Cleveland Cliffs Stock Looks Poised for a Lift From New Brazil Steel Tariffs

Fresh 25% U.S. tariffs on a wide range of Brazilian imports are set to reshape how money flows around the steel trade between the two countries, and that can quickly spill over into stock prices. Some companies could see relief from reduced Brazilian competition, while others may wrestle with higher costs or weaker export appeal. This article walks through three stocks from the US Brazil Trade Tension Steel Industry Impact Stocks screener, highlighting one that could stand to benefit from the new rules and two where the pressure from these tariffs may be harder to ignore.

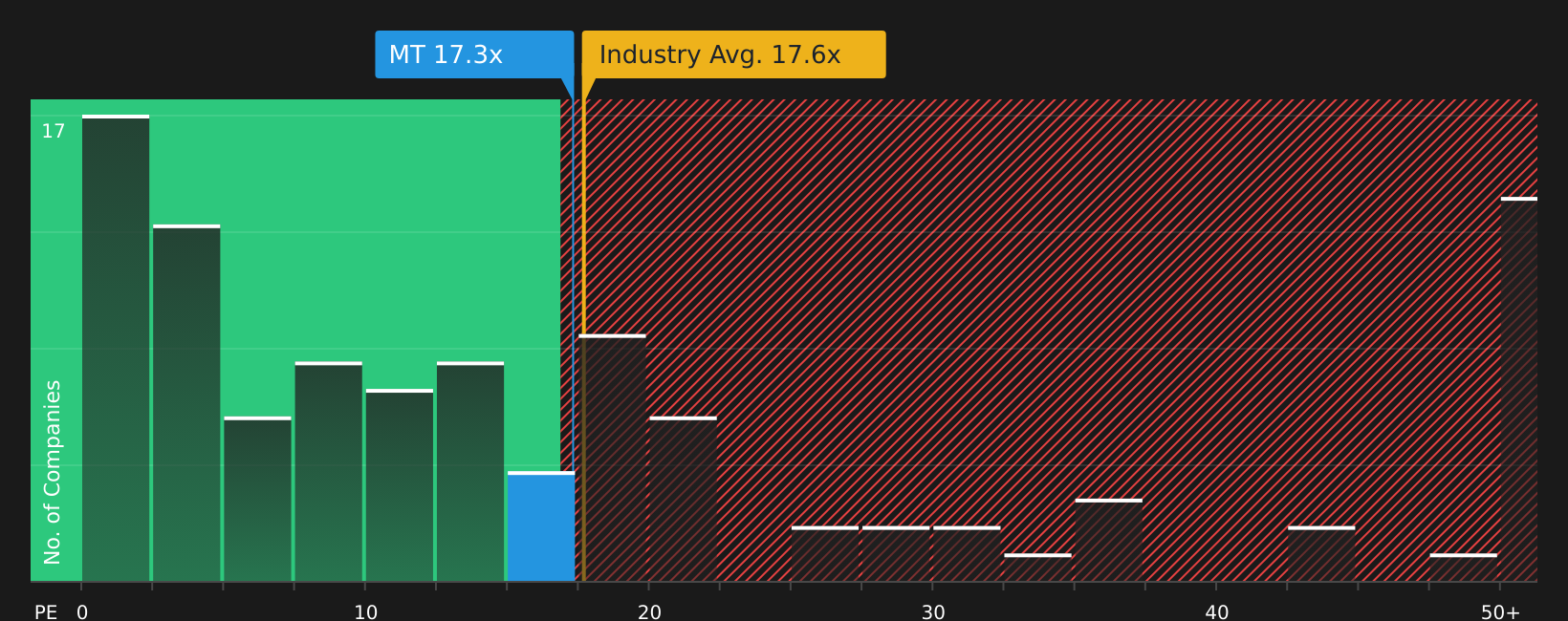

ArcelorMittal (ENXTAM:MT)

Overview: ArcelorMittal is a global steel and mining group that produces a wide range of flat and long steel products, tubes and mining outputs like iron ore and coking coal, supplying sectors such as automotive, construction, energy and machinery across the Americas, Europe, Asia and Africa.

Operations: ArcelorMittal generates revenue primarily from Europe at $29.0b, North America at $12.8b, Brazil at $11.3b, Sustainable Solutions at $10.5b and Mining at $3.4b, partially offset by a segment adjustment of $4.7b.

