3 Australian Gold And Asset Management Stocks With Strong Balance Sheets

With global growth signals mixed, inflation patterns uneven across regions, and interest rates still shaping bond and housing markets, many investors are looking for companies that rely on solid finances rather than perfect economic conditions. Our Solid Balance Sheet and Fundamentals screener focuses on stocks with high return on equity, resilient past performance and stronger balance sheets, which can help you stay focused on quality when headlines are noisy. In this article, you will see 3 stocks from this screener that stand out on financial strength and business fundamentals, and how they might fit different portfolio styles.

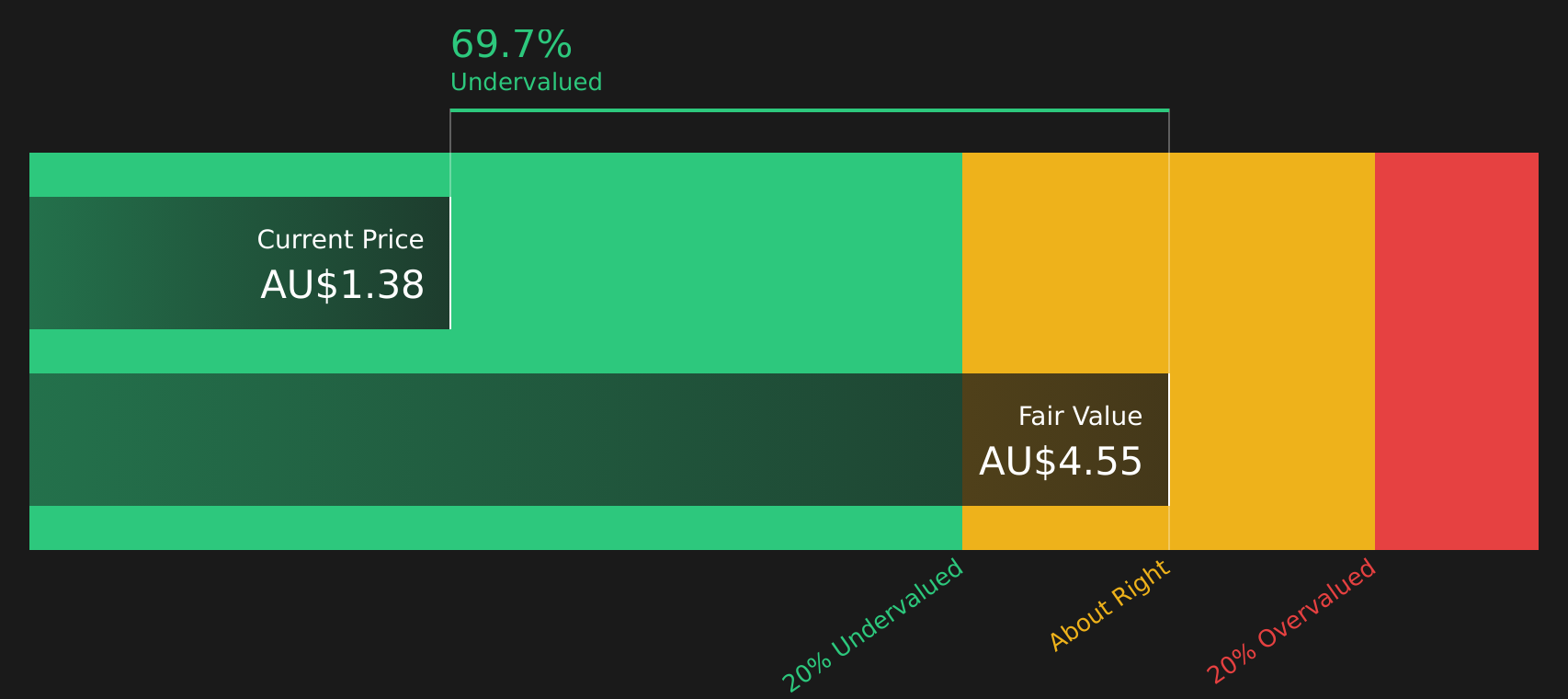

Ora Banda Mining (ASX:OBM)

Overview: Ora Banda Mining (ASX:OBM) is an Australian miner focused on exploring, developing, and operating gold and base metal projects, anchored by its 100% owned Davyhurst Gold Project north west of Kalgoorlie. The company targets gold as its core commodity, with additional exposure to nickel, copper, and lithium across its portfolio.

