Operational Momentum And Buybacks Might Change The Case For Investing In Woodward (WWD)

- In recent months, Woodward (NASDAQ: WWD) has reported multi-year revenue and earnings per share growth, supported by improved operating efficiency and fixed cost leverage, with share repurchases further lifting per‑share results.

- This combination of operational momentum and capital returns is sharpening attention on how Woodward balances its growth ambitions with concentration risk among major aerospace customers.

- We’ll now examine how Woodward’s sustained revenue and earnings expansion may influence its existing investment narrative and future expectations.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Woodward Investment Narrative Recap

To own Woodward today, you need to believe in its role as a key supplier to major aerospace and industrial customers, while accepting customer concentration and capital intensity as core risks. The recent confirmation of multi‑year revenue and EPS growth, amplified by buybacks, feeds directly into the main near term catalyst: upcoming earnings on July 29, 2026. At the same time, it does little to reduce concerns about reliance on a handful of large OEM programs.

The upcoming Q3 fiscal 2026 results date is the most relevant recent announcement, because it creates a clear checkpoint where the market will reassess whether Woodward’s strong share price gains and elevated earnings multiples still line up with its operating performance. With the stock already pricing in years of solid execution, any update on margins, backlog quality or customer mix could either reinforce the current growth narrative or bring concentration and valuation risk into sharper focus.

Yet behind the strong numbers, investors should be aware of how concentrated Woodward remains in a small group of large aerospace customers...

Read the full narrative on Woodward (it's free!)

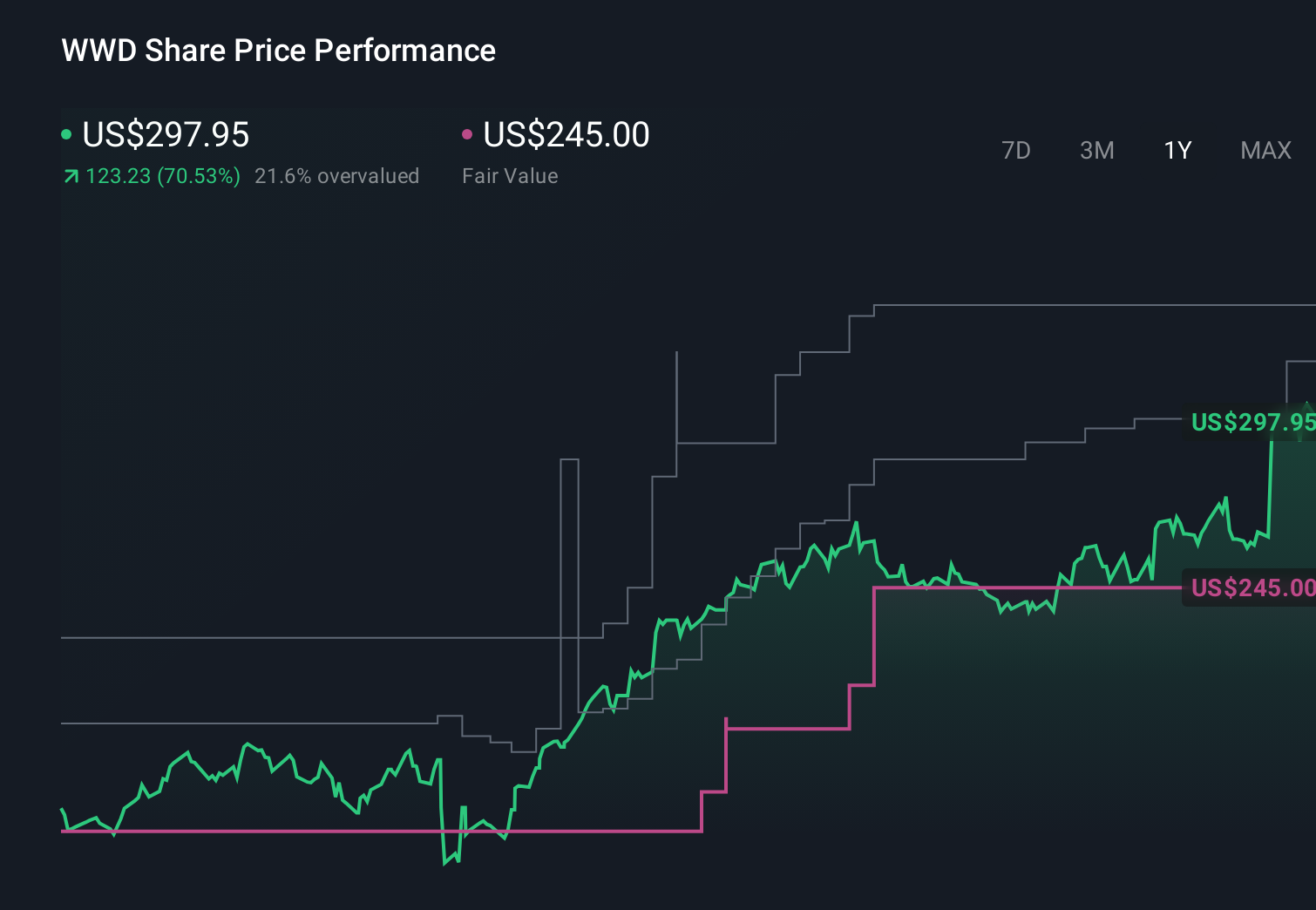

Woodward's narrative projects $5.1 billion revenue and $749.1 million earnings by 2029. This requires 8.6% yearly revenue growth and about a $235 million earnings increase from $513.8 million today.

Uncover how Woodward's forecasts yield a $444.55 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue near US$5.7 billion and earnings around US$885.7 million by 2029, which is far more upbeat than consensus and could look either more realistic or more stretched once the latest growth and margin trends are fully reflected.

Explore 6 other fair value estimates on Woodward - why the stock might be worth 34% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Woodward research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Woodward research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woodward's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com