Marks And Spencer Stock And 2 UK Retail Shares Backed By Easier Parking Rules

Parking charges rarely move markets, but the UK Competition and Markets Authority’s investigation into Euro Car Parks has put a fresh spotlight on how private parking practices affect where and how consumers shop. Stricter rules on parking operators could reshape the balance of power between forecourt operators, supermarkets and retail-focused petrol stations, with implications for customer loyalty and on-site spending. This article looks at 3 stocks from the UK Consumer Retail sector that are closely exposed to this news and explains how the same headline risk might be viewed as a potential positive for their underlying businesses.

Wickes Group (LSE:WIX)

Overview: Wickes Group is a UK focused home improvement retailer that helps both DIY customers and trade professionals with products and services spanning kitchens, bathrooms, heating, solar installations and full design and installation projects, sold through its stores, website and mobile apps.

Operations: Wickes Group generates all of its £1.6b revenue from retailing home improvement products and services in the United Kingdom.

Market Cap: £429.3m

Wickes Group sits at the crossroads of several themes that matter to retail investors right now, including demand for home upgrades, value focused pricing and how easily customers can reach physical sites. The company combines a high forecast return on equity, currently solid profit margins and active store rollout and refit plans with some clear pressure points such as wage inflation, reliance on external borrowing and a patchy dividend record. In addition, the UK parking crackdown could make it easier for shoppers and trade customers to access its forecourts and retail locations, potentially lifting volumes. The key question is whether current expectations already reflect these moving parts or if there is still something the market is overlooking.

Wickes Group’s mix of forecast return on equity, store investment and a cleaner parking backdrop could be masking a bigger story about expectations and risk. See how the 4 key rewards and 1 important warning sign might reframe the opportunity and the catch.

Marks and Spencer Group (LSE:MKS)

Overview: Marks and Spencer Group is a UK based retailer selling food, clothing, homeware and beauty products through its stores, online channels and international partners, with an additional stake in Ocado for grocery delivery and a small banking arm.

Operations: Marks and Spencer Group generates £9.7b from Food, £3.8b from Fashion, Home & Beauty, £3.2b from Ocado and £543.3m from International activities.

