Uber Stock Watch After The Delivery Hero Deal Through 3 Global Delivery Plays

Uber’s plan to acquire Delivery Hero for about €12.5b, at roughly €41 per share, is set to reshape the global food delivery market and could ripple across related stocks well beyond the deal’s immediate parties. With assets like Talabat, HungerStation, and Baemin set to change hands and parts of Delivery Hero headed to a US investment firm, investors are watching closely for potential winners and risks around consolidation and regulation. This article breaks down how that news could affect three stocks from our Global Food Delivery Platforms screener that appear positively exposed to the deal’s outcome.

Yixintang Pharmaceutical Group (SZSE:002727)

Overview: Yixintang Pharmaceutical Group is a Kunming based pharmacy retailer and distributor that runs a wide ranging chain of drugstores and related healthcare services across China, while also selling an assortment of consumer goods and services from medical devices and cosmetics to online health consultations and food delivery. The group blends traditional brick and mortar outlets with online channels, telecom and internet services, and various everyday services such as housekeeping, clinics and wellness offerings.

Market Cap: CN¥6.4b

Investors looking at the Uber and Delivery Hero deal may find Yixintang Pharmaceutical Group interesting because its food delivery operation gives it a direct link to sector consolidation while its core business remains anchored in essential healthcare retail. Recent results show CN¥16,736.33m in 2025 revenue and CN¥263.43m in net income, with net margin at 1.6%, so profitability is still thin but moving in the right direction. Analysts expect strong earnings growth and see upside to the current share price, yet the stock trades deeply below an estimated fair value and has underperformed the local consumer sector. Add in reliance on external borrowing and governance changes, and you have a complex story that deserves a closer look.

Yixintang Pharmaceutical Group looks like a thin margin healthcare staple that investors may be pricing as ordinary, while missing a bigger earnings story. See how the analyst forecasts for Yixintang Pharmaceutical Group could be masking one crucial twist

