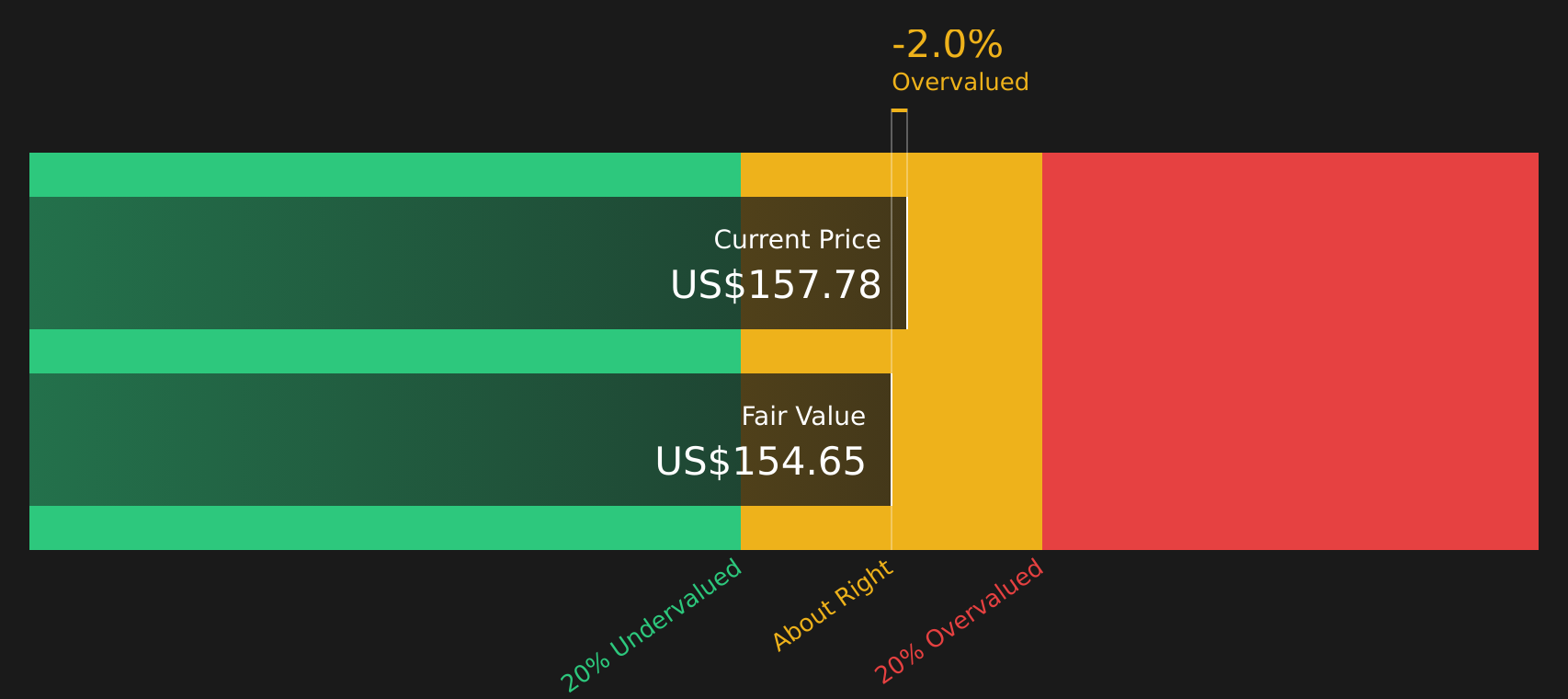

Kaiser Aluminum (KALU) Stock May Be 4% Overvalued After 2026 Growth Outlook

Kaiser Aluminum stock has delivered a 127.7% total return over the past three years, yet current valuation checks suggest it no longer looks like an obvious bargain. The Discounted Cash Flow (DCF) intrinsic value estimate points to a price that is roughly in line with where the shares trade today. After such a strong run, the core question for investors is whether recent growth expectations and operational progress are already well reflected in the current price.

- The 127.7% return over three years highlights how strongly Kaiser Aluminum has rewarded shareholders, which raises the bar for any further potential upside from here.

- Expectations for higher conversion revenues and profitability can support the valuation, but execution risks around demand, pricing, and cost control may limit how much investors are willing to pay ahead of proof in future cash flows.

- With a value score of 2 out of 6, Kaiser Aluminum screens as leaning expensive on the broader set of valuation checks rather than as a clear-cut bargain.

The issue now is whether Kaiser Aluminum's recent operational progress and growth outlook justify paying close to the intrinsic value estimate implied by the DCF work.

Is Kaiser Aluminum Fairly Priced on Cash Flow?

The Discounted Cash Flow (DCF) model uses projected future cash flows to estimate what Kaiser Aluminum might be worth today. For Kaiser Aluminum, the latest twelve month free cash flow is a loss of about $23.9 million, yet the model assumes recovering cash flows over time, with free cash flow turning positive and then settling into a more mature path.

On these assumptions, the DCF points to an intrinsic value of about $154.78 per share, which sits close to the current share price and implies the stock is roughly 3.6% above the modelled value. The recent guidance for higher 2026 conversion revenues and adjusted EBITDA helps explain why the market is willing to pay a price that broadly matches what the cash flow projections suggest.

Overall, Kaiser Aluminum stock appears to be roughly fairly valued on this DCF view, with the current price already reflecting the projected cash flow recovery.

