Rare Earth Stocks To Watch As Magnet Supply Security Gains Importance

Rare earth metal stocks sit at the crossroads of technology, defense, and the clean energy buildout. Today’s mixed global backdrop, from steady US bond yields to shifting industrial output in Asia and Europe, keeps attention firmly on supply security for these materials. With only a limited pool of companies focused on mining these critical elements, a targeted Rare Earth Metal Stocks screener can help you cut through market noise and focus on pure exposure to this theme. This article highlights three rare earth stocks from that screener to watch right now.

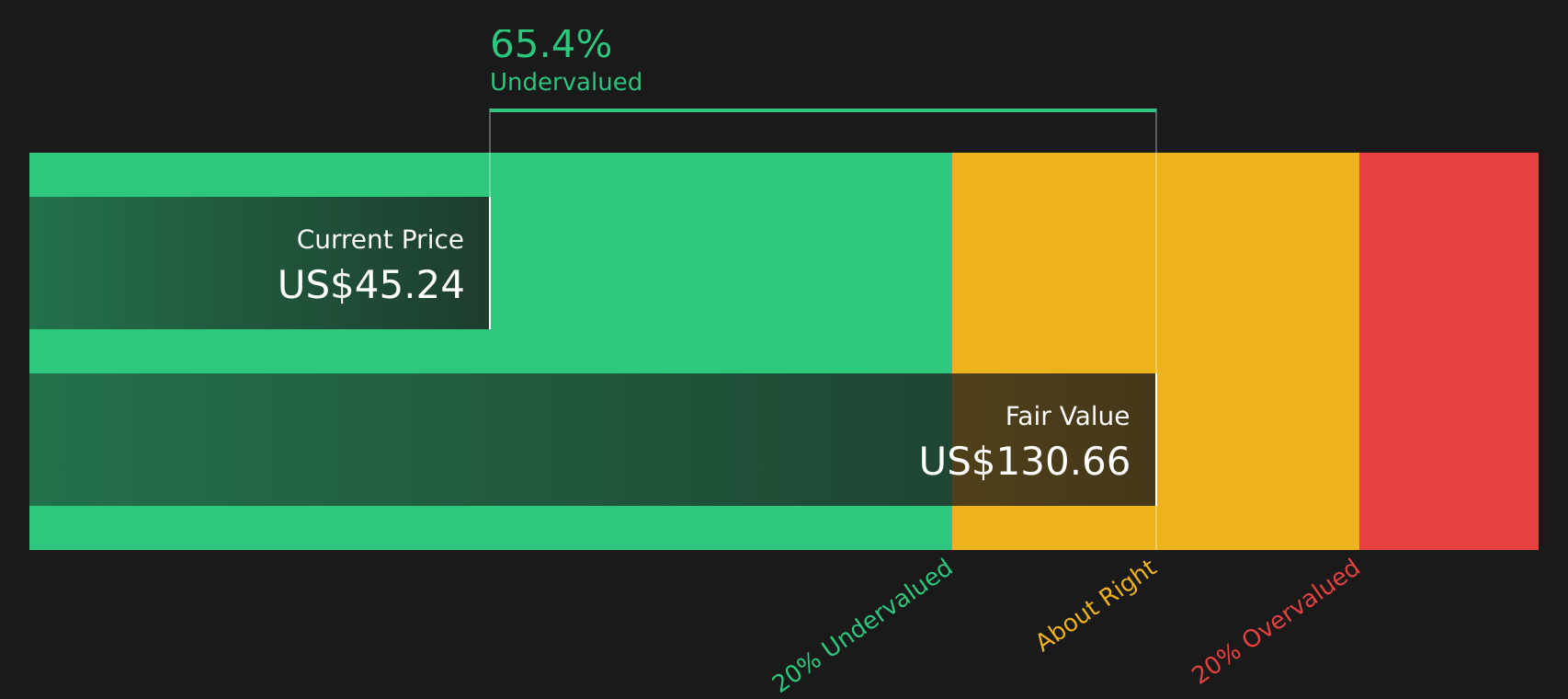

MP Materials (MP)

Overview: MP Materials is a US based rare earth producer that owns the Mountain Pass mine in California and also manufactures higher value NdPr based magnetic materials and finished NdFeB permanent magnets used in electric vehicles, wind turbines, electronics and defense applications.

