Ouster (OUST) Updates EBITDA Breakeven Plan On A Valuation Narrative Still In Question

Ouster (OUST) recently updated investors on its financial roadmap, highlighting a focus on reaching EBITDA breakeven supported by efforts in revenue growth, product development across its lidar portfolio, and wider adoption in automotive, industrial, and smart infrastructure markets.

See our latest analysis for Ouster.

The recent EBITDA breakeven update comes after a mixed share price run, with Ouster’s 1 day share price return of 5.41% contrasting with a 7 day decline of 14.42%, a 30 day decline of 9.04%, and a stronger 90 day share price return of 52.68%. Over a longer horizon, the 3 year total shareholder return is very large and the 5 year total shareholder return is down 60.64%, suggesting momentum has picked up in the shorter term but with a volatile longer history.

If you are looking beyond Ouster for other sensor and automation plays, this could be a good moment to scout 33 robotics and automation stocks

After Ouster’s sharp swing higher over the past quarter but mixed longer term record, the key question is whether the market has already priced in much of the EBITDA breakeven story or if meaningful upside is still on the table.

Most Popular Narrative: 24.4% Undervalued

The most followed narrative for Ouster pegs fair value at $49.00 versus a last close of $37.04, framing the current EBITDA breakeven story against a richer long term path.

Ouster is tapping into the massive Intelligent Transportation Systems (ITS) market with their Blue City traffic management solution, which could drive significant revenue growth as they expand deployments across the US, Europe, and Asia. This is expected to positively impact revenue.

Want to see what sits behind that optimism on traffic systems and autonomy hardware? The narrative focuses on rapid top line expansion, tightening margins, and a rich future earnings multiple. It examines how those moving parts combine into a $49.00 fair value and a double digit discount to today’s price.

Result: Fair Value of $49.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Ouster’s story still hinges on turning a loss of $55.825 million into consistent profitability while facing heavy competition in lidar and perception systems, which could pressure pricing and market share.

Find out about the key risks to this Ouster narrative.

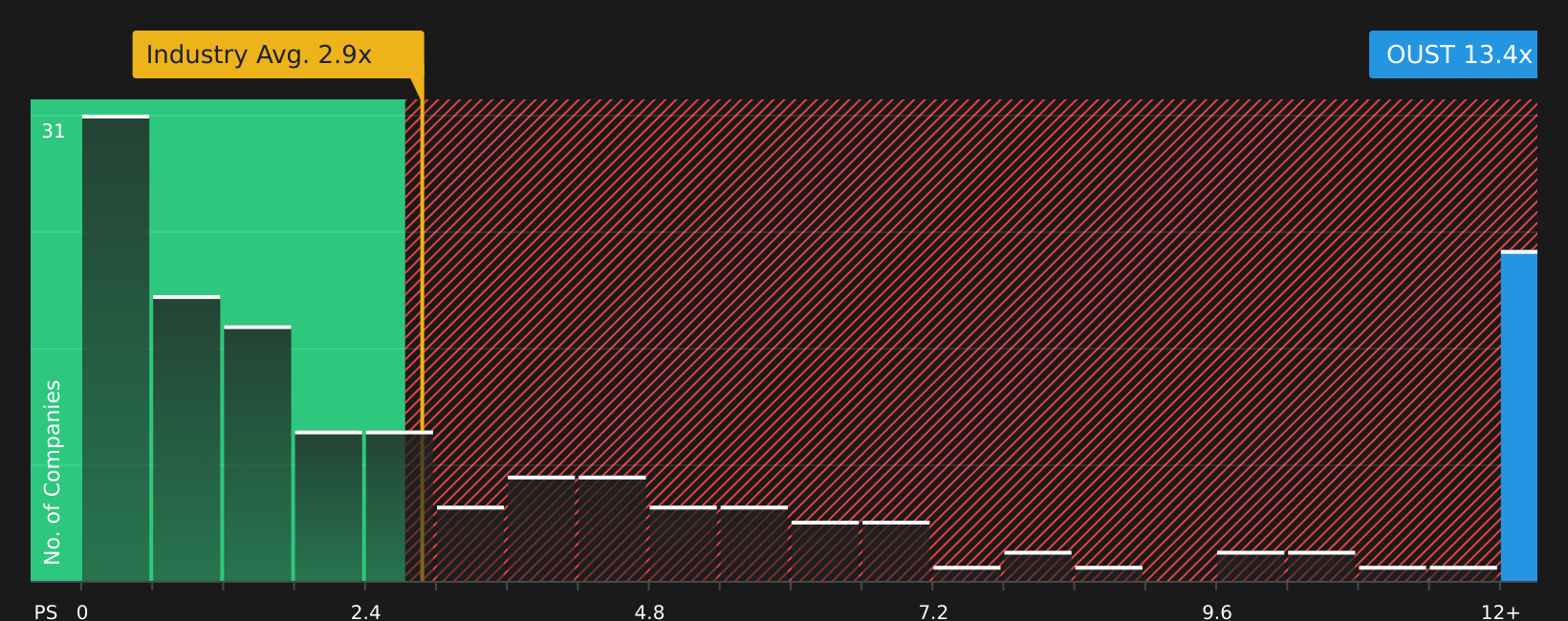

Another View: Ouster On Sales-Based Valuation

While the SWS DCF model points to Ouster trading 46% below its estimated fair value, the picture looks very different when you switch to a simple P/S lens. At 13.4x sales versus a peer average of 2.5x and a fair ratio of 7.6x, the stock screens expensive rather than cheap. Which signal carries more weight for you as an investor?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Feeling torn between the upbeat fair value narrative and the challenges still facing Ouster? Take a closer look at both sides and move quickly to shape your own view using 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Ouster?

If you are serious about building a stronger portfolio alongside Ouster, this is the moment to scan other focused opportunities before they move out of reach.

- Target potential bargains with quality fundamentals by reviewing the 47 high quality undervalued stocks that could complement or contrast with your Ouster thesis.

- Prioritize resilience and sleep better at night by checking the 84 resilient stocks with low risk scores that stand out on stability and downside protection.

- Hunt for underfollowed opportunities by scanning the screener containing 20 high quality undiscovered gems that may not yet be on most investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com