Otter Tail (OTTR) And The Earnings Mix Behind A Stock That Looks About Right

How Otter Tail Stock Looks After Recent Performance

Otter Tail (OTTR) has drawn fresh attention after a period of steady share performance, including a recent close at $90.18. This has prompted investors to reassess the utility and manufacturing company’s mix of businesses and earnings profile.

See our latest analysis for Otter Tail.

The recent move to $90.18 comes on top of a steady trend, with a 10.72% year to date share price return and a 21.54% total shareholder return over the past year suggesting momentum has been building rather than fading.

If Otter Tail’s mix of regulated utility and manufacturing businesses has you thinking about where else to look for resilient earnings, it can be useful to scan for companies plugged into long term grid and infrastructure themes via the 34 power grid technology and infrastructure stocks

With Otter Tail now close to analysts’ price target after its recent run, the real tension is between locking in exposure at today’s level or waiting for a pullback. How does the current valuation compare with its earnings mix?

Most Popular Narrative: 0.4% Undervalued

Otter Tail’s most followed narrative pegs fair value at $90.50, almost exactly in line with the latest $90.18 close. As a result, the story rests on the underlying earnings mix and long term capital plan rather than a big pricing gap.

The analysts have a consensus price target of $90.5 for Otter Tail based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.4 billion, earnings will come to $206.7 million, and it would be trading on a PE ratio of 22.7x, assuming you use a discount rate of 7.1%.

The fair value hinges on a detailed playbook that blends modest revenue growth, slimmer margins, and a richer earnings multiple. Curious which assumptions really carry the weight here? The narrative walks through exactly how future profits, payout on capital, and discount rate discipline add up to that $90.50 figure.

Result: Fair Value of $90.50 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Otter Tail’s story could change quickly if regulatory pressure on coal assets intensifies or if expected large new electricity loads fail to materialize.

Find out about the key risks to this Otter Tail narrative.

Another View on Otter Tail’s Valuation

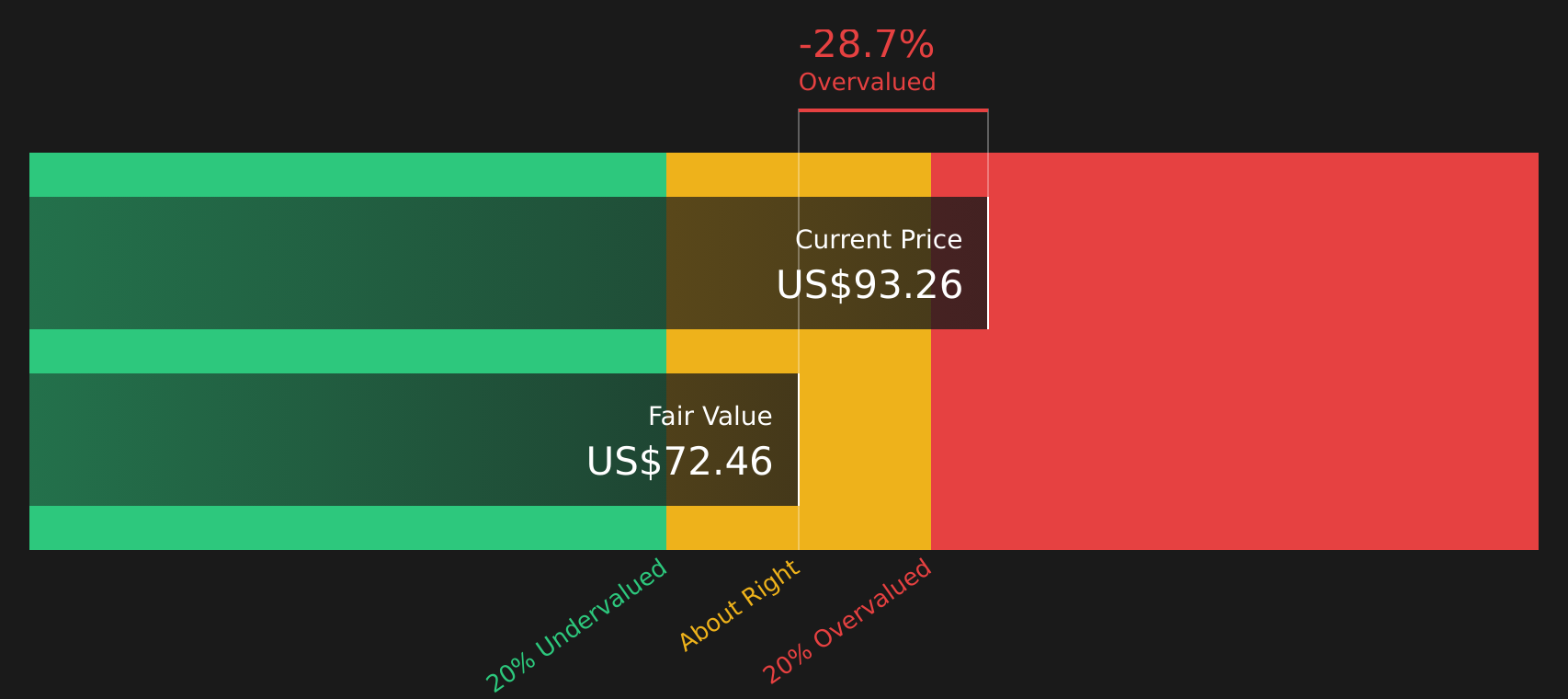

While the narrative fair value for Otter Tail sits close to the current $90.18 share price, the Simply Wall St DCF model comes in lower at about $72.46, which frames the stock as trading above that cash flow based estimate. Which set of assumptions aligns more closely with your own view of Otter Tail’s future?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Otter Tail for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals on Otter Tail leave you uncertain, consider this an opportunity to review the full picture and make a clear decision by weighing both the 1 key reward and 3 important warning signs

Looking for more investment ideas beyond Otter Tail?

If Otter Tail has sharpened your focus, do not stop here. Use the Simply Wall St Screener to uncover other stocks that could fit your portfolio.

- Target reliable income by reviewing 10 dividend fortresses that may appeal if you want yields backed by substantial cash flows.

- Hunt for potential value by checking screener containing 20 high quality undiscovered gems before more investors start paying attention to them.

- Strengthen your core holdings by focusing on solid balance sheet and fundamentals stocks screener (48 results) that can help anchor your portfolio in tougher markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com