Operations: MP Materials generates about US$270.2 million in revenue from its Materials segment and US$82.7 million from Magnetics, with total revenue of roughly US$347.6 million coming from customers in the United States.

Market Cap: US$8.1b

MP Materials offers exposure to the rare earth magnet theme focused on US supply security, with its Mountain Pass mine feeding into in house NdPr processing and the 10X magnet plant backed by long term contracts with the US Department of Defense, Apple and GM. That mix can provide clearer revenue visibility and potential margin benefits as more production shifts from raw materials into finished magnets, but it also involves trade offs such as customer concentration, contract restrictions on certain end markets and heavy spending on new facilities. Alongside insider selling and a premium valuation, MP Materials represents a business where the potential upside is balanced by meaningful execution and funding risks.

MP Materials looks like a rare earth powerhouse in the making, but the real story is how its mine, processing, and magnet contracts fit together. Read the 3 key rewards and 1 important warning sign

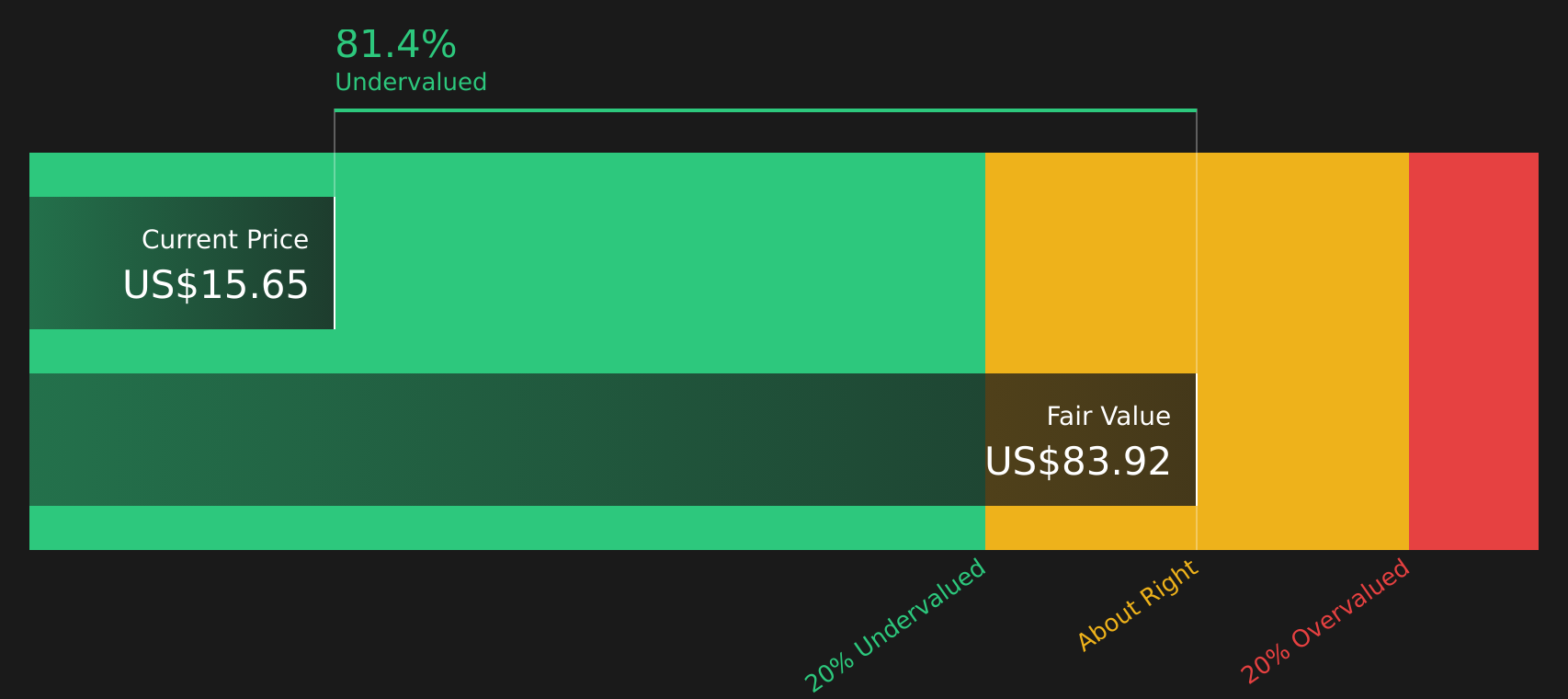

USA Rare Earth (USAR)

Overview: USA Rare Earth is a Stillwater, Oklahoma based company aiming to build a fully domestic rare earths and critical minerals chain, from the Round Top Mountain resource in Texas through to separated oxides and magnet materials used in defense, semiconductors, data centers, electric vehicles, energy and healthcare.

Market Cap: US$3.9b

USA Rare Earth has quickly become one of the more ambitious rare earth stories, combining mining rights at Round Top, early magnet production and a series of US and European projects with backing that includes up to US$1.6b from the US Department of Commerce and a separate potential US$19.3m from the Department of Energy for pilot scale separations. Forecasts pointing to rapid revenue and earnings growth, plus a share price sitting well below some fair value estimates, are what pull investors in. However, this is still an early stage, loss making business with a short cash runway, heavy external funding, insider selling and a relatively inexperienced leadership team. The potential upside case depends on whether those large projects and government partnerships translate into durable, profitable operations.

USA Rare Earth’s government backing and early projects hint at a much bigger story than the current share price suggests, but the real turning point sits inside the 3 key rewards and 4 important warning signs (2 are major!)

Lynas Rare Earths (ASX:LYC)

