Ecolab (ECL) Stock Looks Near Fair Value As Its 49% Run Continues

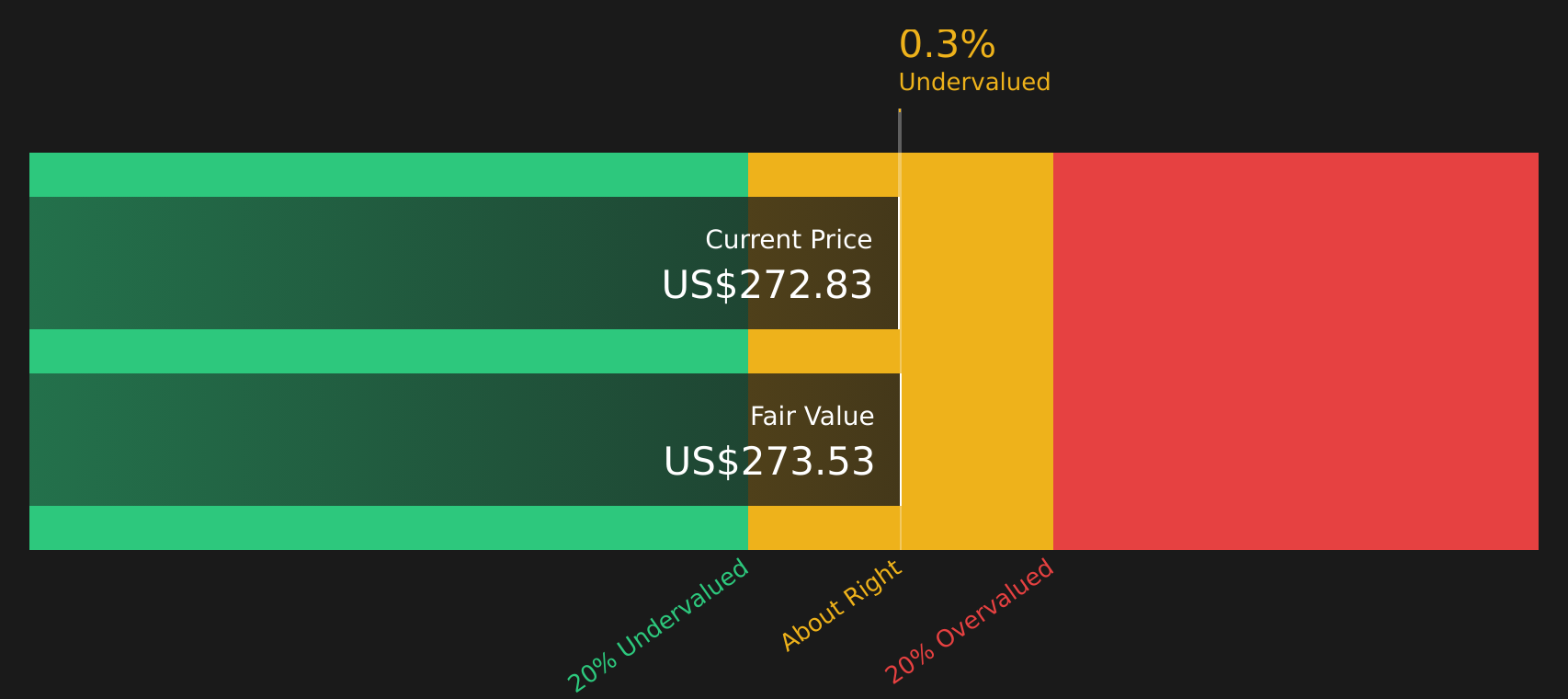

Ecolab stock has delivered a 48.8% total return over the past three years, and at around US$272.83 per share the key question is whether that run now leaves it trading close to its intrinsic value or at a premium. The Discounted Cash Flow (DCF) estimate points to Ecolab being roughly fairly valued, while the broader valuation checks and market multiples lean more cautious.

- Ecolab's 48.8% return over three years means anyone who stayed invested has been rewarded, so fresh buyers now need to think carefully about how much upside is left from here.

- Recent commentary around pricing actions offsetting commodity inflation can support expectations for earnings and cash flow, but those same pricing moves may also heighten the risk that investors are already assuming a lot of that improvement in the current share price.

- With a low value score of 1 out of 6 checks, Ecolab does not screen as a clear bargain when looking across multiple valuation measures.

The issue now is whether Ecolab's current price, after a strong multi year return, still offers a margin of safety relative to its intrinsic value estimate and earnings multiples.

Find out why Ecolab's 2.6% return over the last year is lagging behind its peers.

Does Ecolab Look Fairly Valued on Cash Flow?

The Discounted Cash Flow (DCF) model for Ecolab is built around its ability to generate cash over time. Based on the latest twelve month free cash flow of about $2.0b and an assumption of growing cash flows, the 2 Stage Free Cash Flow to Equity model arrives at an intrinsic value of roughly $273 per share. That sits almost exactly in line with the current share price of about $272.83, implying only a 0.2% discount.

Because RBC’s recent focus is on pricing actions offsetting commodity inflation, it is helpful that the DCF already rests on cash flows rather than headline earnings, which can be more sensitive to near term cost moves. The small gap between the model value and the market price suggests investors are largely aligned with these cash flow expectations.

