Is Entergy (ETR) Fairly Valued Following Its Mitsubishi Carbon Capture Alliance?

Entergy’s carbon capture alliance with Mitsubishi: what investors should watch

Entergy (ETR) is drawing fresh attention after signing a memorandum of understanding with Mitsubishi Heavy Industries Group to advance gas turbine, carbon capture and storage projects, while targeting a 50% reduction in overall costs.

See our latest analysis for Entergy.

Entergy’s recent carbon capture agreement arrives as the stock trades at $115.41, with a year to date share price return of 22.96% and a 5 year total shareholder return of 169.38%. This performance suggests momentum supported by long term income and dividends.

If this low carbon power story has your attention, it could be a good moment to scan other grid focused opportunities using our 34 power grid technology and infrastructure stocks

Entergy’s Mitsubishi partnership and the stock’s recent run invite a practical question for investors weighing carbon capture exposure now: Is today’s price already baking in the new roadmap, or does the valuation still leave room for patience?

Most Popular Narrative: 5.3% Undervalued

Entergy’s most followed narrative pegs fair value at $121.88, a touch above the last close at $115.41. This frames the Mitsubishi deal within a broader growth and earnings story.

Capital investment of $40 billion over four years (with an expanded pipeline for renewables, grid modernization, and resilience upgrades) is expected to grow the company's rate base and support above-average EPS and earnings growth for several years.

Read the complete narrative. Read the complete narrative.

Want to see what is backing that fair value gap? The narrative leans on steady double digit earnings growth, rising margins, and a future earnings multiple that assumes investors keep paying up for Entergy’s long term plan.

Result: Fair Value of $121.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Entergy story also hinges on heavy capital needs and Gulf South weather exposure, and either factor could pressure returns if financing or storm impacts surprise.

Find out about the key risks to this Entergy narrative.

Another view on Entergy’s valuation

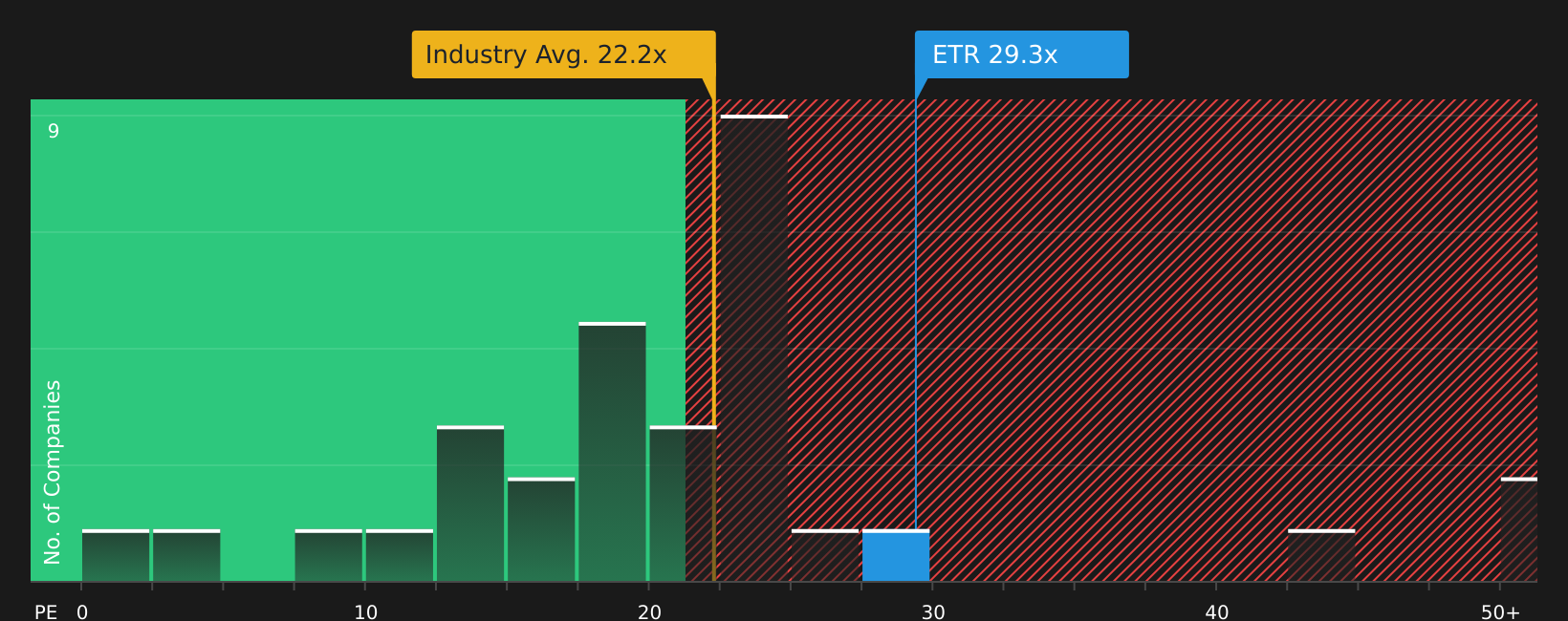

The analyst narrative tags Entergy as 5.3% undervalued at $121.88 fair value, but the current multiples tell a more demanding story. At a 29.6x P/E versus 22.4x for the US Electric Utilities industry and a 26.9x fair ratio, investors are paying a visible premium. Is that premium a narrow cushion or a hidden risk?

Our valuation work using this P/E comparison asks you to weigh how comfortable you are paying above both peers and the fair ratio for Entergy’s earnings profile, especially with earnings forecast to grow 15% a year but at a slower pace than the broader US market. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seen enough to sense both optimism and caution around Entergy? Put the headlines aside for a moment and look at the full picture of risks and rewards yourself, starting with the 2 key rewards and 2 important warning signs.

Looking for more Entergy sized investment ideas?

If Entergy has sharpened your focus, do not stop here. Broaden your watchlist now to avoid missing other strong setups hiding in plain sight.

- Target income strength by reviewing companies in the 8 dividend fortresses that may suit a portfolio built around regular cash returns.

- Hunt for value by checking the screener containing 20 high quality undiscovered gems before the rest of the market pays attention.

- Prioritise resilience by scanning stocks in the 79 resilient stocks with low risk scores that aim to keep volatility in check while you stay invested.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com