Is Adaptive Biotechnologies (ADPT) Below Fair Value Or Too Pricey On Sales?

Adaptive Biotechnologies has delivered a strong 183.7% return over the past three years, yet the valuation signals are split, with the Discounted Cash Flow (DCF) intrinsic value implying the stock trades below that estimate while market based multiples lean the other way.

- Over the last three years, the share price return of 183.7% highlights how strongly sentiment has shifted toward Adaptive Biotechnologies and raises the bar for what the current valuation needs to justify.

- Expectations around the company turning its technology into scalable, cash generative revenue streams can support the current price, but execution risk and the timing of those cash flows may weigh on what investors are willing to pay today.

- Adaptive Biotechnologies screens as undervalued on the Discounted Cash Flow (DCF) estimate, yet scores only 1 out of 6 on broader valuation checks, which points to a stock that does not look like a straightforward bargain once other metrics are considered.

The issue now is whether the recent share price strength in Adaptive Biotechnologies is still leaving a reasonable margin between the traded price and its intrinsic value, or whether the rally has already used up most of that gap.

Is Adaptive Biotechnologies a Bargain on Cash Flow?

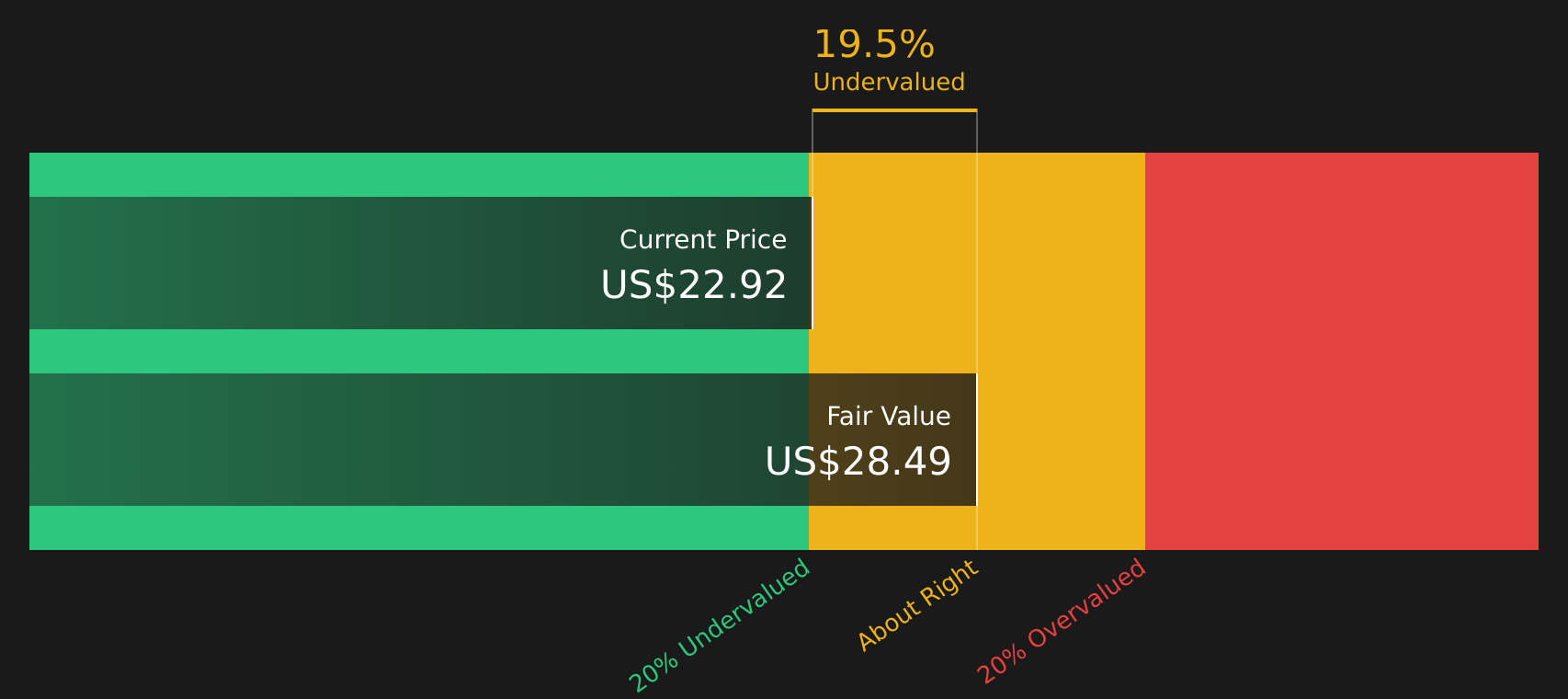

The Discounted Cash Flow (DCF) method values Adaptive Biotechnologies by projecting its future free cash flows and discounting them back to today. For the latest twelve months, the company reported a free cash flow loss of about $33.8 million, so the current valuation relies heavily on expectations that cash generation improves rather than on existing surplus cash.

In this model, cash flows are assumed to move from that loss into a growing, positive stream over time, which results in an estimated intrinsic value of about $28.41 per share. Compared with the current share price, this implies the stock trades at about a 19.3% discount to that estimate, so the DCF indicates Adaptive Biotechnologies is attractively priced if those cash flow assumptions are met.

On this DCF view, Adaptive Biotechnologies stock appears undervalued relative to the cash flows analysts expect it to produce.

Our Discounted Cash Flow (DCF) analysis suggests Adaptive Biotechnologies is undervalued by 19.3%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Does Adaptive Biotechnologies Look Pricey on Sales?

P/S is a useful yardstick for Adaptive Biotechnologies because revenue is a cleaner reference point than earnings while the company is still reporting losses.

