Will Dorian LPG’s (LPG) US$1 Irregular Dividend and Asset Sale Shift Its Capital-Return Narrative?

- Dorian LPG Ltd. recently declared an irregular US$1.00 per-share cash dividend, returning about US$42.8 million to shareholders, following the earlier sale of its 2014-built VLGC Corsair for roughly US$81.8 million and repayment of US$24.2 million of associated debt in the quarter ended June 30, 2026.

- Together, the special dividend and vessel sale highlight Dorian LPG’s use of asset recycling and excess liquidity to return capital while reshaping its fleet profile.

- We’ll now examine how this one-off US$1.00 irregular dividend influences Dorian LPG’s income-focused, fleet-renewal investment narrative beyond 2026.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

DorianG Investment Narrative Recap

To own DorianG, you need to believe LPG shipping will remain a viable cash generator and that management will keep turning that cash into shareholder returns while managing freight rate volatility and environmental regulation risk. The latest irregular US$1.00 dividend and Corsair sale support the near term income story, but do not fundamentally change the biggest swing factor today: exposure to spot freight rates and potential market overcapacity.

The June 23 announcement to order a new 90,000 cbm VLGC for about US$115 million, alongside MOUs to sell three mid‑2010s vessels for roughly US$256 million, ties directly into this dividend decision. Proceeds from asset sales are helping fund both the newbuild program and these irregular dividends, reinforcing the theme that fleet renewal and capital returns are currently being funded by recycling older assets rather than incremental leverage or core earnings alone.

Yet beneath these generous cash returns, investors should be aware that tightening environmental rules could eventually reshape DorianG's cost base and dividend capacity...

Read the full narrative on DorianG (it's free!)

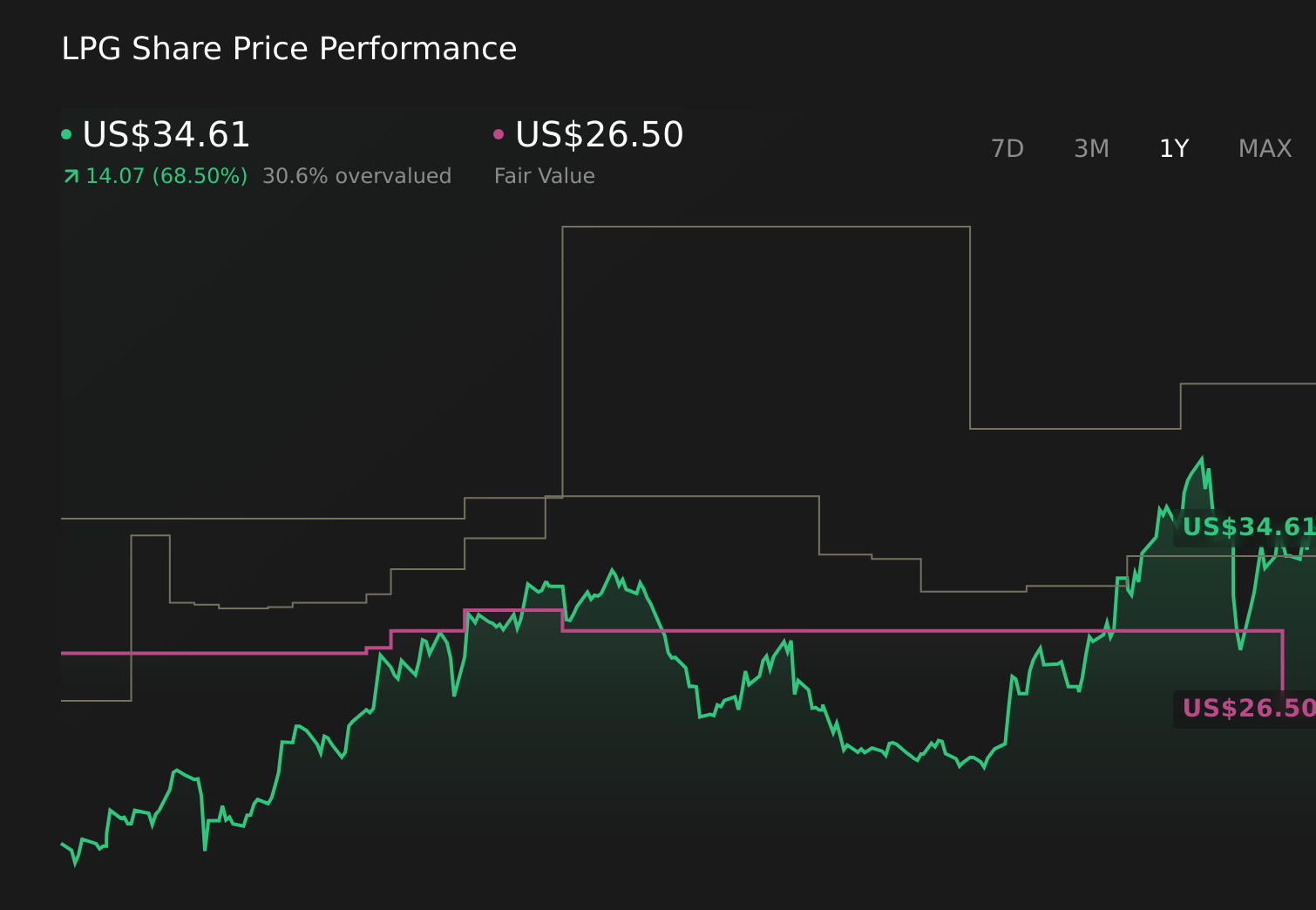

DorianG's narrative projects $371.0 million revenue and $64.9 million earnings by 2029.

Uncover how DorianG's forecasts yield a $51.20 fair value, a 25% upside to its current price.

Exploring Other Perspectives

While this dividend looks attractive, the most pessimistic analysts were already projecting revenue falling to about US$362.7 million and earnings to just US$16.9 million, so you should weigh this payout against the risk that rising compliance costs could still pressure future margins and distributions.

Explore 2 other fair value estimates on DorianG - why the stock might be worth just $39.31!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your DorianG research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free DorianG research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DorianG's overall financial health at a glance.

No Opportunity In DorianG?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com