Fonterra Co Operative Group (NZSE:FCG) Could Be 68% Undervalued As Milk Price Forecast Falls

Fonterra Co-operative Group (NZSE:FCG) cut its 2026/27 forecast Farmgate Milk Price to NZ$9.25 per kgMS after an 11% drop in Global Dairy Trade prices, signaling softer demand and potential earnings pressure.

See our latest analysis for Fonterra Co-operative Group.

At the current share price of NZ$4.23, Fonterra Co-operative Group has seen its 90 day share price return fall 13.14%, even as year to date share price return is 5.75% and the 5 year total shareholder return is 271.50%. This suggests momentum has cooled in the short term while long term holders have still experienced strong compounding.

If this shift in sentiment has you thinking about where else capital might work hard, it could be a good time to scan 33 elite gold producer stocks for other potential opportunities.

Bulls may view Fonterra Co-operative Group’s pullback and lower milk price forecast as a reset, while bears focus on softer demand and pressure on earnings. Which side does the valuation currently lean toward?

Price-to-Earnings of 9.7x: Is it justified?

On the numbers alone, Fonterra Co-operative Group looks inexpensive, with the stock at NZ$4.23 trading on a P/E of 9.7x compared with richer peers in the food sector.

The P/E ratio compares the current share price to earnings per share, so a lower number can indicate the market is placing a lower value on each dollar of profit. For a profitable business like Fonterra Co-operative Group, it is a quick way to see how investors are weighing earnings against sector alternatives.

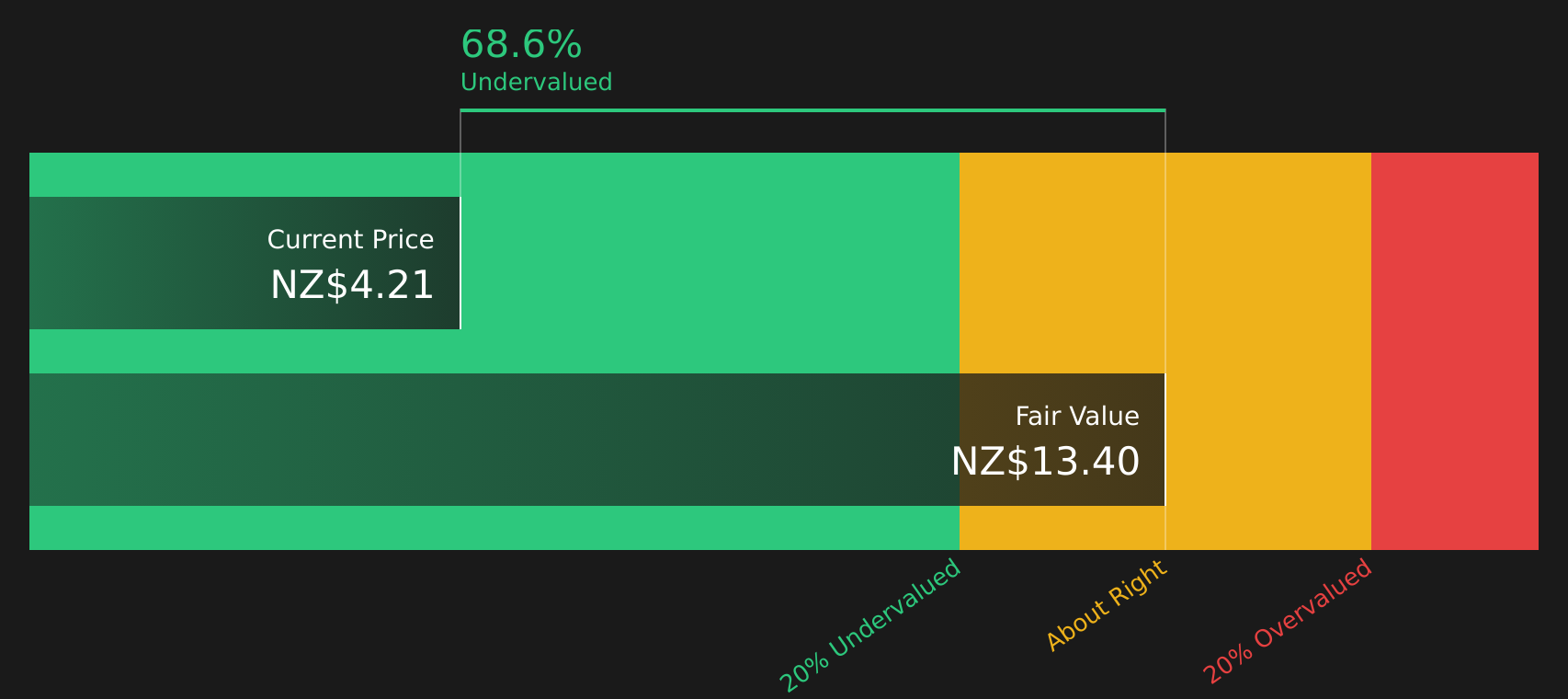

Here, the gap is clear. Fonterra Co-operative Group trades at 9.7x earnings, while the Oceanic Food industry sits at 13.6x and the broader peer group average is 17.6x, implying the stock is priced at a sizeable discount to both groups. That sits alongside the SWS DCF model, which currently suggests the shares are trading 68.4% below its estimate of future cash flow value at NZ$13.40.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 9.7x (UNDERVALUED)

However, the cut to Fonterra Co-operative Group’s milk price forecast and softer Global Dairy Trade demand could pressure future earnings and limit the speed at which sentiment stabilises.

Find out about the key risks to this Fonterra Co-operative Group narrative.

Another view on Fonterra Co-operative Group’s value

The SWS DCF model presents another perspective on Fonterra Co-operative Group, with an estimated future cash flow value of NZ$13.40 per share compared with the current NZ$4.23, indicating the stock is trading at a 68.4% discount. If that gap persists, what is the market still concerned about?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Fonterra Co-operative Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 208 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Fonterra Co-operative Group clearly split between risks and rewards, it makes sense to move quickly, review the underlying numbers, and shape your own view using our breakdown of 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Fonterra Co-operative Group?

If Fonterra Co-operative Group has sharpened your focus on valuation and risk, now is a smart moment to scan other stocks that might better fit your goals.

- Target potential bargains by reviewing companies that screen well on quality and value using the 208 high quality undervalued stocks.

- Strengthen your income stream by checking stocks highlighted as yield heavyweights via the 464 dividend fortresses.

- Prioritise resilience by focusing on companies that clear strict risk filters through the 299 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com