Is Del Monte (DMC) Trading At A Premium As Earnings Improve?

Del Monte stock has delivered a 22.5% gain over the past three years, yet its valuation signals are split, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to a premium to the current fundamentals while market multiples suggest the shares may still be priced below what the earnings profile implies.

- Over the last three years, Del Monte has returned 22.5%, which puts recent share price swings in the context of a longer period of steady, but not spectacular, gains.

- Recent coverage has focused on Del Monte's acquisition driven growth ambitions and expansion into upcycled fruit extracts, which can support higher revenue and cash flow over time, but investors also need to weigh execution risk and the possibility that expected earnings improvements take longer or cost more than hoped.

- Del Monte only passes 2 of 6 valuation checks on Simply Wall St's broader framework, which means that despite some supportive signals, the stock leans more expensive than cheap overall on standard valuation measures such as cash flows, assets and earnings multiples (2/6 valuation score).

The issue now is whether Del Monte's current share price at around US$29.35 is high relative to its intrinsic value estimate and recent performance, or if the conflicting signals still leave room for a reasonable entry point.

Find out why Del Monte's -10.2% return over the last year is lagging behind its peers.

Is Del Monte Getting Expensive on Cash Flow?

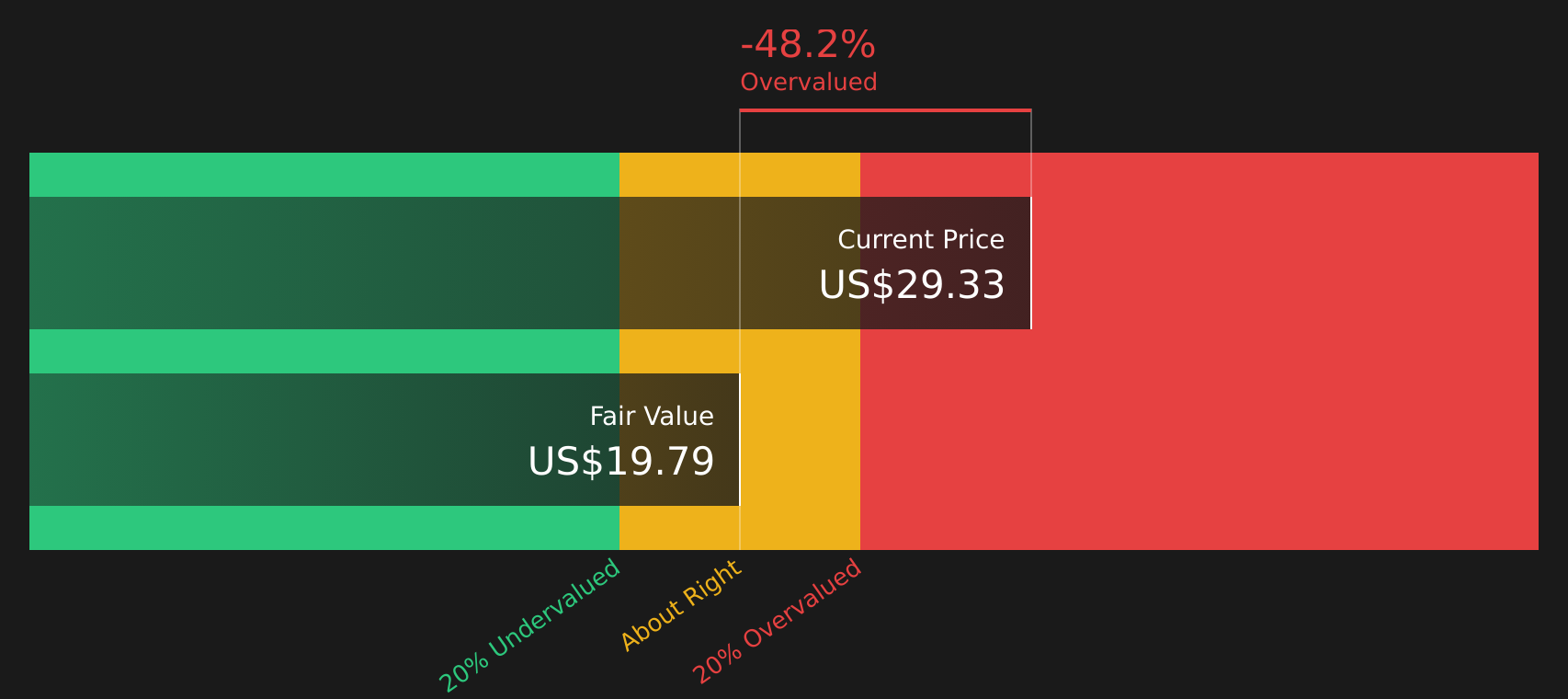

The Discounted Cash Flow (DCF) method estimates what Del Monte is worth today based on the cash it is expected to generate in the future. For Del Monte, the latest twelve month free cash flow sits at about $184.1 million, and the model assumes cash flows ease back from that level before settling into a relatively steady pattern rather than strong growth.

On those assumptions, the DCF model points to an intrinsic value of around $19.79 per share, which is well below the current share price of about $29.35. This implies the stock screens as roughly 48.3% overvalued. Because the acquisition of former Del Monte Foods assets is already well flagged as a potential earnings boost, the premium price suggests the market is assigning a lot of credit to that opportunity already.

Putting it together, Del Monte stock currently looks overvalued relative to what its projected cash flows support.