Kaiser Aluminum is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

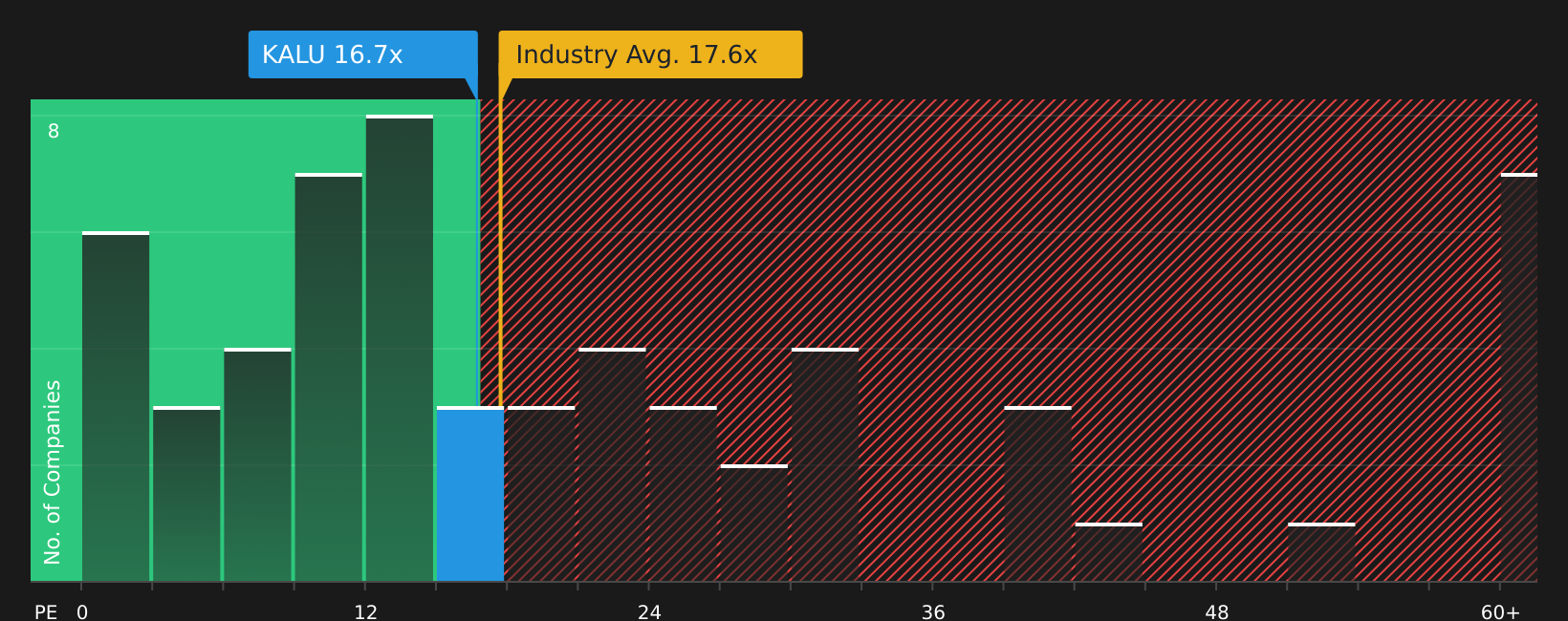

Where Does Kaiser Aluminum Sit on Earnings?

For Kaiser Aluminum, the P/E ratio is a useful cross check because earnings are a key focus for many investors in the Metals and Mining sector. The stock currently trades on a P/E of about 16.9x, which sits below the broader industry average of roughly 18.9x and above the peer group average of around 10.6x. That places Kaiser Aluminum at a modest premium to similar companies while still sitting slightly under the wider sector level.

The fair P/E ratio for Kaiser Aluminum is estimated at about 18.7x, which is only a little higher than where the stock trades now. This fair multiple reflects what investors might typically pay for a company with Kaiser Aluminum's earnings profile, risks, and sector positioning. The small gap suggests neither a clear discount nor an obvious premium on this measure.

Overall, Kaiser Aluminum appears roughly fairly valued on its P/E multiple, with the current price sitting close to the level implied by these earnings comparisons.

See what the numbers say about this price — find out in our valuation breakdown.

The Kaiser Aluminum Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the valuation work on Kaiser Aluminum leaves off by spelling out in plain terms which assumptions about Kaiser Aluminum's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. They sit within the Community page so you can see different views side by side. Rather than relying on a single multiple or model output, each Narrative lays out the assumptions behind its fair value so you can compare them with the actual results as they are reported.

Community views on Kaiser Aluminum are divided, with one camp seeing upside from capacity ramps and another focused on execution and valuation risk.

Bull case: 10% undervalued

"Ramp up of the Warrick coated packaging line, with coated products now around 75% of mix and long-term contracts in place, points to higher conversion revenue per pound and supports margin and EBITDA performance over time…"

Read the full Bull Case to see why Kaiser Aluminum could be undervalued

Bear case: roughly fairly valued

"Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high…"

Read the full Bear Case to see why Kaiser Aluminum could be overvalued

Do you think there's more to the story for Kaiser Aluminum? Head over to our Community to see what others are saying!

The Bottom Line

For Kaiser Aluminum, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple suggest the stock is priced at roughly about the right level rather than offering an obvious discount. The low value score implies that, across a wider set of checks, it leans on the expensive side even if no single model flags a clear mispricing. From here, the key question is whether Kaiser Aluminum can deliver on the expected improvements in cash generation and profitability, because any slip in that trajectory would make the current valuation harder to justify.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com