Market Cap: £7.7b

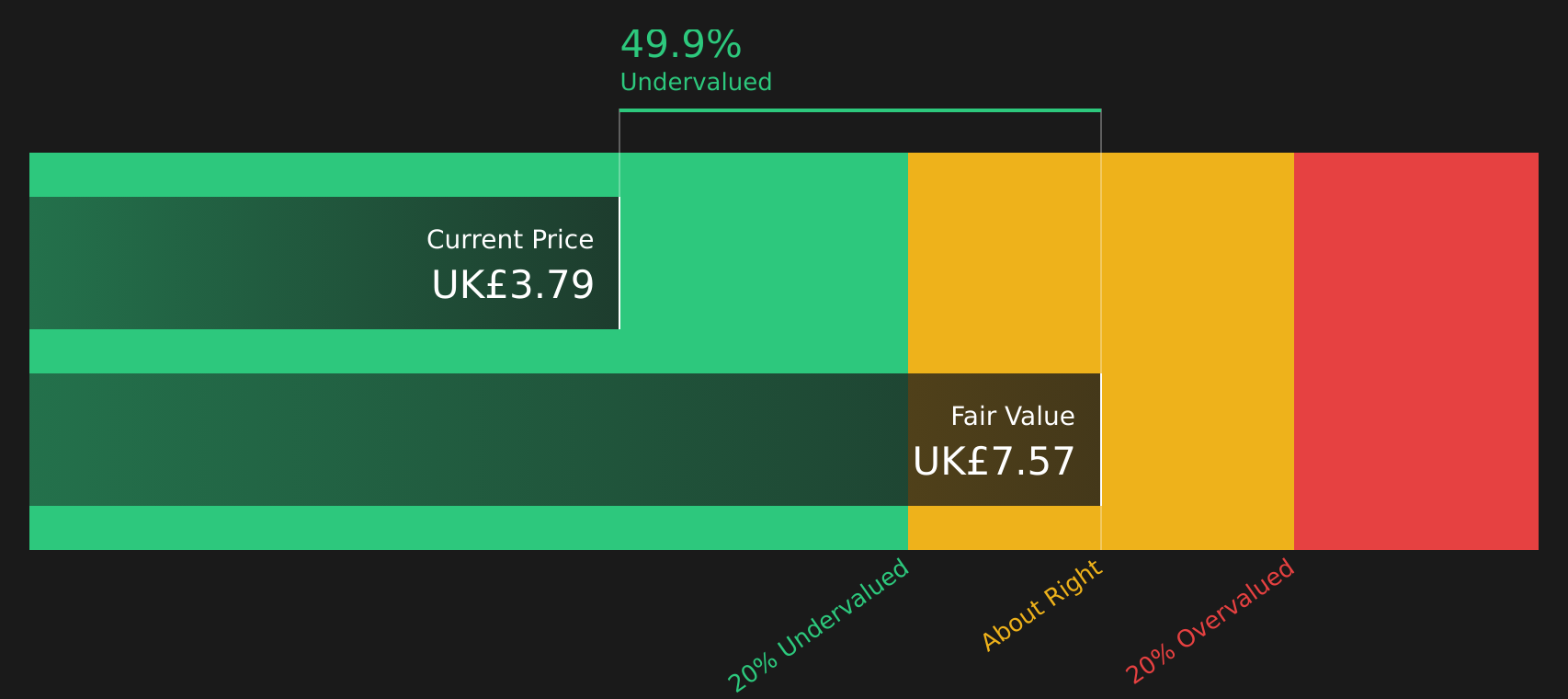

Marks and Spencer Group is worth a closer look if you are interested in how a large multi format retailer can use store investment, digital growth and supply chain upgrades to try to lift relatively thin margins, while benefiting from any improvement in customer access such as fairer parking rules. Analysts see scope for higher earnings and revenue over time. Yet the stock trades at what some models suggest is a discount to estimated future cash flows, with a P/E that is above peers but below one fair value estimate. At the same time, Ocado losses, ongoing regulatory costs and one off items keep risk firmly on the table and make it important to understand what is really driving the current valuation.

Marks and Spencer Group’s mix of digital growth, store investment and parking tailwinds is only half the story; the real tension is how the market is pricing that against risk in the analysis report for Marks and Spencer Group

NWF Group (AIM:NWF)

Overview: NWF Group is a UK based distributor of fuel oils, ambient groceries and animal feeds, running a nationwide fuels depot network, grocery warehousing and transport for supermarkets, and feed manufacturing for farmers.

Operations: NWF Group generates £604.2m from Fuels, £199.5m from Feeds and £88.6m from Food, with a small inter segment adjustment of £8.9m, almost all within the United Kingdom.

Market Cap: £68.7m

NWF Group provides exposure to fuel distribution, food logistics and agriculture in one relatively small UK focused stock. The CMA’s push for fairer parking rules may support forecourt traffic and customer loyalty at its fuel sites. The company offers a high dividend yield of 6.07% and revenue growth is forecast at 6.1% a year. However, margins are thin, earnings declined 33.8% over the past year and return on equity is only 6%, so there is clear execution risk. Analysts note that the shares trade below one DCF based fair value estimate of £2.44. At the same time, higher leverage and a board still bedding in mean investors need to weigh the income and growth story against financial resilience and governance quality.

NWF Group’s mix of fuel, food and agriculture exposure with a 6.07% yield and modest revenue growth forecasts hints at a more complex story. Start with the analyst forecasts for NWF Group and see what might be quietly changing.

The three stocks covered here are just a starting point, and the full UK Consumer-Retail Sector screener surfaces 15 more UK Consumer Retail companies with similarly detailed stories that could be worth your attention. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction ideas in this corner of the market.

Take Control of Your Investment Journey

If Marks and Spencer Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks

Some stocks move first, others follow. Before the next breakout gathers momentum and flies out of reach, build your shortlist of fresh ideas while it matters and be ready to act.

- Spot potential turnaround stories early by scanning curated companies in the 10 high quality undervalued stocks before the crowd catches on and pricing fully reflects their balance sheet strength.

- Explore structural shifts in automation and productivity by reviewing the carefully filtered group in the 32 robotics and automation stocks while these themes are still relatively under the radar.

- Focus on income opportunities through the hand picked 3 dividend fortresses instead of reacting only after payouts and prices have already adjusted.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com