Overview: Lynas Rare Earths is an Australia based company that mines and processes rare earth minerals from its Mt Weld operation and refines them through plants in Kalgoorlie and Malaysia, supplying a wide range of light and heavy rare earth oxides used in magnets, electronics, and other industrial applications.

Operations: Lynas Rare Earths generates about A$715.9 million in revenue from its Rare Earth Operations segment.

Market Cap: A$16.0b

Lynas Rare Earths stands out as a large, integrated rare earth supplier outside China, with A$715.9 million in rare earth operations revenue, exposure to magnet demand, and a long term supply and equity deal with JS Link that extends to 2038. The current P/S ratio and the past 5 year earnings decline are important reference points for setting expectations. In addition, ambitious downstream expansion, regulatory sensitivities in Malaysia, and reliance on external borrowing mean execution and policy considerations remain significant. The key issue is how these factors combine in the detailed risk and reward profile that investors may wish to assess more closely.

Lynas Rare Earths sits at the center of ex China supply, and its A$715.9 million in rare earth revenue and JS Link agreement to 2038 only hint at the full picture inside the analysis report for Lynas Rare Earths

The three rare earth metal stocks in this article are just a starting point, as the full Rare Earth Metal Stocks screener has surfaced 26 more companies with equally compelling narratives tied to defense, clean energy, and high tech demand. Use Simply Wall St to identify, analyze, and filter those rare earth stocks by the specific catalysts and narratives that matter most to you so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Lynas Rare Earths or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh stock ideas can move from quiet accumulation to breakout momentum fast, and once they are flying it is hard to get a clean entry, so consider acting early instead of chasing later.

- Spot smaller companies where momentum could be building by scanning 20 elite penny stocks with strong financials curated for stronger balance sheets and healthier cash flows than typical high risk micro caps.

- Explore the next wave of automation by checking 33 robotics and automation stocks packed with companies tied to factories, warehousing, and hardware supplying the shift to smarter machines.

- Review potential grid upgrades ahead of major spending cycles by looking at 33 power grid technology and infrastructure stocks featuring businesses focused on transmission tech, grid stability, and supporting infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com