How Policy Setbacks to Ultium EV Batteries At General Motors (GM) Have Changed Its Investment Story

- A recent BlueGreen Alliance report found that President Donald Trump’s One Big Beautiful Bill Act led to very large cancellations and delays, around US$83.00 billion worth, in U.S. clean energy, manufacturing, and industrial projects, including General Motors’ Ultium Cell EV battery initiative with LG Energy Solution.

- At the same time, General Motors’ emphasis on full-size SUVs and pickups in the Middle East, where these vehicles made up 44% of sales between 2000 and 2025, highlights how its regional product mix and safety-focused technology contrast with policy-related headwinds for its U.S. clean energy and EV projects.

- We’ll now examine how policy-driven setbacks to GM’s Ultium Cell EV battery project could affect the company’s investment narrative and long-term positioning.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

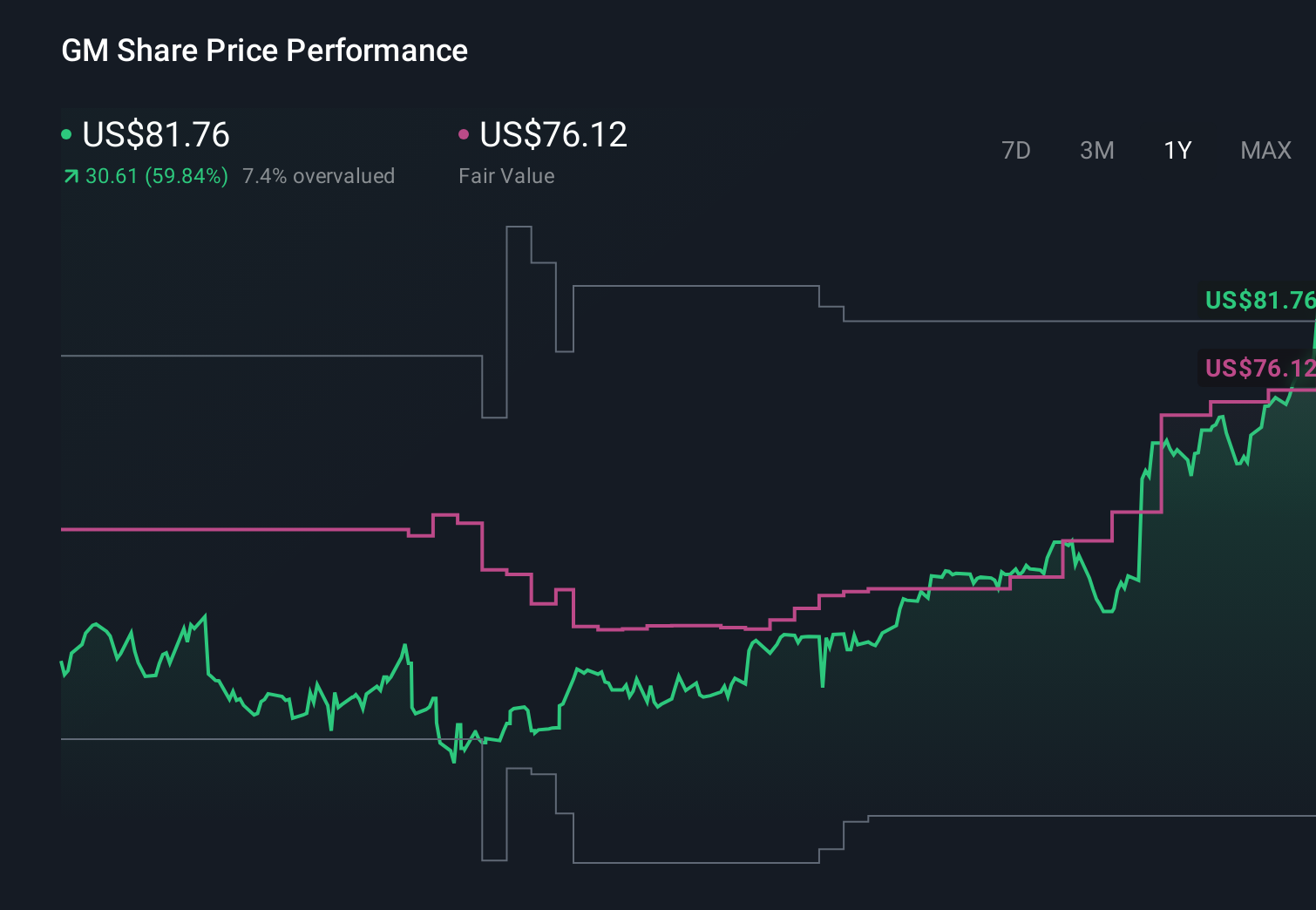

General Motors Investment Narrative Recap

To own GM today, you need to believe it can balance profitable truck and SUV sales with a credible transition toward electrification and software-driven revenue. The BlueGreen Alliance findings around US$83.00 billion in project disruptions, including GM’s Ultium Cell EV battery initiative, highlight policy risk to that transition, but they do not fundamentally alter the near term catalyst of EV execution and software monetization or the key risk of capital-heavy EV investment facing shifting regulations.

Against this backdrop, GM’s recent strategic customer agreement with Micron Technology stands out. Securing long term supply of advanced memory and storage for future vehicles directly supports GM’s push into more software intensive EVs and driver assistance features. For investors watching how policy headwinds might slow Ultium progress, this kind of supply chain reinforcement speaks to GM’s efforts to keep its technology roadmap on track despite external shocks.

Yet even with GM’s strong SUV and pickup mix, investors should be aware that tighter emissions rules or further policy shifts could quickly pressure those high margin segments and...

Read the full narrative on General Motors (it's free!)

General Motors' narrative projects $195.5 billion revenue and $10.8 billion earnings by 2029. This requires 1.9% yearly revenue growth and a $8.4 billion earnings increase from $2.4 billion today.

Uncover how General Motors' forecasts yield a $94.81 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts already assumed only about US$188.5 billion of revenue and US$10.2 billion in earnings by 2029, so if you are worried about policy delays to Ultium and heavier reliance on trucks and SUVs, their much more pessimistic view shows just how far expectations can differ and why it may be worth comparing several scenarios before deciding where you stand.

Explore 7 other fair value estimates on General Motors - why the stock might be worth 14% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Motors research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free General Motors research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Motors' overall financial health at a glance.

No Opportunity In General Motors?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com