How Life Time’s New Brea Flagship Expansion Could Shape the Premium Strategy for LTH Investors

- Life Time, Inc. has opened its Life Time Brea Athletic Country Club at Brea Mall in North Orange County, creating a nearly 123,000-square-foot, resort-style fitness and wellness destination with extensive indoor and outdoor amenities.

- This expansion deepens Life Time’s role as an anchor tenant in high-traffic retail settings, underscoring its focus on premium, comprehensive lifestyle offerings across affluent markets.

- Next, we’ll examine how adding a large, premium Brea club may influence Life Time’s investment narrative around affluent-market expansion.

Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

Life Time Group Holdings Investment Narrative Recap

To own Life Time, you need to believe its premium, high-amenity clubs can support steady membership and ancillary revenue while funding a capital-intensive expansion model. The Brea opening fits the affluent, large-format playbook, but it also adds to near term capital needs. For now, the key catalyst remains execution on new clubs and ancillary services, while the biggest risk continues to be heavy capex and reliance on real estate financing. The Brea news does not materially change that balance.

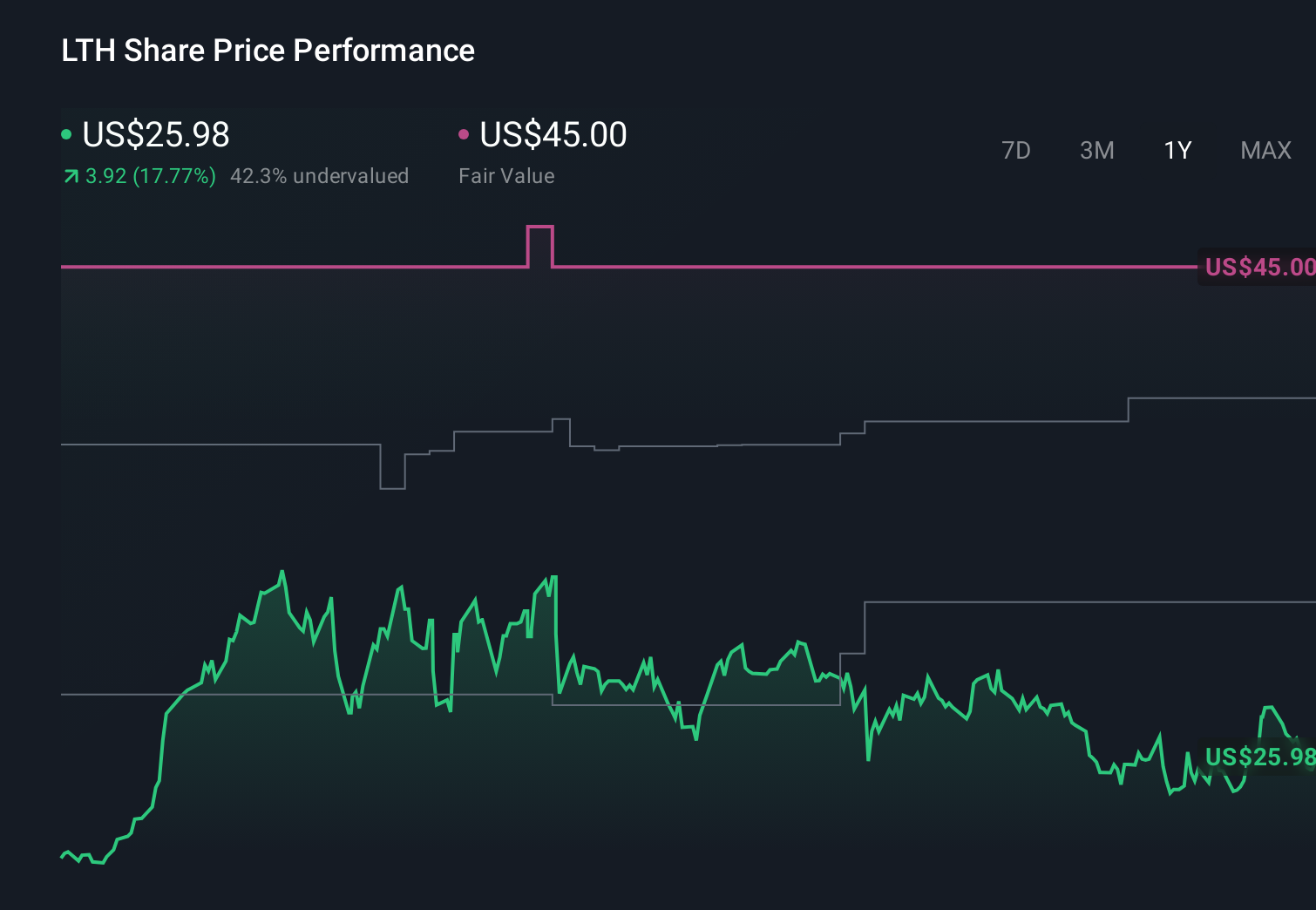

The most relevant recent announcement alongside Brea is Life Time’s raised 2026 guidance, with revenue now guided to US$3,320 million to US$3,350 million and net income to US$340 million to US$345 million. This guidance was set before Brea opened, so investors will be watching whether large, premium additions like Brea help the company stay within those targets while managing debt and sale leaseback activity, which sit at the heart of both the growth story and its financial risk.

Yet beneath Life Time’s premium club growth, there is a financing risk investors should be aware of if sale leaseback markets or borrowing costs were to...

Read the full narrative on Life Time Group Holdings (it's free!)

Life Time Group Holdings' narrative projects $4.2 billion in revenue and $434.5 million in earnings by 2029.

Uncover how Life Time Group Holdings' forecasts yield a $41.00 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue would reach about US$4.2 billion and earnings roughly US$423 million by 2029, so you should recognize that their more pessimistic view on expansion risk could either be reinforced or softened once results from Brea and similar openings are fully reflected.

Explore 2 other fair value estimates on Life Time Group Holdings - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com