SIA Engineering (SGX:S59) Signs Air India MoU, Is The Stock Fully Valued?

MoU with Air India puts SIA Engineering’s India MRO ambitions in focus

SIA Engineering (SGX:S59) has drawn fresh attention after signing a non binding Memorandum of Understanding with Air India to explore Maintenance, Repair and Overhaul collaboration in India’s developing aviation hub.

The MoU builds on earlier agreements covering a 12 year inventory technical management arrangement for Air India’s Airbus A320 fleet and a base maintenance partnership in Bangalore. Taken together, these point to a broader framework for possible joint MRO development.

See our latest analysis for SIA Engineering.

SIA Engineering’s SGD3.35 share price has seen a 3.4% 30 day share price return after a softer recent week, while its 1 year and 5 year total shareholder returns of 4.1% and 78.4% point to interest that has built steadily over time around developments such as the Air India MoU.

If this India focused MRO story has caught your attention, it could be worth widening your watchlist using a screener that surfaces specialist infrastructure plays, such as 34 power grid technology and infrastructure stocks.

SIA Engineering now trades about 16% below the average analyst price target, even though an intrinsic value model implies a premium instead of a discount. Is the market fairly cautious after the recent MoU rally, or is it too restrained?

Price-to-Earnings of 22.2x for SIA Engineering: Is it justified?

On a P/E of 22.2x, SIA Engineering is priced higher than both its peer group average of 16.2x and the Asian infrastructure sector average of 13.3x. This signals a richer valuation at the current SGD3.35 share price.

The P/E multiple compares the share price to earnings per share, so it effectively shows how much investors are paying for each dollar of current earnings. For a service heavy business like SIA Engineering, where earnings quality is flagged as high and profit margins have improved from 11.2% to 11.9%, a premium multiple can sometimes reflect confidence in the durability of those earnings and in the wider MRO footprint, including agreements such as the Air India MoU.

However, the current 22.2x P/E not only stands well above sector and peer benchmarks, it also sits above an estimated fair P/E of 18.1x. That gap suggests the market is paying more than the level that the fair ratio implies, even though SIA Engineering’s earnings are forecast to grow 8.3% a year, slightly ahead of the broader Singapore market’s 7.1% forecast growth rate.

Explore the SWS fair ratio for SIA Engineering

Result: Price-to-Earnings of 22.2x (OVERVALUED)

However, SIA Engineering’s India MRO ambitions could face execution risk related to the non binding MoU, as well as exposure to wider aviation demand cycles.

Find out about the key risks to this SIA Engineering narrative.

Another view on SIA Engineering’s value

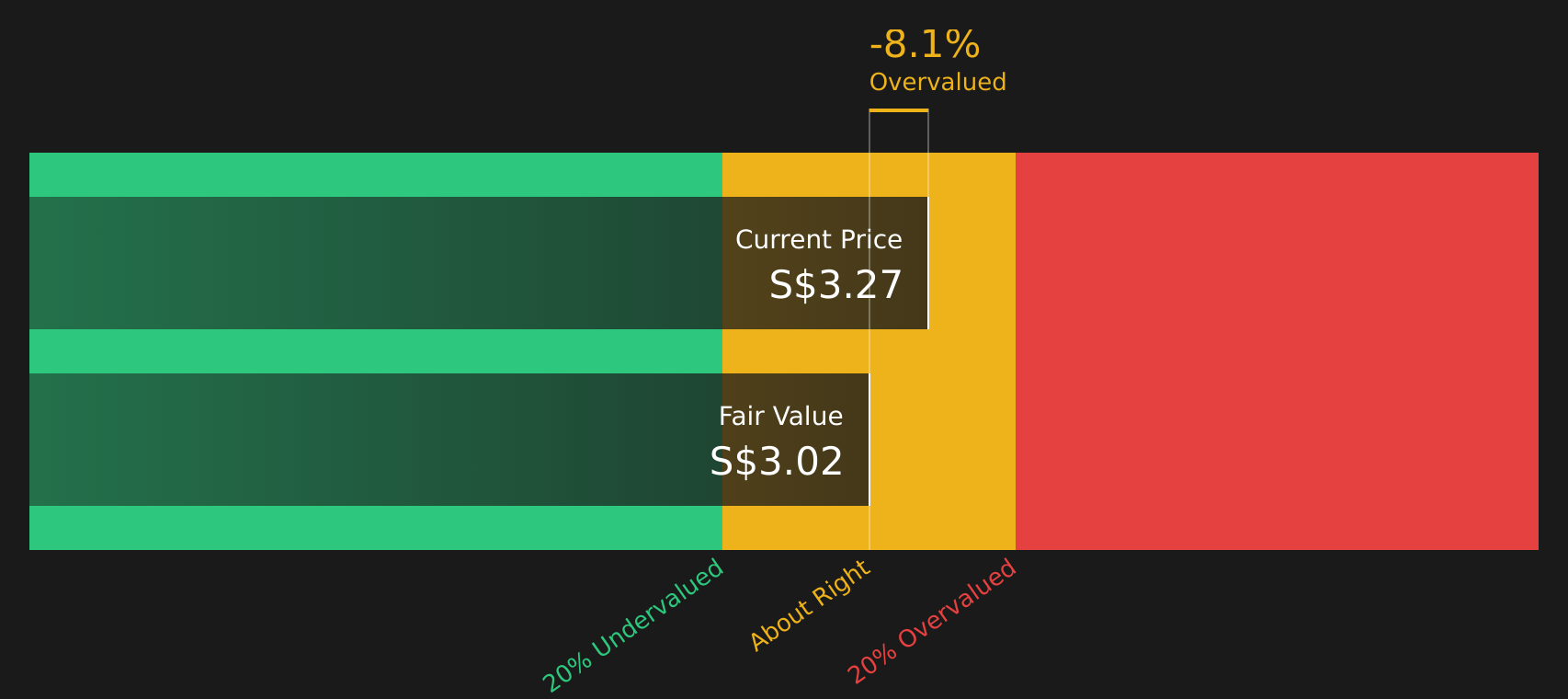

The earlier P/E check presents SIA Engineering as expensive, and the SWS DCF model points in the same direction. At SGD3.35, the stock trades above an estimated future cash flow value of SGD3.02, which suggests limited room for error if MRO growth in markets like India is slower than expected.

For a closer look at how this cash flow view is built, it is worth checking how the model treats revenue growth, margins, and reinvestment needs for SIA Engineering, then comparing that to your own expectations for the India MRO build out and wider aviation cycles. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SIA Engineering for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 215 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With SIA Engineering’s mixed signals on valuation, risk and opportunity, it makes sense to move quickly and stress test the numbers yourself using the 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond SIA Engineering?

If SIA Engineering has sharpened your focus, do not stop here. Broaden your opportunity set by checking other companies that meet clear quality and income filters.

- Target potential mispricings by scanning for companies that combine quality metrics with attractive valuations through the 215 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that offer higher yields and resilient payouts via the 463 dividend fortresses.

- Prioritise resilience by reviewing companies that score well on balance sheet strength and fundamentals using the solid balance sheet and fundamentals stocks screener (417 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com