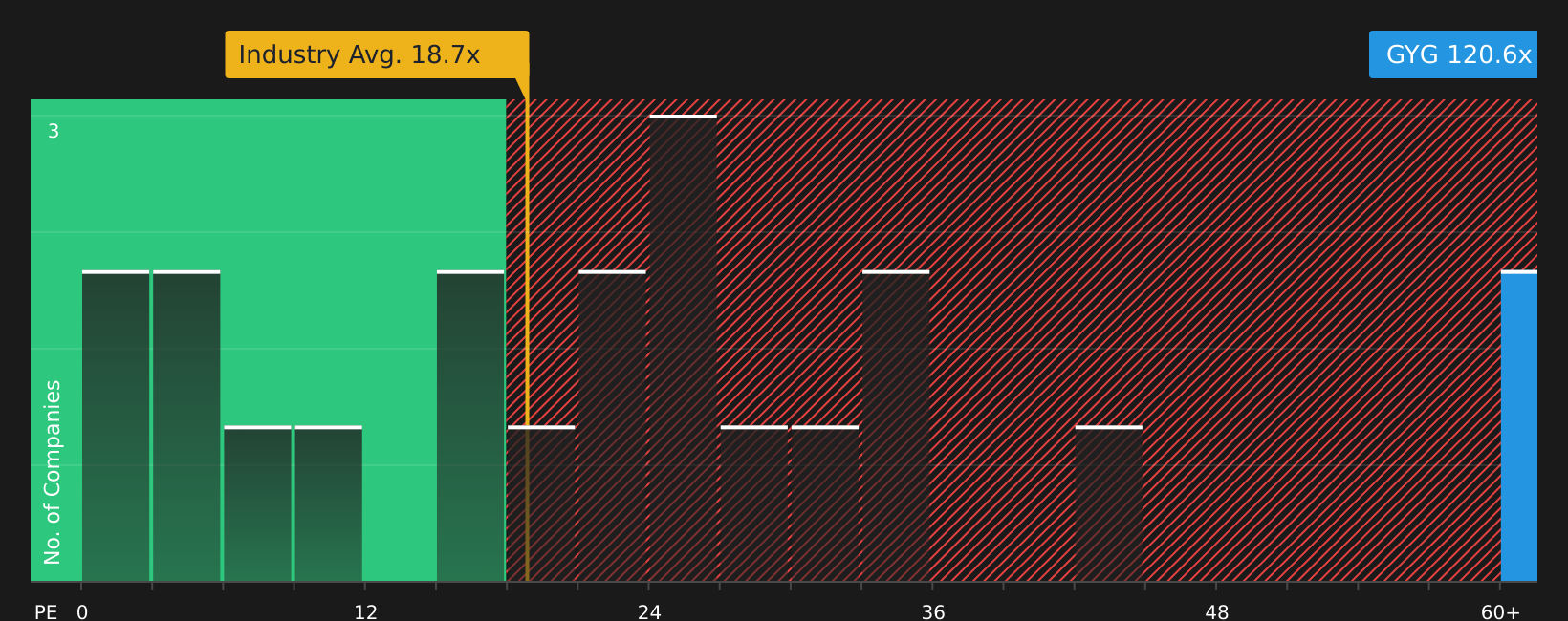

Guzman y Gomez (ASX:GYG)

Overview: Guzman y Gomez operates quick service restaurants serving Mexican inspired food across Australia, Singapore, Japan, and the United States, using a mix of dine in, drive thru, delivery, and digital channels, including a managed franchise network.

Operations: Guzman y Gomez generates A$516.47m in restaurant revenue, with A$483.94m from Australia and A$12.36m from the United States.

Market Cap: A$2.11b

Investors watching Uber’s Delivery Hero move may want Guzman y Gomez on the radar, because its exclusive partnership with Uber, growing digital ordering and delivery mix, and wellness branded menu put it squarely in the slipstream of any shift in how consumers order quick service meals. Forecast revenue and earnings growth, rising return on equity and high quality earnings sit alongside a very rich P/E multiple and a business that still relies on external borrowing. Recent index removals and leadership changes around the company secretary underline that sentiment can swing quickly. The key question is how this mix of growth, valuation tension and aggregator exposure compares with the rest of the sector, and what the Uber deal’s longer term impact may be.

Guzman y Gomez’s growth story and premium P/E look tightly linked to its Uber partnership and digital ordering mix, yet the crucial tension sits inside the analyst forecasts for Guzman y Gomez that could rewrite how this story ends

Wangsu Science & TechnologyLtd (SZSE:300017)

Overview: Wangsu Science & TechnologyLtd is a Shanghai based provider of edge computing, content delivery networks, cloud video, and security services that help businesses run faster and more securely across the internet, from streaming and gaming to finance, e commerce, and public sector clients.

Market Cap: CN¥35.81b

Wangsu Science & TechnologyLtd gives you direct exposure to the digital plumbing that underpins food delivery and other app based services in China, which is why the Uber and Delivery Hero deal matters. The stock screens as relatively good value versus the wider CN IT sector, with a P/E below both peers and an estimated fair value. Earnings are forecast to grow faster than the broader market even though recent growth has been modest and flattered by one off gains. Improving 16% net margins sit beside a volatile share price, full reliance on external borrowing and an unstable dividend record. The key consideration is how this mix of growth potential and funding risk could influence outcomes as demand for low latency delivery and security services increases across the platforms that run on Wangsu’s infrastructure.

Wangsu Science & TechnologyLtd’s earnings story and 16% net margin may not be fully reflected in how the stock is priced, but the real twist sits inside the analyst forecasts for Wangsu Science & TechnologyLtd that could change the risk balance

The three stocks covered here are just a starting point, as the full Global Food Delivery Platforms screener surfaces 22 more companies with equally compelling food delivery narratives that could reshape how you think about this theme. Use Simply Wall St to identify and analyze the specific catalysts and storylines that matter to you, so you can narrow your focus to the opportunities that best fit your portfolio.

Take Control of Your Investment Journey

If Yixintang Pharmaceutical Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Market themes move fast, and the next breakout stocks often build quiet momentum under the radar for now. Before the crowd catches on and pricing shifts, consider exploring new ideas.

- Spot early strength in financially resilient companies by scanning the list of solid balance sheet and fundamentals (418 results), which filters for cash-rich businesses that may respond when sentiment turns.

- Chase income potential with disciplined risk control by reviewing the 465 dividend fortresses, curated for yield seekers who want payouts designed to remain steadier when others drop.

- Track under followed opportunities before momentum takes off by working through the 505 high quality undiscovered gems, which highlights under-the-radar stocks with cleaner fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com