Rivian (RIVN) Stock May Be Overvalued Even As Sales Stay Strong

Rivian Automotive’s share price has swung between sharp setbacks and rebounds over the past few years, and with the stock recently around US$17.46, the core question for investors is whether that price still looks rich given a weak overall value score and mixed sentiment around its capital needs.

- Over the past 3 years the stock has declined about 30.9%, which suggests investors who bought early are still facing a material drawdown despite more recent strength.

- On the one hand, expectations for higher vehicle deliveries and new initiatives such as the investment in e-bike startup Also can support long term revenue potential. On the other hand, concerns about ongoing cash burn, shareholder dilution from recent equity raising, and competition in electric vehicles may limit how much valuation investors are willing to pay.

- Rivian scores only 2 out of 6 on the broader valuation checks, which leans more toward the stock looking expensive than like a clear bargain.

The issue now is whether Rivian’s current market price still builds in too much optimism relative to the risks around funding, profitability, and competitive pressure.

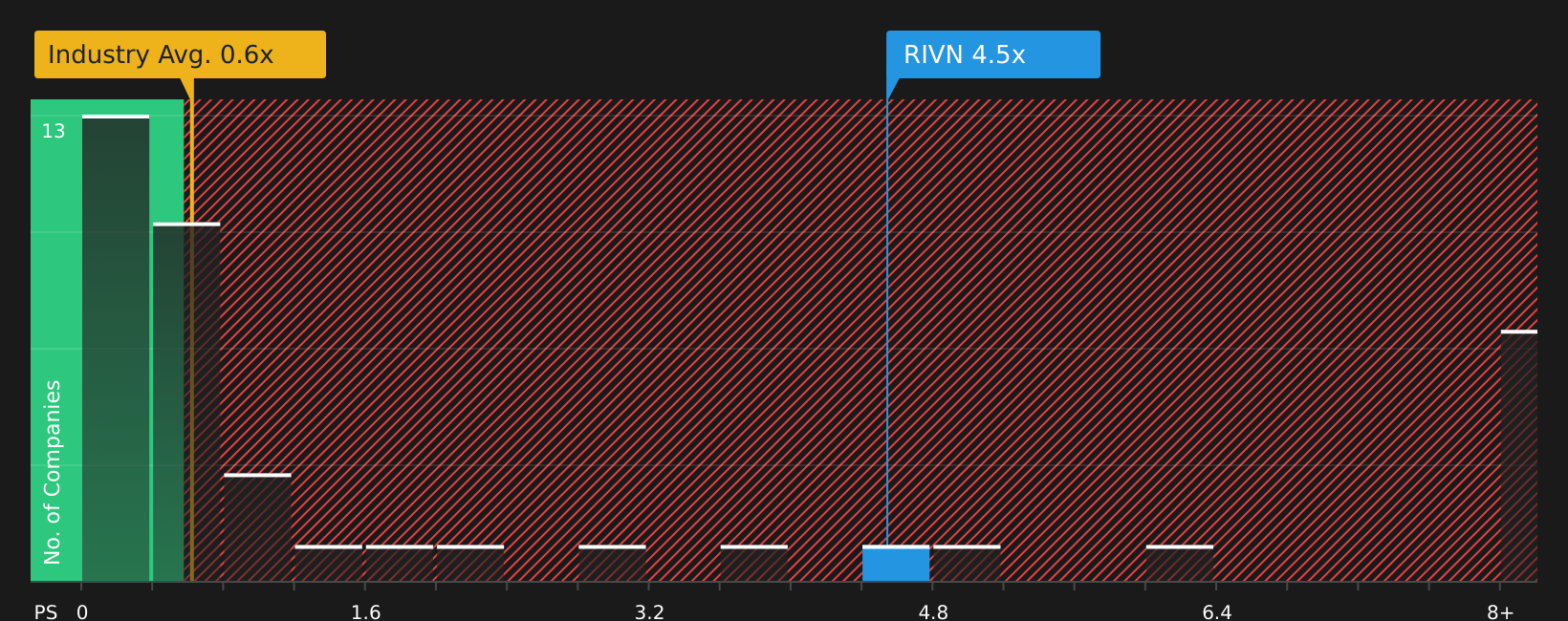

Does Rivian Automotive Look Pricey on Sales?

P/S is a useful way to look at Rivian Automotive because the company is still focused on scaling revenue while it works toward more stable profitability.

Rivian trades on a P/S of about 4.5x, compared with an auto industry average of roughly 0.6x and a peer average around 0.8x. On a tailored basis, the fair P/S ratio for Rivian is estimated at about 2.0x, which is less than half of where the stock currently sits. This framework suggests investors are paying a sizeable premium for each dollar of Rivian’s sales relative to the broader auto sector and closer peers.

Despite recent headlines around capital raises and updated delivery guidance, that premium P/S implies the market is already assigning Rivian a relatively rich sales valuation.

Overall, Rivian Automotive stock appears overvalued on its current P/S multiple compared with both modelled fair value and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Rivian Automotive Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Rivian Automotive pick up where this valuation puzzle leaves off by spelling out the growth, margin and earnings paths that would need to play out for the stock to be worth materially more or materially less than today's price. Each Narrative ties a specific fair value to one clear story about Rivian Automotive's potential catalysts and key risks, so you can watch over time which version of events is actually unfolding on the Community page.

Community views on Rivian Automotive sit on a wide spectrum, ranging from roughly fairly valued on the upside to concerns that expectations still look rich.

Bull case: roughly fairly valued

"The launch of the R2 platform represents a step-change improvement in Rivian's cost structure, with management securing supplier contracts and component sourcing that reduce bill of materials by nearly 50% versus R1…"

Read the full Bull Case to see why Rivian Automotive could be undervalued

Bear case: 34% overvalued

"Without a rapid improvement in demand or meaningful reduction in cost per unit, Rivian's net margins and free cash flow will remain deeply negative, which may require dilutive equity issuance or further debt…"

Read the full Bear Case to see why Rivian Automotive could be overvalued

Do you think there's more to the story for Rivian Automotive? Head over to our Community to see what others are saying!

The Bottom Line

Rivian Automotive screens as overvalued on its current P/S multiple, with the market clearly paying up for future growth and execution that are not yet proven. The broader checks also lean weak, which reinforces the idea that expectations already sit on the optimistic side. For you as an investor, the key question from here is whether Rivian can scale production, improve unit economics and manage funding needs well enough to eventually justify this premium sales multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com