Overall, the Discounted Cash Flow workup implies Ecolab stock is approximately fairly valued at today’s price.

Ecolab is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Ecolab Getting Expensive on Earnings?

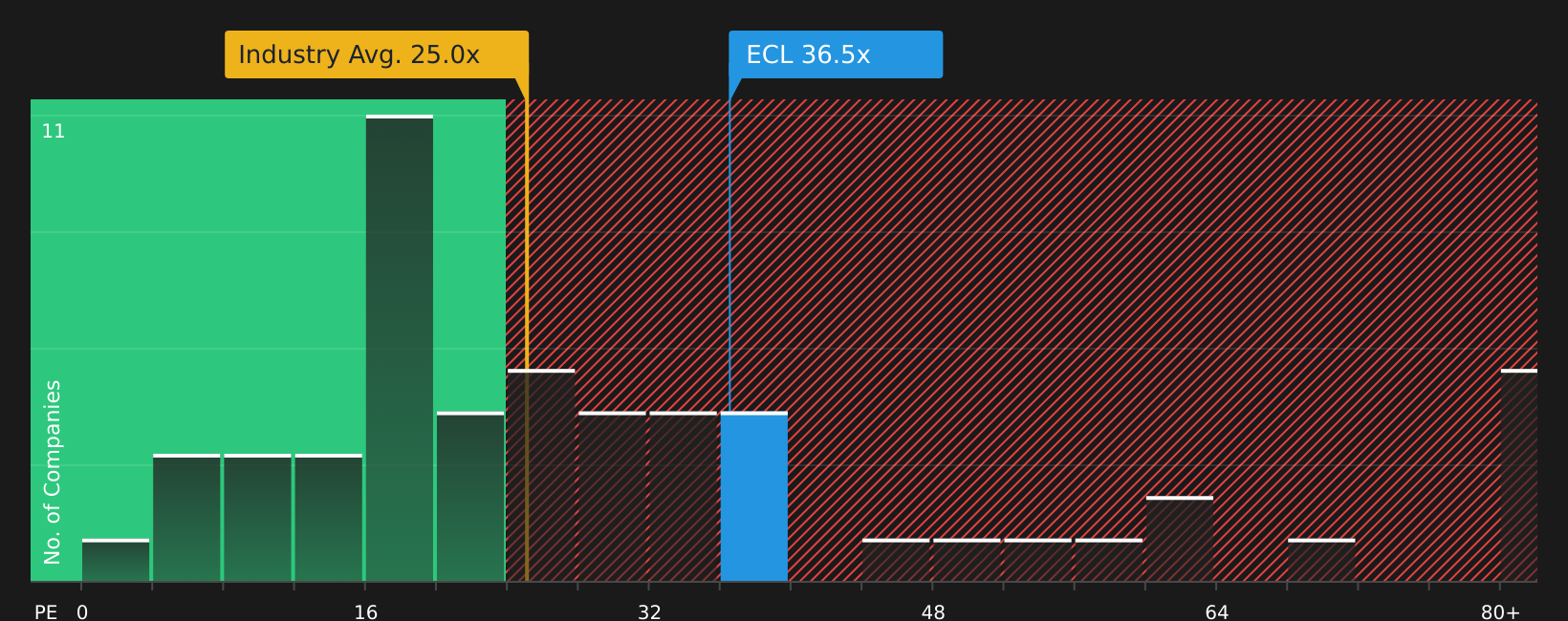

The P/E ratio is a useful way to judge how much investors are paying for each dollar of Ecolab's earnings. Ecolab currently trades on a P/E of about 36.5x, compared with an industry average of roughly 25.0x and a peer average of about 23.1x, so the stock sits at a clear premium to both its sector and similar companies.

A fair P/E multiple for Ecolab, based on factors like its industry, business profile and risk, is estimated at about 24.6x, which is well below the current 36.5x. That gap indicates investors are paying materially more than this framework would suggest, even after allowing for the quality of the business and its position within the chemicals industry.

Overall, Ecolab stock currently appears overvalued on its P/E multiple relative to both its peers and a tailored fair-value benchmark.

See what the numbers say about this price — find out in our valuation breakdown.

The Ecolab Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Ecolab pick up where the valuation puzzle leaves off. They spell out which views on Ecolab's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. Each narrative ties its number to a clear stance on how Ecolab's growth, profitability and risk profile could evolve, giving you a reference point to revisit as fresh information emerges.

Share your own narrative on Ecolab, setting out a number-driven view on whether Ecolab's pricing surcharges offset commodity inflation as expected, and see how your thesis holds up as new results are released.

Do you think there's more to the story for Ecolab? Head over to our Community to see what others are saying!

The Bottom Line

For Ecolab, the Discounted Cash Flow (DCF) work suggests the stock is close to intrinsic value, so there is no clear margin of safety on cash flows alone. Market multiples, however, still flag Ecolab as overvalued relative to peers and a tailored fair P/E, which keeps the broader valuation picture cautious rather than outright cheap. The crux from here is whether the company can deliver on the earnings and pricing power implied by that premium multiple, or whether the P/E gradually settles closer to sector norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com