Can Hailey Bieber’s Denim Capsule Really Refresh Gap’s (GAP) Culture-Led Brand Strategy?

- Earlier this week, Gap announced it had partnered with beauty entrepreneur and influencer Hailey Bieber to launch “The Hailey Jean,” a limited-edition ’90s-inspired relaxed denim capsule featuring Extra Baggy and ’90s Low Rise Loose fits with 1996-themed detailing, available online and in select stores.

- The collaboration highlights Gap’s effort to connect heritage denim with culture-led marketing, using Bieber’s influence to reach younger shoppers and reinforce its focus on relaxed fits.

- Next, we’ll examine how this Hailey Bieber collaboration fits into Gap’s broader brand reinvigoration and long-term earnings narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

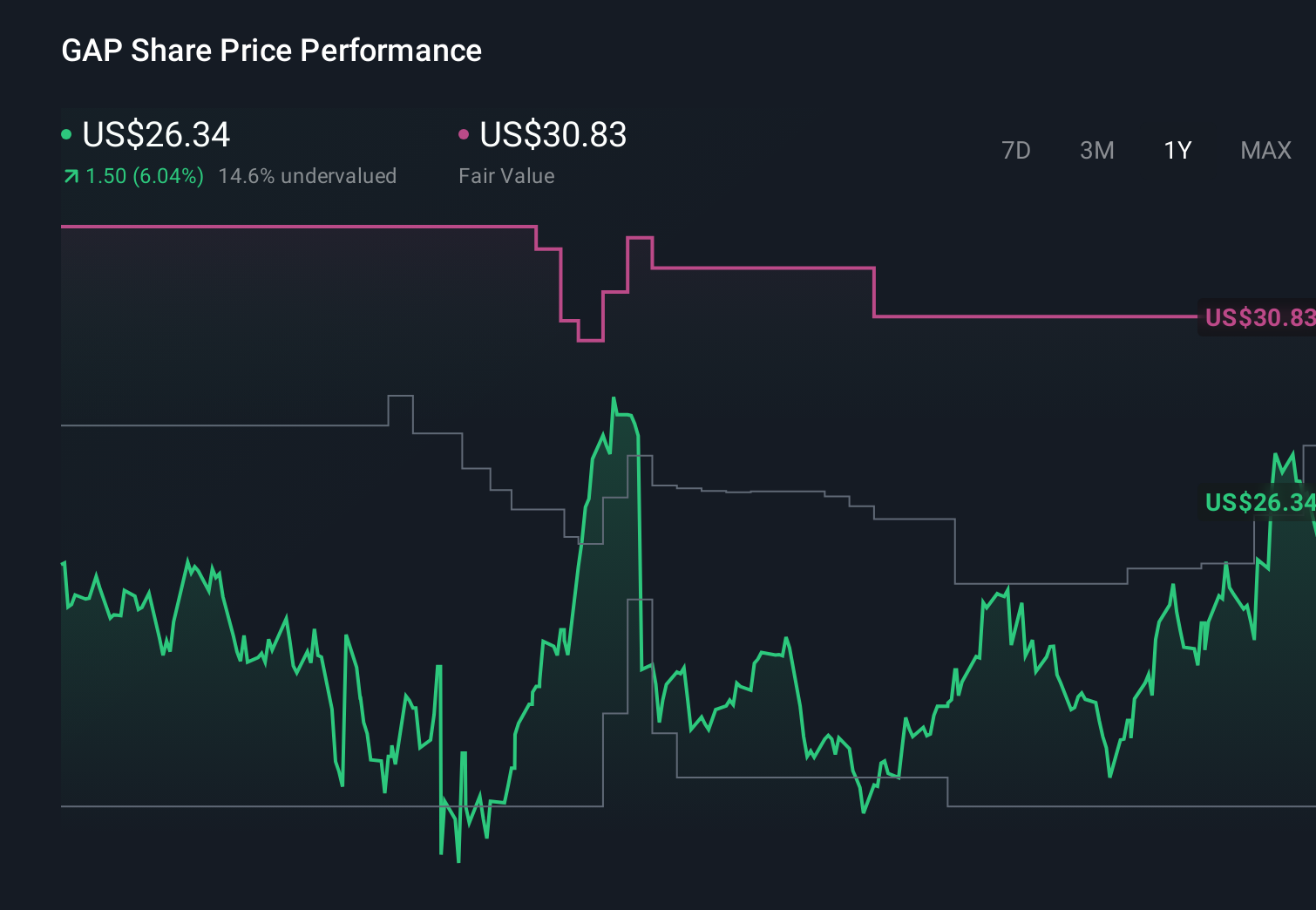

Gap Investment Narrative Recap

To own Gap, you need to believe the company can turn culture-led marketing and heritage denim into steady earnings while managing margin pressure and inventory risk. The Hailey Bieber launch may support near term interest in relaxed fits, but on its own it does not materially change the biggest swing factors right now: sustaining low single digit sales growth and avoiding heavy discounting if demand softens.

The most relevant recent announcement here is Gap’s May 2026 decision to raise full year FY2027 EPS guidance to about US$2.83 to US$2.93. That move tied brand reinvigoration, cost control and omni channel investments to higher earnings power. The Hailey Jean capsule sits squarely in that playbook, putting more weight on whether culture-driven campaigns can support the modest growth and margin expansion implied in that outlook.

But even with the buzz around Hailey Bieber, investors should still be aware of the risk that heavy promotions could return and...

Read the full narrative on Gap (it's free!)

Gap’s narrative projects $16.5 billion revenue and $1.0 billion earnings by 2029.

Uncover how Gap's forecasts yield a $27.26 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a much harsher view, assuming revenue creeps to only about US$16.2 billion and earnings to roughly US$969 million, so you should weigh that cautious outlook against the current buzz around influencer driven campaigns and decide which story feels closer to your own expectations.

Explore 5 other fair value estimates on Gap - why the stock might be worth just $20.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Gap research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Gap research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gap's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com