehensive production schedule, polysilicon production will continue to grow in July, and the pattern of loose supply remains unchanged. The demand side continues to be weak. Affected by terminal transmission, the operating rate of silicon wafers is low, the willingness to purchase silicon materials is insufficient, the conflict between supply and demand in the industry still exists, and inventories continue to accumulate.

Taken together, there has been no substantial reversal of the current situation of high inventories and weak demand. The polysilicon market is still at the bottom of the supply-demand game, but there is relatively limited room for prices to continue to decline: the deep price drop has made the bottom characteristics more clear, and corporate price promotion agreements are gradually being formed; the superposition of the new energy consumption policy accelerates the clearance of backward production capacity, and policy support effects continue to be unleashed. It is expected that the market will complete structural adjustments in the midst of a bottom-up shock, and subsequent repairs can be expected.