SMS (TSE:2175) Stock Looks Cheap On Cash Flow But Less Clear After An 88% Run

SMS stock has climbed strongly year to date, yet both the Discounted Cash Flow (DCF) intrinsic value estimate and the market multiples still point to the shares trading at a discount, which sits alongside a mixed overall valuation score.

- Year to date, SMS has returned 87.9%, which puts extra focus on whether the current share price fully reflects its intrinsic value.

- The valuation case can be supported if SMS continues to convert revenue into reliable cash flows. Any setback in cash generation or higher capital needs may weaken the argument that the stock is pricing in enough caution.

- SMS screens as undervalued on both intrinsic value and multiples, but with a mixed set of checks, scoring 3 out of 6 on overall valuation. This suggests neither a straightforward bargain nor a clear overpricing.

The stock's next move may depend on whether SMS's recent gains have already captured most of the upside implied by its current intrinsic value estimate.

Does SMS Look Undervalued on Cash Flow?

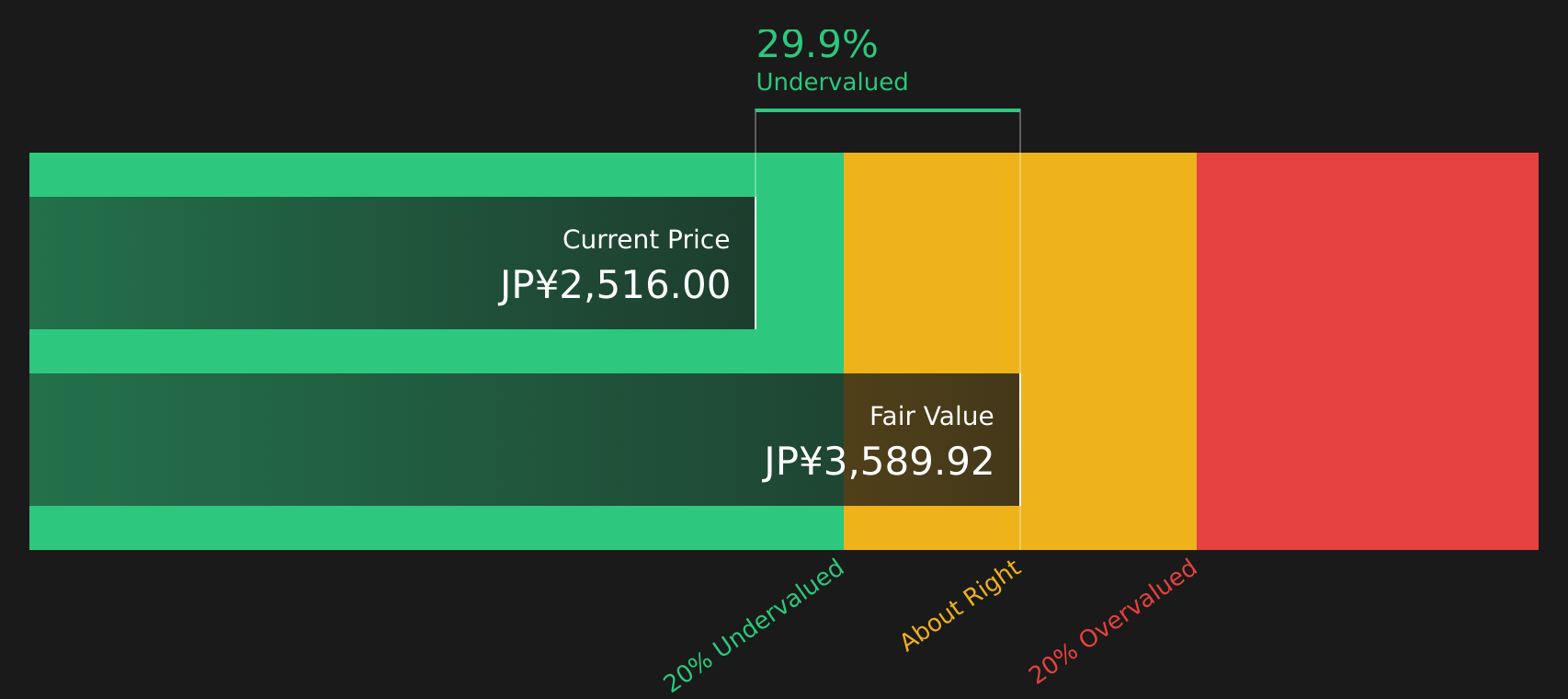

The Discounted Cash Flow (DCF) approach estimates what SMS is worth today based on the cash it is expected to generate in the future. For SMS, the model uses latest twelve month free cash flow of about ¥4.6b and assumes that cash generation continues to grow over time rather than contract.

Using these inputs, the DCF model arrives at an estimated intrinsic value of around ¥3,589 per share. Compared with the current share price, this implies SMS appears about 29.3% undervalued. In other words, the market price sits below the level that the projected cash flows would justify if they are delivered.

Under the current Discounted Cash Flow assumptions, SMS stock appears undervalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests SMS is undervalued by 29.3%. Track this in your watchlist or portfolio, or discover 16 more high quality undervalued stocks.