Market Cap: €44.6b

ArcelorMittal may look appealing with earnings growth, a P/E below peers and a discount to some fair value estimates. However, the new 25% U.S. tariffs on Brazilian imports put a direct question mark over its Brazil to U.S. steel flows and margin resilience. Management has discussed mitigating tariff effects through facilities like Calvert and flexible sourcing. At the same time, rising trade barriers, heavy decarbonization spending and global overcapacity all pull in the opposite direction. Adding in earnings boosted by one offs, share price volatility and higher funding risk from debt financing makes the story less straightforward. Investors focusing only on the green steel and automation headlines could miss how much of the current narrative depends on tight execution and policy outcomes that are outside the company’s control.

ArcelorMittal’s low P/E and tariff exposure could be masking a larger tension around margins, debt and execution, so it is worth reading the 4 key rewards and 2 important warning signs

Cleveland-Cliffs (CLF)

Overview: Cleveland-Cliffs is a vertically integrated U.S. and Canadian steel producer that mines iron ore, processes scrap, and turns these inputs into flat-rolled, stainless, electrical and tubular steel products used by automotive makers, infrastructure projects, manufacturers and distributors.

Operations: Cleveland-Cliffs generates most of its revenue from Steelmaking at US$18.4b, supplemented by Other Businesses at US$662m, partially offset by segment eliminations of US$124m.

Market Cap: US$5.6b

Cleveland-Cliffs is directly affected by the new 25% U.S. tariffs on Brazilian imports, as a domestically focused producer that does not depend on foreign supply chains and has been publicly supportive of tougher trade enforcement. With earnings still fragile, a history of losses and meaningful debt, the stock carries risk, particularly if tariff policy softens, auto demand is weaker than expected, or decarbonization costs rise faster than anticipated. For investors tracking how trade protection, vertical integration and automotive reshoring may influence U.S. steel producers, Cleveland-Cliffs provides a focused way to follow those themes as they are reflected in profits, balance sheet developments and pricing power over time.

Cleveland-Cliffs looks like a pure play on tougher trade enforcement, but the real story sits in how its balance sheet, pricing power and tariff support intersect. To explore these dynamics in more detail, start with the 3 key rewards and 3 important warning signs (1 is major!)

Gerdau (BOVESPA:GGBR4)

Overview: Gerdau is a long established Brazilian steel producer that supplies rebars, bars, wire products, plates, coils and special steels to customers in construction, automotive, energy, agriculture and mining across Brazil, North America and the rest of South America, and also owns iron ore mines in Brazil.

Operations: Gerdau generates most of its revenue from its North America business at R$36.4b and Brazil at R$28.5b, with South America contributing R$5.6b and segment eliminations of R$1.2b.

Market Cap: R$45.0b

Gerdau might catch your eye because of its exposure to North American steel demand, cost cutting projects and recent share buybacks, but the picture is complicated. Earnings fell sharply in recent years, profit margins are thin at 2.4%, and the stock trades on a rich P/E multiple while relying heavily on external borrowing and absorbing a R$2.0b one off loss in the last 12 months. The new 25% U.S. tariffs on Brazilian imports threaten a key export channel just as management is still pushing for stronger trade defenses at home, which could squeeze both volumes and pricing. Investors who stop at the growth forecasts and analyst upgrades risk missing how much tariff pressure, funding risk and insider selling are shaping the story for Gerdau.

Gerdau’s thin 2.4% margins, rich P/E and reliance on borrowing suggest something in the story is stalling just as tariffs bite. Before assuming the pressure is temporary, review the 1 key reward and 3 important warning signs

Take Control of Your Investment Journey

If Gerdau or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh stock ideas do not stay under the radar for long. Before momentum builds, spreads widen and the best entry points get caught by the crowd, move quickly and get in early.

- Target resilient cash generators by scanning a curated list of solid balance sheet and fundamentals (417 results) that keeps weak balance sheets off your radar while it still matters.

- Ride long term infrastructure momentum with a focused set of 34 power grid technology and infrastructure stocks positioned around grid upgrades and electrification before pricing fully reflects the story.

- Position ahead of the next materials cycle by reviewing a hand picked pool of 29 best rare earth metal stocks while they are still flying mostly under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com