Our Discounted Cash Flow (DCF) analysis suggests Del Monte may be overvalued by 48.3%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Does Del Monte Look Undervalued on Earnings?

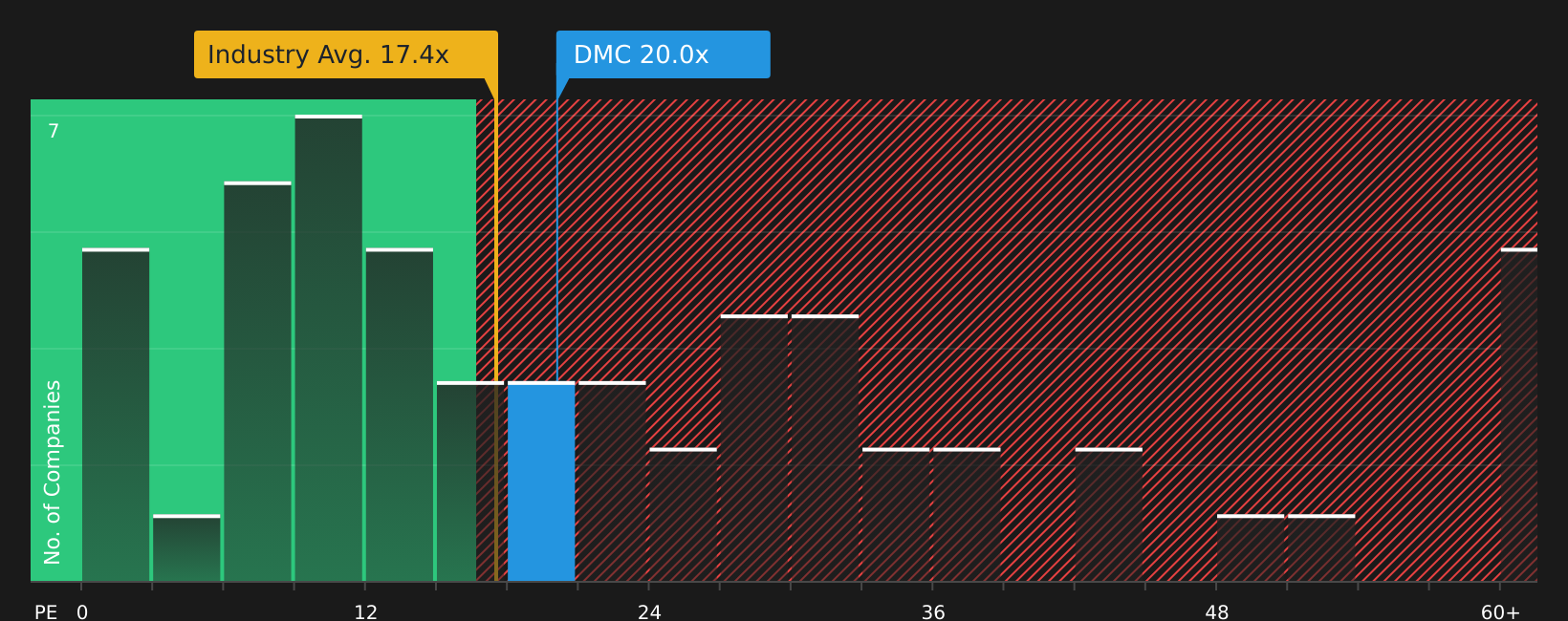

The P/E ratio suits Del Monte because earnings are a key focus for investors in established food businesses. Del Monte currently trades on a P/E of about 20.1x, which is above the Food industry average of around 17.2x but below the peer group average of roughly 23.6x, so the stock sits between broader sector pricing and closer peers.

On Simply Wall St's model, the fair P/E multiple for Del Monte is estimated at about 38.5x, which is materially higher than the current 20.1x. That gap suggests the market is not fully reflecting what this framework implies for Del Monte given its mix of growth prospects, margins, scale and risk profile, even after the attention on its acquisition of former Del Monte Foods assets and expansion into upcycled fruit extracts.

Overall, Del Monte stock appears undervalued on the P/E multiple relative to the model's fair ratio and to closer peers.

See what the numbers say about this price — find out in our valuation breakdown.

The Del Monte Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the Del Monte valuation puzzle a step further by spelling out what would need to happen to Del Monte's growth, margins and earnings for the stock to be worth materially more or less than today's price, using scenarios shared on the Community page. Rather than a single P/E or DCF output, each narrative lays out the assumptions behind its fair value so you can compare those expectations with future results as they are reported.

If you have a number driven view on whether Del Monte's acquisition of former Del Monte Foods assets and its move into upcycled fruit extracts really supports today's price, share a Narrative on Del Monte to put your assumptions on the record. It is a chance to be one of the early voices in the Simply Wall St community and see how your thesis stacks up as new results and updates arrive.

Do you think there's more to the story for Del Monte? Head over to our Community to see what others are saying!

The Bottom Line

For Del Monte, the Discounted Cash Flow (DCF) view points to the stock trading well above its intrinsic value, while the earnings multiple suggests it screens as undervalued relative to the model's fair P/E and closer peers. That split largely reflects a tension between cash flow timing and capital needs on one side, and expectations for growth and re rating on the other. With broader valuation checks scoring weakly, the multiple based upside case sits on shakier ground than a simple P/E gap might imply. The real swing factor from here is whether the acquisition and upcycled products translate into durable earnings without stretching cash flows too thin.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com