How Investors May Respond To NNN REIT (NNN) Extending Its 37-Year Dividend Growth Streak

- NNN REIT, Inc.’s Board of Directors previously approved a quarterly dividend of US$0.62 per share, payable August 14, 2026, to shareholders of record on July 31, 2026, representing a 3.3% increase and marking the company’s 37th consecutive annual dividend increase.

- This streak places NNN among only three publicly traded REITs with 37 or more straight years of annual dividend raises, underscoring its long-term focus on consistent income for shareholders.

- Next, we’ll explore how NNN’s 37-year dividend growth streak interacts with its focus on necessity-based tenants to shape its investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

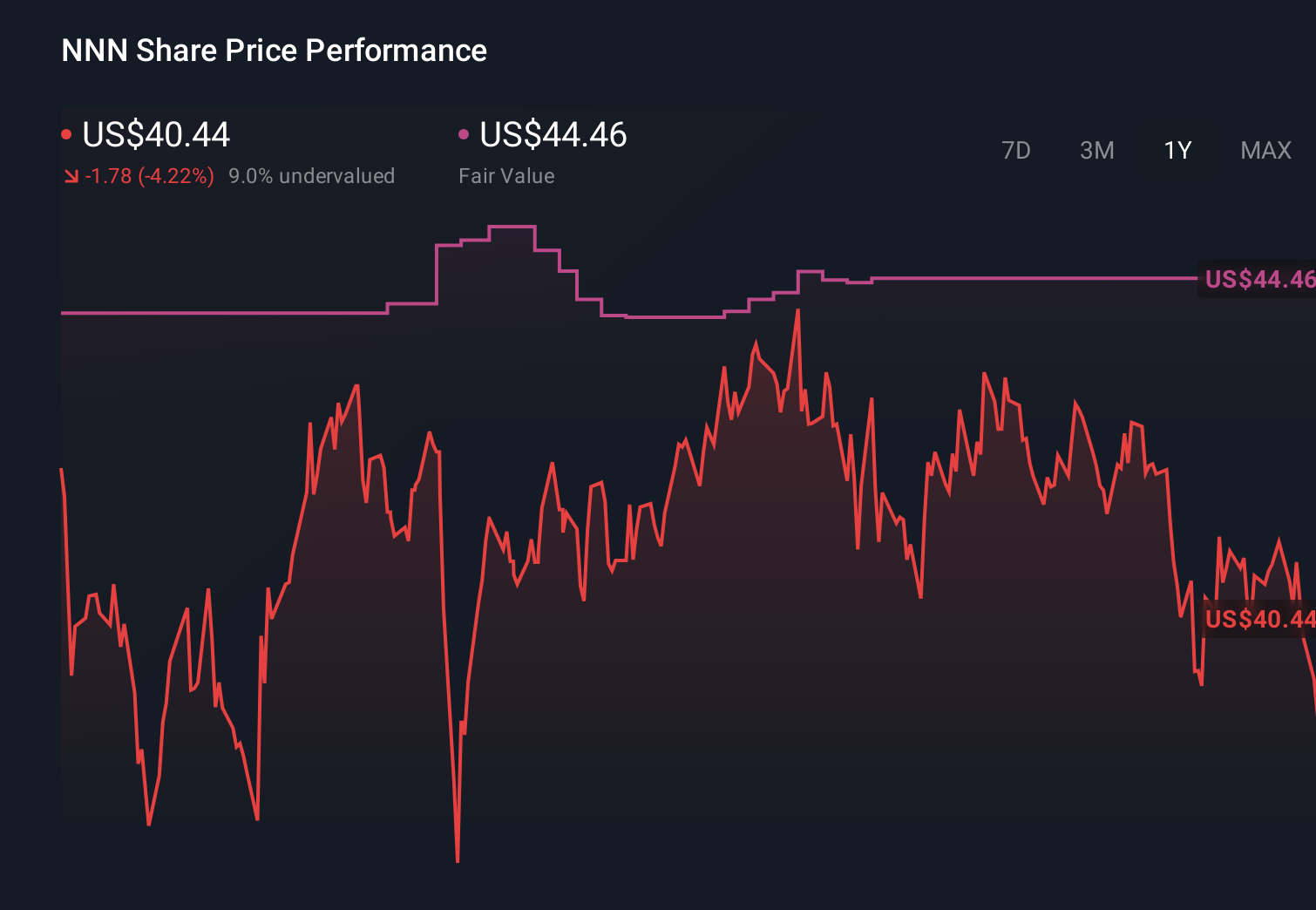

NNN REIT Investment Narrative Recap

To own NNN REIT, you need to believe in the durability of long-term, net-leased, necessity-based retail and the company’s ability to keep properties occupied while managing financing costs. The 3.3% dividend increase and 37-year growth streak reinforce its income-oriented identity, but do not materially change the near-term catalyst, which remains execution on disciplined acquisitions, or the key risk around tenant quality and potential retail bankruptcies that could pressure occupancy and cash flow.

The recent US$200 million incremental term loan, with SOFR partially fixed via swaps and slightly lower credit spreads, is the most relevant backdrop to this dividend news. It underscores how NNN is currently funding its portfolio while facing the risk that higher interest expense and less favorable debt markets could limit the cushion supporting future dividend growth and moderate earnings expansion, even as the company continues to emphasize necessity-based tenants and long-term leases.

Yet behind the 37-year dividend growth story, investors should be aware of the ongoing risk that retailer bankruptcies and consolidations could...

Read the full narrative on NNN REIT (it's free!)

NNN REIT's narrative projects $1.1 billion revenue and $448.9 million earnings by 2029. This requires 4.7% yearly revenue growth and a $62.4 million earnings increase from $386.5 million today.

Uncover how NNN REIT's forecasts yield a $46.23 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members see NNN’s fair value between US$46.23 and US$85.41 across 3 independent views, highlighting wide dispersion. You can weigh those opinions against the current risk that tenant distress and retailer bankruptcies could limit occupancy, soften earnings, and influence how sustainable the recent dividend increase truly feels over time.

Explore 3 other fair value estimates on NNN REIT - why the stock might be worth as much as 80% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NNN REIT research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NNN REIT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NNN REIT's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com