Operations: Ora Banda Mining currently generates all of its A$554.1 million in revenue from gold production and exploration in Australia.

Market Cap: A$1.93b

Ora Banda Mining catches the eye because it combines a sizeable producing asset with an aggressive growth plan and a valuation that screens as inexpensive against estimated fair value. Record quarterly output at Davyhurst and a large step up in mineral resources and ore reserves give the company more optionality for its “DRIVE to 300” production expansion, supported by heavy drilling investment. High current and forecast returns on equity and strong profit margins point to efficient use of capital. However, a high share of non cash earnings and reliance on external borrowing introduce quality and funding risks that investors may wish to weigh carefully. For investors who want to see how those positives and trade offs balance out, there is more to unpack in the detailed fundamentals and risk breakdown.

Ora Banda Mining’s push to scale Davyhurst while screening as inexpensive on fundamentals raises a clear question: how much of that story is already in the numbers and what the 4 key rewards and 1 important major warning sign might reveal about the next chapter

Regis Resources (ASX:RRL)

Overview: Regis Resources (ASX:RRL) is an Australian gold producer and explorer that operates and develops open pit and underground gold projects, including the Duketon and Tropicana operations in Western Australia and the McPhillamys project in New South Wales.

Operations: Regis Resources generates A$1.23b of revenue from Duketon and A$730.7m from Tropicana, with all A$2.0b of revenue earned in Australia.

Market Cap: A$4.27b

Regis Resources earns a place on a solid balance sheet and fundamentals shortlist because it combines high current profitability with financial flexibility and meaningful growth options in its project pipeline. Strong operating cash flow and the absence of corporate debt provide room to fund McPhillamys and other projects. In addition, a high return on equity and relatively low P/E suggest the market may not fully reflect these assets. At the same time, the story is far from risk free, with sensitivity to gold prices, rising mining costs, and regulatory uncertainty around project approvals all capable of affecting future cash flows and valuation. This is where the detailed fundamentals and risk work really matter for investors weighing Regis against other quality gold stocks.

Regis Resources appears to be a high margin cash engine with no corporate debt, yet its P/E hints at skepticism. Get the fuller picture with the analyst forecasts for Regis Resources, including what the market might be missing.

GQG Partners (ASX:GQG)

Overview: GQG Partners (ASX:GQG) is a global boutique asset manager that runs active equity strategies for large institutions, pension and super funds, sovereign wealth funds, high net worth clients and wealth managers, offering its portfolios through funds, separate accounts and listed vehicles around the world.

Operations: GQG Partners generates all of its US$808.3m in revenue from asset management, with about US$656.7m from the United States and US$151.5m from international clients.

Market Cap: A$4.13b

GQG Partners interests investors because it combines a very high profit margin and strong return on equity with a low P/E and a share price that screens well below some fair value estimates, while still paying out around 90% of distributable earnings as dividends. At the same time, sustained fund outflows, an earnings and revenue decline expected over the next few years, a very high dividend yield that is not fully covered, and a key person and governance profile centred on a founder with a large stake all introduce meaningful risk. The tension between these powerful cash flows and those flow and leadership risks is what makes GQG Partners stand out on a quality screener.

GQG Partners looks like a cash machine trading on hesitation, with a rich dividend profile sitting beside governance and flow questions. Get the full story in the analysis report for GQG Partners

The three stocks in this article are only a starting point, with our full Solid Balance Sheet and Fundamentals screener surfacing 17 more companies that pair high return on equity, solid past performance and strong balance sheets with equally compelling narratives. Use Simply Wall St to identify, analyze and filter for the exact catalysts and storylines that matter most to you so you can focus on the highest conviction ideas.

Take Control of Your Investment Journey

If GQG Partners or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do?

Fresh ideas can move from quiet to flying under the radar in a hurry, and once momentum builds, ideal entry points can shrink quickly. It may be worth scanning new angles and deciding whether to act sooner rather than later.

- Review the 6 dividend fortresses to find potential income workhorses early, and focus on companies built around consistent cash generation instead of chasing the latest story.

- Use the 62 profitable AI stocks that aren't just burning cash to track where AI-related profitability is already showing up in the numbers, before broader attention affects the most compelling risk reward setups.

- Check the 8 top copper producer stocks to explore long term demand in critical materials, rather than reacting primarily to short term commodity headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com