Does SMS Look Undervalued on Sales?

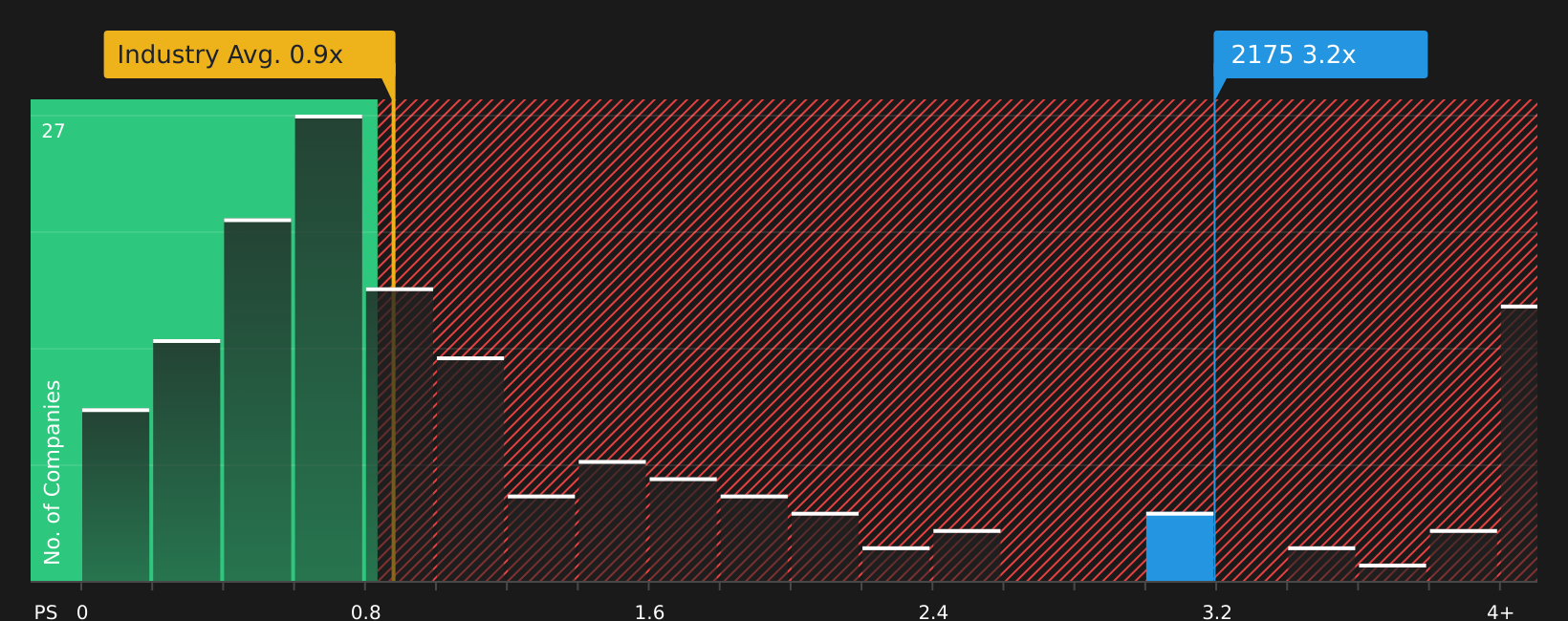

The P/S ratio is a useful cross check for SMS because its revenue base is more stable than its accounting earnings and book value. SMS currently trades on a P/S of about 3.2x, compared with an industry average of roughly 0.9x and a peer group average of around 2.4x, so the stock sits at a premium to both reference points.

The tailored fair P/S ratio for SMS is estimated at about 4.3x, which is higher than where the stock trades today. That gap suggests the current market price does not fully reflect the level of sales investors might expect, given the company’s size, margins and risk profile.

On the P/S multiple, SMS stock appears undervalued relative to the level the fair ratio would indicate.

See what the numbers say about this price — find out in our valuation breakdown.

The SMS Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for SMS take the valuation puzzle a step further by explaining which assumptions about SMS' future growth, margins and earnings would need to hold for the stock to be worth materially more or less than it is today, using scenarios hosted on the Community page. Each scenario links a fair value estimate to a particular set of potential catalysts and risks, so you can track over time which version of SMS' story appears closer to reality.

Share a Narrative on SMS in the Simply Wall St community to lay out your number driven case on where its growth, margins and execution go from here, and see how your thesis stacks up as new data arrives.

Do you think there's more to the story for SMS? Head over to our Community to see what others are saying!

The Bottom Line

For SMS, both the Discounted Cash Flow (DCF) intrinsic value estimate and the tailored sales multiple point to an undervalued stock, even after recent gains. The catch is that the broader set of valuation checks is mixed, so the apparent discount is not a slam dunk. The key question is whether SMS can keep turning its revenue base into consistent free cash flow without requiring significantly higher capital. That cash generation profile is likely to decide whether today’s discount proves to be an opportunity or a sign that the market is appropriately cautious.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com