Adaptive Biotechnologies currently trades on a P/S of about 12.4x, compared with a Life Sciences industry average of roughly 4.0x. Even when set against a closer peer group average of about 9.3x, the stock still carries a clear premium. The Fair Ratio model, which factors in the company’s profile and risks, points to a P/S closer to 4.8x, so the current multiple sits well above that level.

That wide gap means the market is already attaching a high value to each dollar of Adaptive Biotechnologies revenue, especially relative to both industry and peer benchmarks.

On this P/S view, Adaptive Biotechnologies stock appears overvalued relative to the multiple indicated by the Fair Ratio model.

See what the numbers say about this price — find out in our valuation breakdown.

The Adaptive Biotechnologies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this Adaptive Biotechnologies valuation puzzle leaves off by spelling out the specific paths for growth, margins and earnings that could make the stock worth materially more or less than it is today, and they sit on Simply Wall St's Community page. Each one links its number to a clear view of how Adaptive Biotechnologies' growth, profitability and risks might evolve, giving you a reference point to revisit as new information comes through.

Community narratives on Adaptive Biotechnologies sit far apart, with one cohort seeing upside from faster adoption and another focused on execution and profitability risks.

Bull case: 8% undervalued

"Analyst consensus points to mid-teens percent price improvements and higher volume from payer contracts and ASP uplift, but coverage and pricing wins are happening faster and with broader scope than expected..."

Read the full Bull Case to see why Adaptive Biotechnologies could be undervalued

Bear case: 14% overvalued

"Prolonged unprofitability at the total company level, with continued operating losses ($25.6 million net loss for the quarter) and ongoing cash burn even though improving could require dilutive capital raises or further cost-cutting..."

Read the full Bear Case to see why Adaptive Biotechnologies could be overvalued

Do you think there's more to the story for Adaptive Biotechnologies? Head over to our Community to see what others are saying!

The Bottom Line

For Adaptive Biotechnologies, the Discounted Cash Flow (DCF) intrinsic value points to a meaningful discount to the current share price, while market based multiples, including P/S, indicate the stock screens as overvalued against peers. That split, combined with weak broader valuation checks, suggests the DCF upside depends on future cash generation that is not yet reflected in fundamentals. The crux is whether Adaptive Biotechnologies can translate its technology into sustained, profitable revenue quickly enough to support the intrinsic value estimate, rather than the current premium multiple proving to be ahead of what the business ultimately delivers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com