Diamondback Energy (FANG) Stock Looks Fairly Priced Despite Pre Earnings Pullback

Diamondback Energy stock has delivered a very strong 208.9% return over the past 5 years. With the latest checks pointing to an about-right market multiple and a mixed overall value score, the question is whether the current price still offers an appealing entry point or largely reflects that strength.

- Over 5 years, Diamondback Energy has returned 208.9%, which puts recent gains in context and raises the bar for any new upside to be supported by fundamentals.

- Expectations around oil-linked cash generation can support today’s valuation, while sensitivity to crude prices and geopolitical shocks may challenge how much investors are willing to pay for those earnings.

- The stock scores 3 out of 6 on the valuation checks, which points to a mixed picture rather than a clear bargain or clear overvaluation.

For investors, the debate is whether Diamondback Energy’s strong track record and earnings power justify paying close to what the current market multiples imply, or if patience is more appropriate at these levels.

Is Diamondback Energy Fairly Priced on Sales?

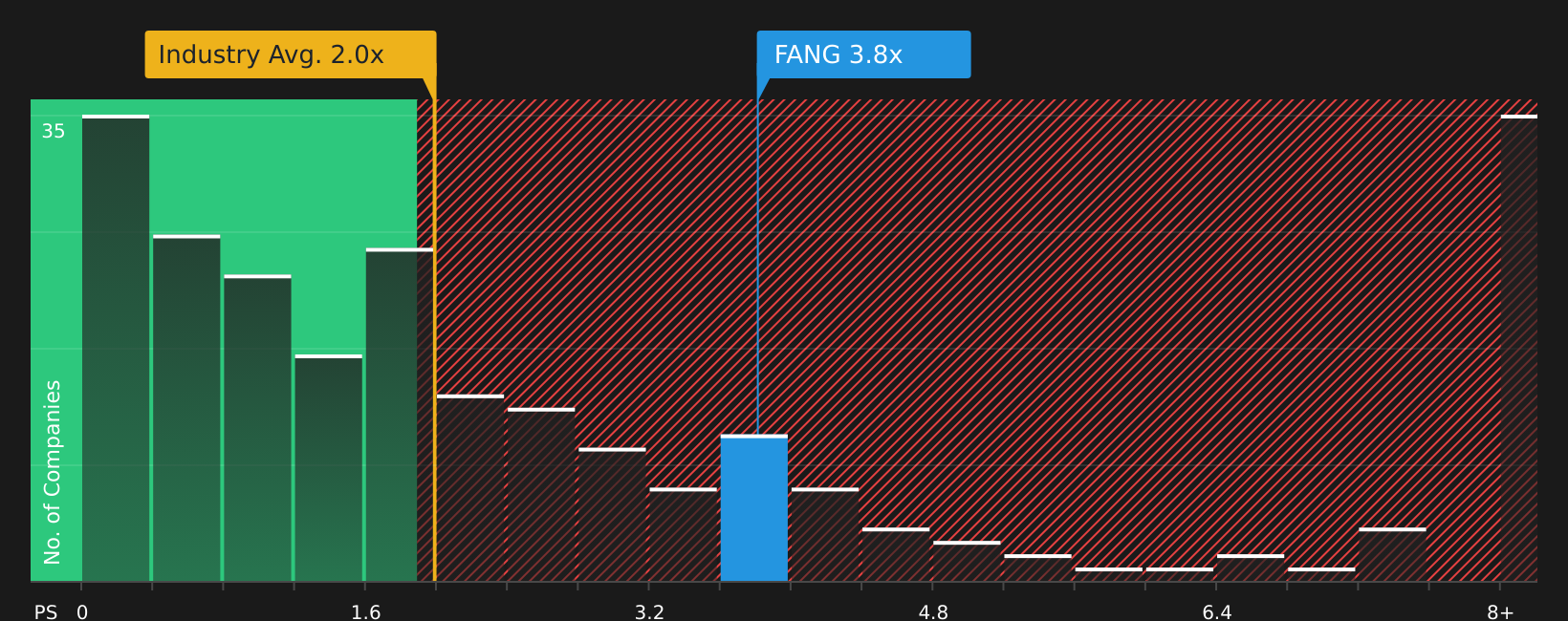

The P/S ratio suits Diamondback Energy because revenue is closely tied to commodity prices and production volumes, which investors often watch more than accounting earnings for producers like this.

Diamondback Energy currently trades on a P/S of about 3.8x, compared with an Oil and Gas industry average of about 2.0x and a peer group average around 11.0x. A more tailored fair P/S ratio for the stock is estimated at roughly 3.7x, which is very close to where the shares are now. That suggests the market is pricing the company at a modest premium to the sector overall, but far from the upper end of the peer range.

Despite recent news coverage highlighting both pullbacks and rallies in the stock around oil price swings and geopolitical headlines, the current P/S still points to Diamondback Energy being priced in line with what its revenue profile and risk level might justify.

On the P/S multiple, Diamondback Energy looks priced roughly in line with what this framework suggests is fair.

See what the numbers say about this price — find out in our valuation breakdown.

The Diamondback Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Diamondback Energy extend this valuation puzzle by spelling out which paths for Diamondback Energy's revenue, margins and earnings would need to play out for the stock to be worth meaningfully more or less than it is today on the market. Each one treats fair value as a concrete, testable view of the business that you can revisit over time rather than a one off snapshot.

One of the top community narratives on Diamondback Energy: 28% undervalued

"Operational efficiencies, disciplined capital allocation, and acquisitions position Diamondback for stable cash flow and shareholder returns despite volatile energy markets..."

Read one of the top narratives on Diamondback Energy

Do you think there's more to the story for Diamondback Energy? Head over to our Community to see what others are saying!

The Bottom Line

For Diamondback Energy, the current market multiple suggests the stock is priced close to what its revenue profile and risks support rather than offering an obvious discount. The mixed valuation checks back up that middle ground, hinting at neither a clear opportunity nor a clear red flag on price alone. From here, the key question is whether Diamondback Energy can keep translating its operating profile and exposure to crude prices into earnings that justify staying on this higher valuation plateau, or whether shifting sentiment on oil and capital discipline eventually forces a reset in what investors are willing to pay.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com